Utilities Brighten Under Cloud of Recession, but Future Dim at Lofty Valuations

Renewable energy continues to be a long-term boon for the sector.

/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)

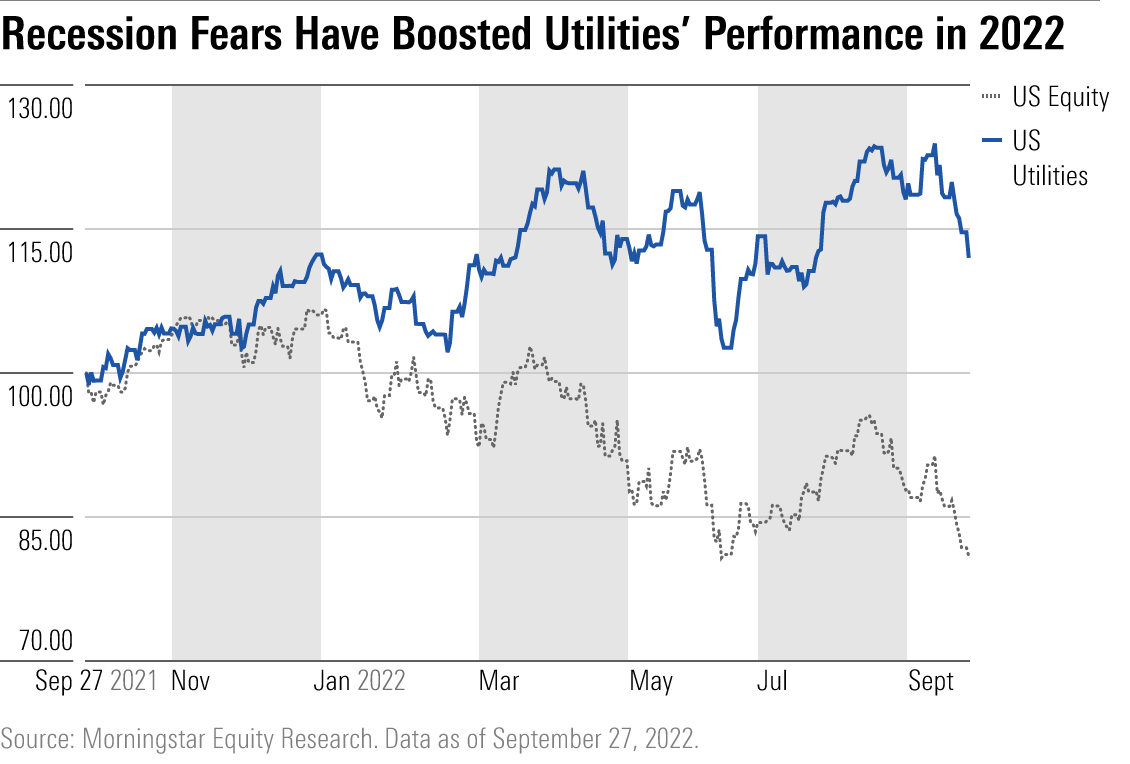

Despite high inflation and rising interest rates, utilities investors aren’t scared. Utilities stocks are outperforming the market by more than 30 percentage points going into the fourth quarter. If they hold that lead, utilities would outperform the market by the widest margin since 2000. Absolute returns have been solid as well. Utilities and energy are the only two sectors with positive year-to-date returns.

Unsurprisingly, utilities have benefited from the market’s recession concerns. Utilities also outperformed ahead of the 2001 and the 2007-09 recessions. Once the market digested the last two recessions, utilities’ outperformance quickly reversed. Utilities lagged the market for three consecutive years following the 2000 recession and four of the five years following the 2007-09 recession.

What's Up With Utilities?

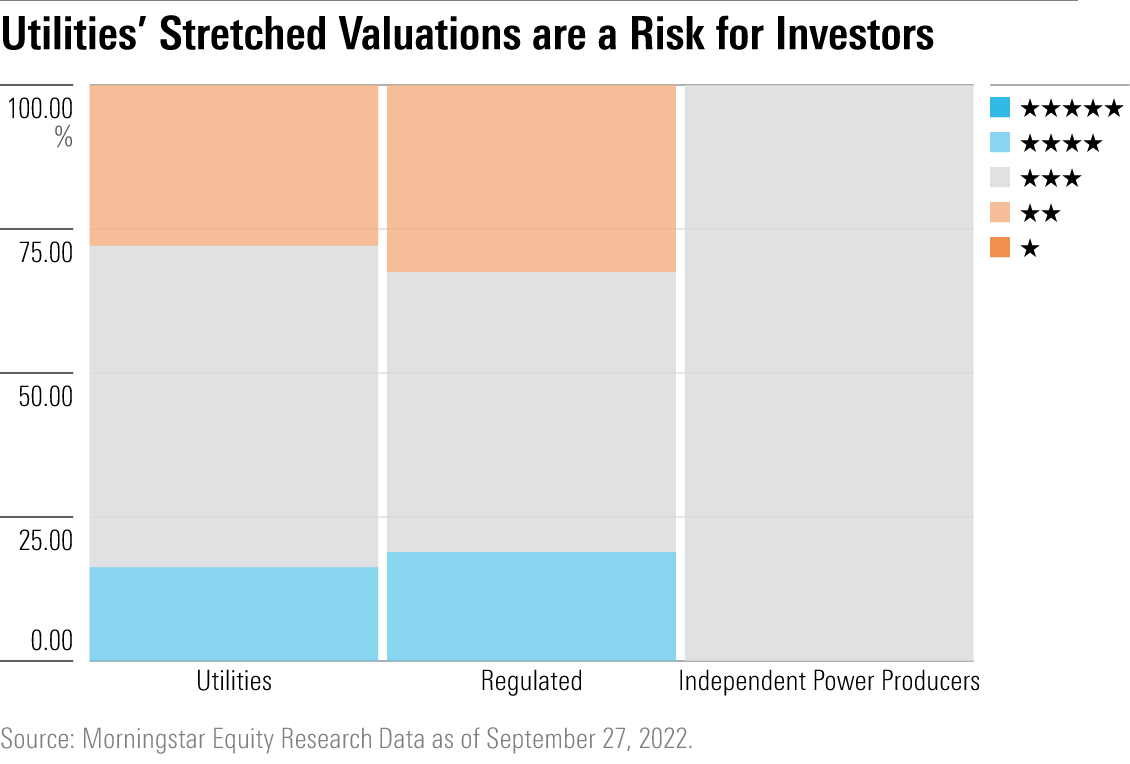

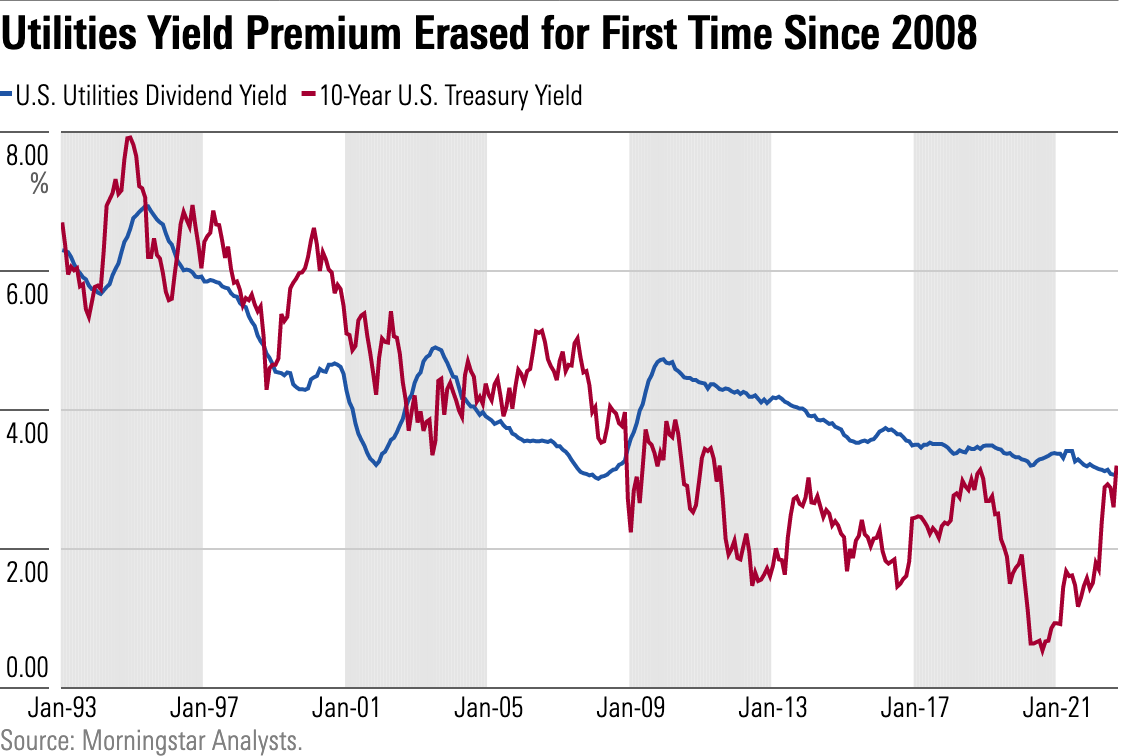

We think utilities will struggle to match those returns going forward. U.S. utilities are 3% overvalued based on our fair value estimates, making it the most overvalued sector. Dividend yields have lost their appeal. In June, 10-year U.S. Treasury rates topped the Morningstar U.S. Utilities Index dividend yield for the first time in 14 years.

Growth is the only way we think utilities can avoid a steep correction. We forecast a long runway of 6% average earnings growth for the sector, offsetting some of the valuation downside. Renewable energy has state and federal policy tailwinds. Electric vehicle sales drive our bullish outlook for electricity demand. Safety, reliability, and resiliency are top of mind following extreme weather events and record-breaking electricity demand this summer in Texas and California. If utilities can convince regulators and policymakers to support their growth investments, utilities investors might avoid a worst-case scenario.

Top Picks

Edison International EIX Star Rating: ★★★★ Economic Moat Rating: Narrow Fair Value Estimate: $73 Fair Value Uncertainty: Medium

Edison continues to trade at a sizable discount to its peers despite a growth outlook, 4% dividend yield, and clean energy profile that tops most other U.S. utilities. California’s progressive energy policies and utility rate regulation support Edison’s $6 billion annual investment plan to harden the grid against natural disasters, integrate renewable energy, and support electric vehicle adoption. We forecast 6% annual earnings growth for at least the next five years and similar dividend growth. Edison is one of the few pureplay electric utilities that owns no power generation and has no direct fossil-fuel exposure.

NiSource NI Star Rating: ★★★★ Economic Moat Rating: Narrow Fair Value Estimate: $32 Fair Value Uncertainty: Low

We think NiSource has the best clean energy transition growth in the sector as its Indiana electric business replaces coal generation with renewable energy. Safety investments at its natural gas distribution business also provide near-term growth. NiSource trades at similar valuation multiples and dividend yield as the sector, but we think it should trade at a premium because of its higher long-term earnings growth potential and constructive rate regulation. In November, NiSource’s new CEO plans to announce his long-term strategic plan, which could include divesting some of its small gas utilities.

Dominion Energy D Star Rating: ★★★★ Economic Moat Rating: Wide Fair Value Estimate: $82 Fair Value Uncertainty: Low

Dominion has transitioned to a predominantly rate-regulated utility operating in highly constructive regulatory environments. The company's five-year $37 billion capital investment plan focusing on clean energy supports our 6.5% annual earnings growth forecast. Virginia is the company's most important subsidiary and has the most constructive regulation. Dominion expects 90% of its capital investment in the region will be eligible for rate riders, reducing regulatory risk in an inflationary environment.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IORW4DN3VVC3BC4JO7AQLSJTF4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ODMSEUCKZ5AU7M6BKB5BUC6G5M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TGMJAWO4WRCEBNXQC6RFO5TOAY.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ea0fcfae-4dcd-4aff-b606-7b0799c93519.jpg)