The Glass Half Full Market: Earnings Misses Are Getting More of a Pass

Second-quarter results haven’t actually been impressive, but investors are rewarding them anyway.

Even as stocks bounced from bear-market lows, there was a nagging concern: Would second-quarter earnings derail the move higher?

The worry was inflation and a slowing economy would lead to weak earnings reports that would set the market back.

And in fact, companies aren’t topping analysts’ expectations on earnings by a record margin as they did in 2021.

Despite that, investors are rewarding companies that simply met expectations or that beat by a wider margin than in any other earnings season in the last two years.

“We came into earning season with a glass half empty mindset,” says Steve Sosnick, chief strategist at Interactive Brokers. “We were probably a bit predisposed to think negatively, there were worries about a kitchen sink quarter,” he says, meaning that investors were expecting second-quarter earnings to be the time companies would dump all their bad news at once.

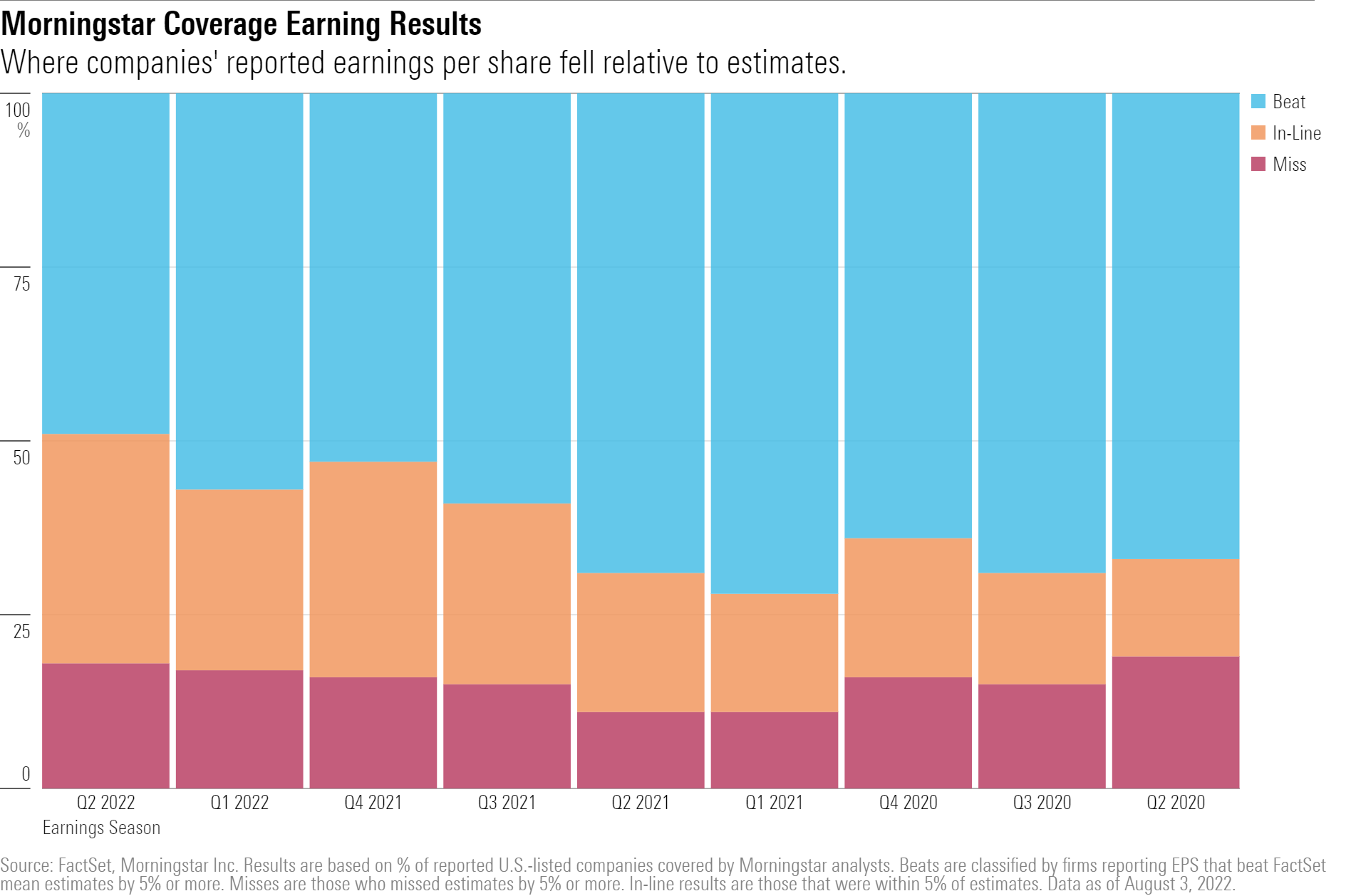

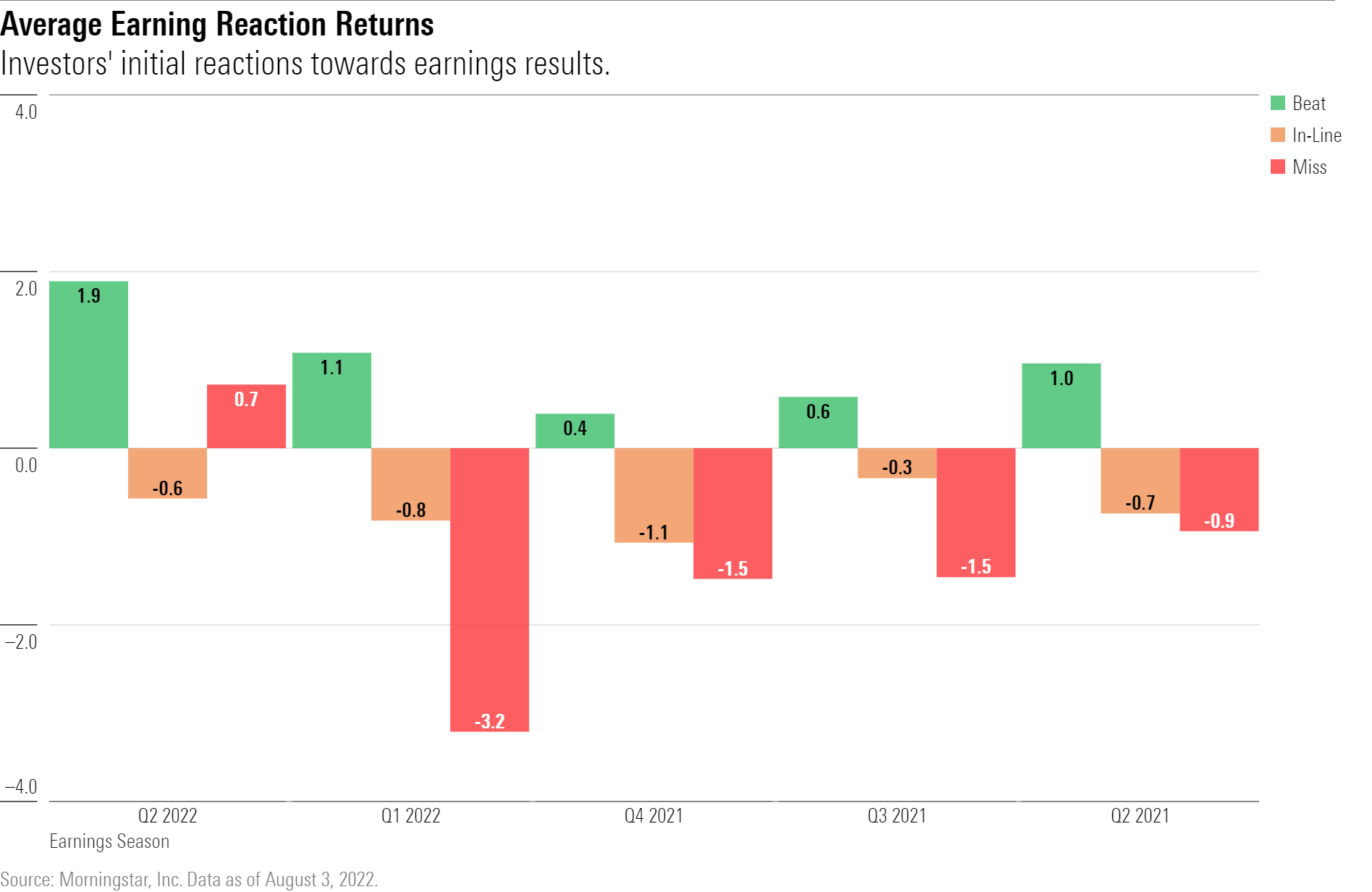

Instead, as of Aug. 3, with about 51% of the 854 U.S.-listed companies covered by Morningstar analysts that have reported second-quarter results, investors have failed to punish any stocks to the same degree they did during first-quarter earnings. The average one-day return following the release of positive results is 1.89%, compared with an average of 0.75% in the last four quarters. For a full explanation of how we calculated the data, see the explanation at the end of this article.

Other Key Takeaways From Q2 Earnings So Far

- Companies that missed earnings estimates actually saw their shares rise by an average of 0.72%, versus an average loss of 1.77% in the prior year for that same group.

- Executives came off as more confident in their guidance and commentaries, leading to investors also sending the stocks that missed earnings estimates higher.

- Of the stocks covered by Morningstar analysts that have reported, only eight fell more than 10% after their earnings results, compared with 32 during the first-quarter earnings season. Taking the biggest hit was reinsurance firm Scor SCRYY, which fell 15%.

- None of the companies that have reported so far saw their stock fall more than 20%. Seven companies fell by that much during in the prior quarter including Under Armour UA, whose shares plunged 25.88%.

- Stocks that had the worst earnings reaction to first-quarter results, the big retailers, have yet to report, leaving the potential for investors' sentiments to sour quickly.

So far fewer companies are actually beating their second-quarter earnings estimates, with only 47% of those who reported doing so. That’s down from the 56% seen in the first quarter, and below the average of 60% for the last four earnings seasons. There’s also been an uptick in the number of companies that failed to meet expectations, with about 19% of missing second-quarter estimates. That compares to an average of 15% in the past year, and is slightly worse than the 18% in the first quarter.

So why are investors cheering second-quarter news when there are fewer earnings beats and more frequent misses?

“Better than feared was key this quarter,” says Sosnick, who points to changing market psychology. When market psychology is good, investors are expecting companies to beat earnings and generally reward that and vice versa, he says. But when market psychology “stinks” as Sosnick sees it now, “the market is just hoping companies make their targets. You don’t need an earnings beat to make results good news,” he says.

That tracks with a rise in number of companies that have met expectations for the second quarter, which is 33% of those that have reported so far. Companies that met expectations had an average earnings reaction return of a decline of 0.57%, which is slightly above the average decline of 0.74% over the previous year.

As for companies that missed expectations and still saw an average earnings reaction that was positive, the implication is that investors were paying attention to more than just beats or misses. Sosnick saw a greater level of confidence in how companies were talking about their goals during second-quarter results commentary.

“Companies lacked clarity, and that was expressed in the first quarter, and that’s why investors came into the second quarter glass half empty,” he says. “Instead, companies seemed more, if not sanguine, a bit more confident in their guidance. Markets like certainty.”

A combination of companies generally meeting expectations, if not beating them at an increased pace this quarter, and more confidence in guidance ranges was enough to turn around market sentiment.

“Investors were much more willing to reward positive news than they were to punish negatives,” Sosnick says. He cited investors’ reactions to bank earnings, which many see as a bellwether for the rest of earnings.

What’s Next?

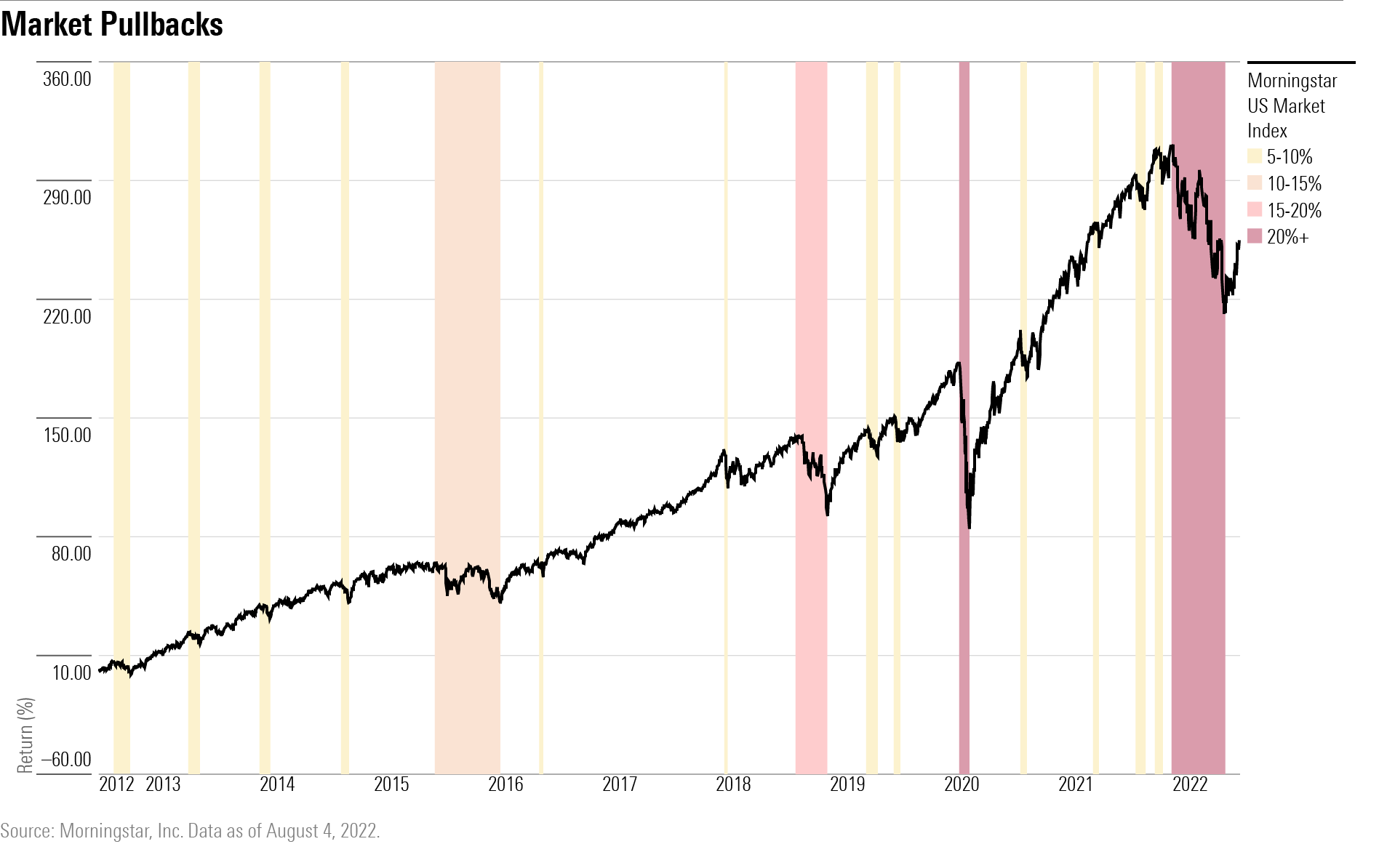

The broad market has rallied 13.9% from its 52-week low on June 16, buoyed by solid earnings news, which has prompted some to think the market has passed its bear-market low. But Sosnick is hesitant to say recent results are an indication that the market is moving higher.

“We’ve made it through the bulk of the earnings season, but the next few weeks are going to be telling as we’re going to hear from the retailers, and I suspect they may tell a different story,” he says.

A big wave of retailers typically reports toward the end of earnings season, many of which were among the companies who had the worst earnings reactions during first-quarter earnings including Target TGT, whose shares dropped 24.93%, and Bed Bath and Beyond BBBY, which fell 23.58%.

Sosnick is also wary of market psychology reversing again, saying that there are still factors that can change sentiment.

“I’m reluctant to say we’ve hit the bear-market low because I’m a big believer of ‘Don’t fight the Fed,’ and they haven’t taken their foot off the brakes yet,” he says, referring to expectations that the Federal Reserve will continue raising interest rates.

“We’re also going to have the other issue of the Fed shrinking its balance sheet, the Fed pumped a lot of money into the markets, and they’ve really only just started withdrawing,” Sosnick says. While the Fed will be shrinking their balance sheet at a very slow pace, Sosnick still sees that as a major headwind in the future.

“They [the Fed] are unlikely to change their stance unless we’re facing a recession, and the bond market is screaming at our face that we’re likely to face one. But stock investors are somehow viewing this as something to be ignored or fine as they expect the Fed to cut rates [in the event of a recession],” Sosnick says. “That’s very much a case of be careful what you wish for.”

Methodology notes:

Analysis was conducted on the 854 U.S.-listed stocks covered by Morningstar analysts as of Aug. 3, 2022. Earnings release dates were pulled for each stock during each earnings period between April 1, 2020 (the start of 2020’s second-quarter earnings season) to Aug. 3, 2022.

Earnings reactions are the one-day return of companies’ stocks of the next available trading day following their earnings release dates. If a company released earnings pre-market or while the market was open, then the return was calculated for that very same day. If a company released earnings results after the market closed, or on a weekend, the next trading day was used to pull the one-day return as the earnings reaction.

Data was aggregated based on the percentage surprise of a company’s earnings per share results. If firms reported actual EPS 5% or more above FactSet mean consensus estimates, it was considered a beat. If firms reported actual EPS 5% below or less than estimates, it was labeled as a miss. If actual EPS was within 5% of estimates, results were viewed as in line.

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PKH6NPHLCRBR5DT2RWCY2VOCEQ.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/54RIEB5NTVG73FNGCTH6TGQMWU.png)