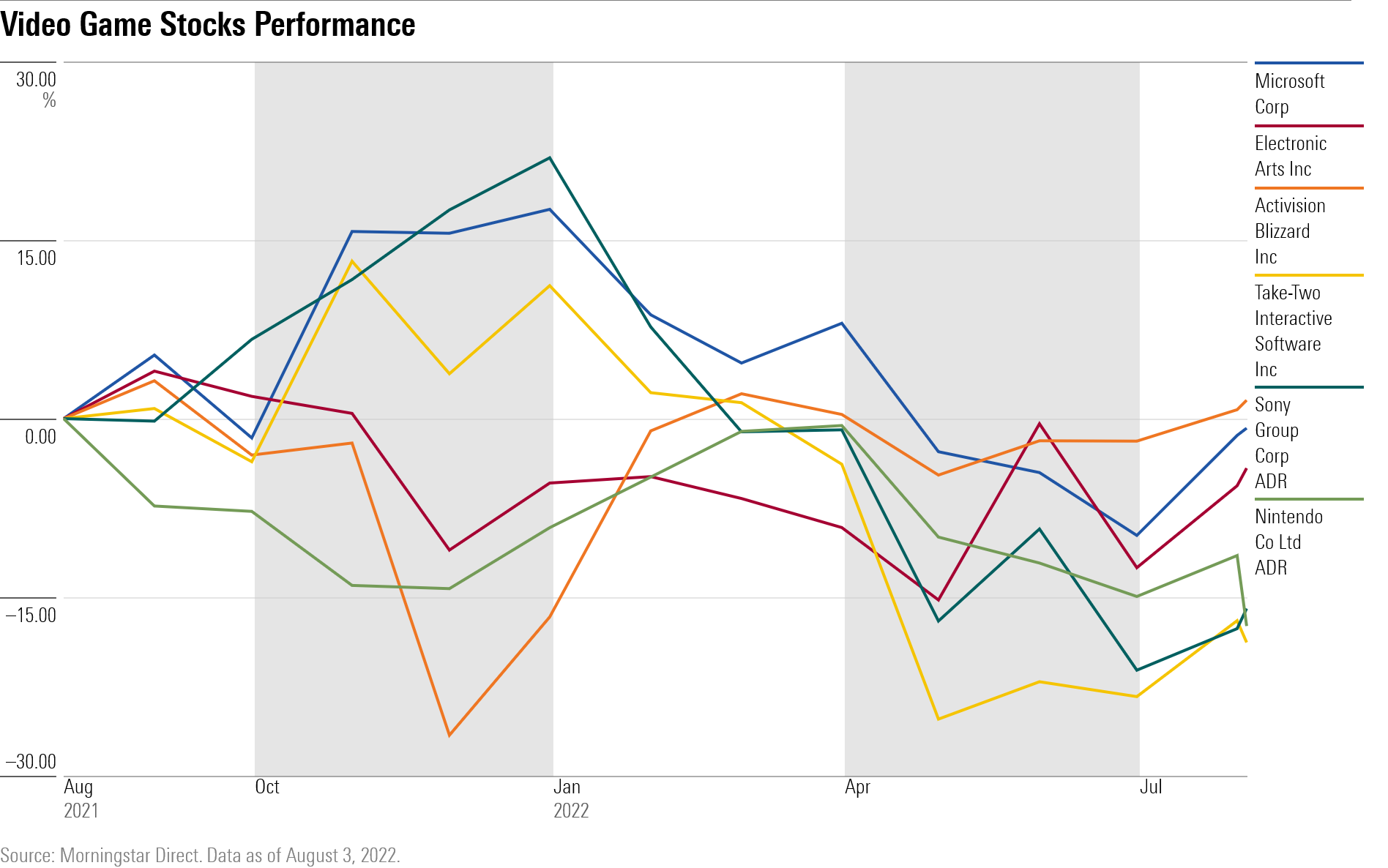

Video Game Stocks Hit by Slowdown in Spending

Electronic Arts in a sweeter spot but fairly valued.

/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)

Even hardcore video gamers have their limits. And that’s affecting growth for the top video game stocks.

Tired of being cooped up indoors for two years, gamers traded in their controllers and the comforts of home for the great outdoors, music festivals, and other experiences as pandemic restrictions eased. The high cost of essentials such as food and gas is also cutting into spending on games and accessories.

“The surge in new players and higher engagement from 2020 and 2021 has leveled off,” wrote Mat Piscatella, a games industry analyst at NPD Group, which does market research, in a recent report. “We now see more entertainment opportunities competing for consumer attention and dollars.”

This shift has been evident as several leading companies in the video game space have reported earnings in recent weeks and noted that gamers spent less money overall in the second quarter. Some said gamers played less. Among those seeing this trend:

- Sony Group SONY

- Microsoft MSFT

- Nintendo NTDOY

- Activision Blizzard ATVI

- Electronic Arts EA

Adding to the industry’s woes are production halts due to COVID lockdowns in China, which has crimped the supply of next-generation consoles. Sony’s PlayStation 5 and Microsoft’s Xbox Series X were launched two years ago but are still hard to come by. Semiconductor shortages are also affecting the supply of personal computers. The rollout of new big-name games has been delayed, too, as development teams adjusted to work-from-home conditions under during the pandemic.

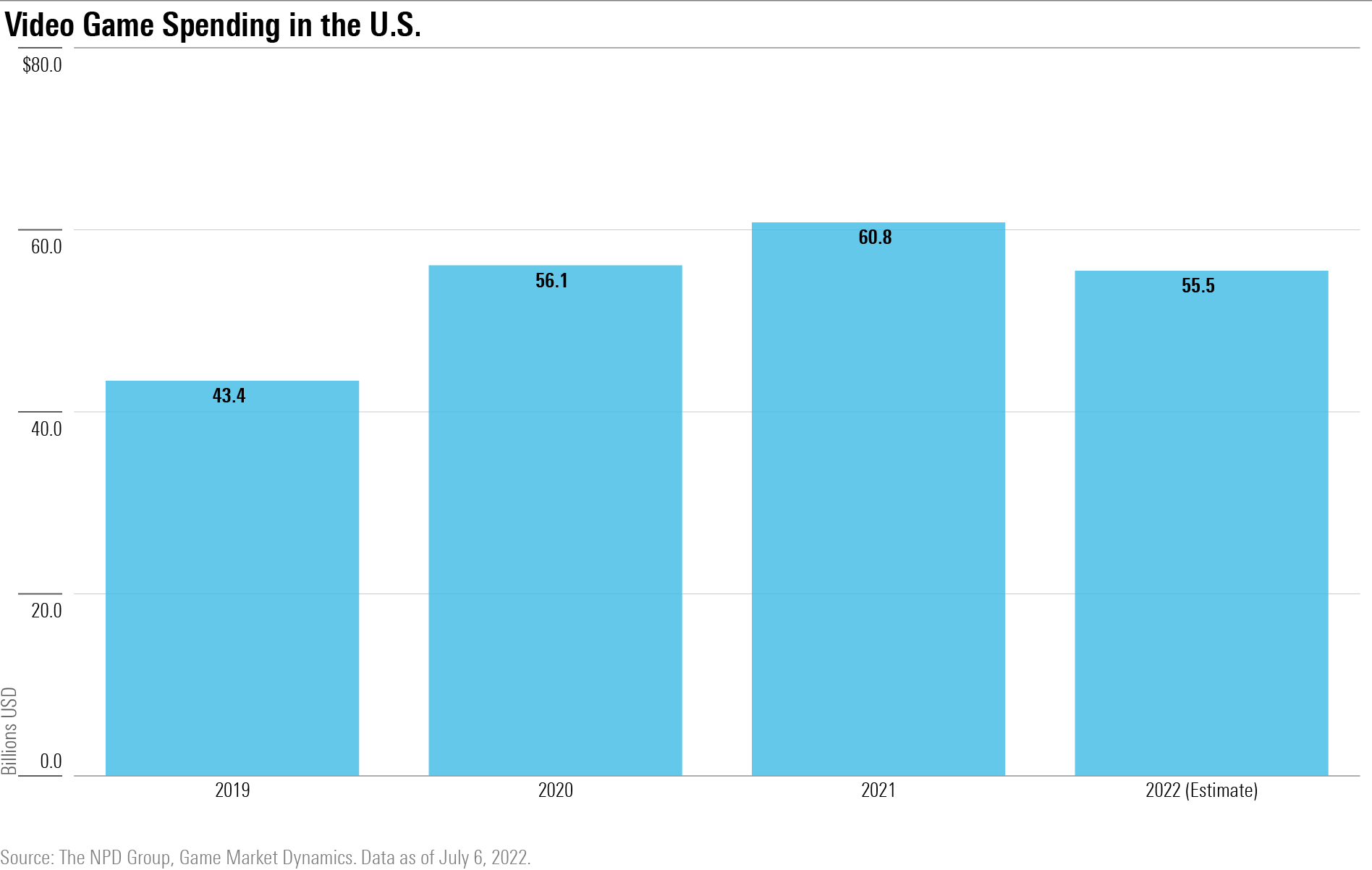

Video Gamers Spending Less

Consumer spending on video gaming products in the U.S. fell by nearly 13% to $12.35 billion in the second quarter of 2022, compared with the $14.13 billion posted in the same period a year ago, according to NPD. Spending decreased in all but one category: nonmobile subscription services. For the full year, spending is expected to decline by nearly 9% to $55.5 billion. That marks a less than 3% gain from the prepandemic level of $43.4 billion.

“Long-term growth trends remain in place,” says Neil Macker, senior equity analyst at Morningstar. “But the second half looks weak across the board with no pickup in demand.”

Forecasting Growth for Video Game Stocks

Amsterdam-based market research firm Newzoo revised its outlook for worldwide spending on video gaming to $196.8 billion this year from an earlier estimate of more than $200 billion in response to the challenging environment. That represents just a 2% increase from 2021.

More than half the growth globally is expected to be generated by games played on mobile platforms, increasing by 5% to $103.5 billion. The personal computer market is expected to increase by 1.6% to $40.4 billion, while console games will decline 2.2% to $52.9 billion. Newzoo forecasts global spending on gaming will reach $225.7 billion by 2025, representing a compounded annual growth rate of 4.7% between 2020 and 2025.

“This signals our belief that the games market will continue growing healthily in a postpandemic world, albeit at a slower pace than during the pandemic,” Newzoo’s lead market analyst for games Tom Wijman says.

Considered “console first” gaming markets, North America and Europe are expected to show flat growth this year. “Strong mobile growth and, to a lesser extent, modest PC growth in these regions are the only factors offsetting a steep overall decline,” says Newzoo’s Wijman.

No one expected the torrid pace of spending growth the past two years to continue. Yet neither did anyone foresee the extent of the slowdown that’s occurred, especially in an industry long thought to be somewhat insulated from broader economic downturns. developments. The latest results highlight the unsettled economic backdrop, but also point to shifting industry dynamics.

From `Hit-Driven' to `Free-to-Play' and `Live Services'

The industry has moved from the “hit-driven movie-studio like” model of 10 to 15 years ago when people bought the latest console and the hottest games, says Morningstar’s Macker. Now “live service” games in which content is updated regularly and that are typically “free-to-play” on mobile devices, with companies relying on players to make in-game purchases and microtransactions, are all the rage.

The new postpandemic developments are catching some in the industry off guard.

Sony, maker of the popular PlayStation console, saw sales decline in its Gaming and Network Services division by nearly 12% to JPY 604 billion yen for the quarter ended in June from a year ago, mostly due to decreasing software sales. Operating income plunged 31% to JPY 53 billion yen. Gaming and Network Services is Sony’s largest division, generating more than JPY 24 billion in sales in 2021. It lowered its full-year 2022 sales guidance for the division to JPY 3.62 trillion yen from 3.66 trillion, and cut its outlook for operating income by 16%, or JPY 50 billion yen, to JPY 255 billion.

The company said total gameplay time for PlayStation users declined 15% year on year in the fiscal first quarter and fell 10% in June versus the same period a year ago, noting “this is a much lower level of engagement than we anticipated in our previous forecast.” Executives cited reduced COVID-19 infections in some of its major markets created more opportunities for gamers to go outside as the reason for the drop.

Sony is maintaining its forecast for sales of 18 million units of their PlayStation 5 console for fiscal 2022 and said it would take action to increase user engagement in the second half by releasing major software titles, making the PlayStation 5 more available, and promoting its new PlayStation Plus subscription service.

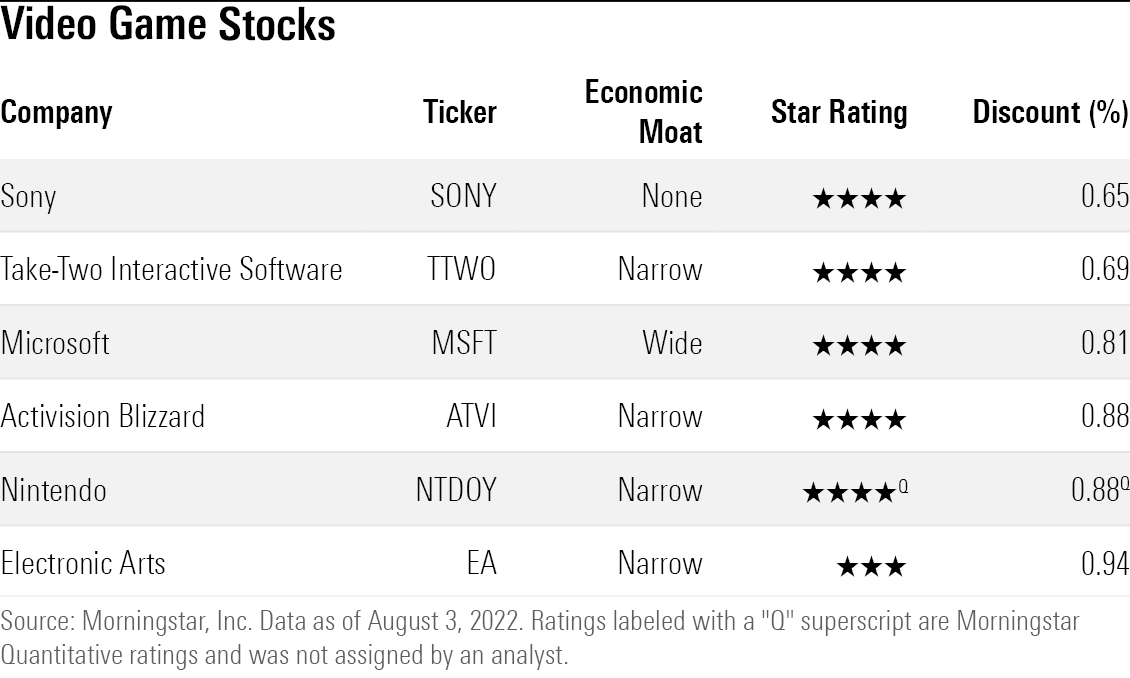

Morningstar director of equity research Kazunori Ito maintains 4-star Sony’s business portfolio is resilient and under appreciated. At $85.88, Sony’s stock recently traded at $85.88 a share, a 35% discount to his fair value estimate of $133.

Xbox maker Microsoft reported its overall gaming revenue declined by 7% in its fiscal 2022 fourth quarter. Xbox hardware revenue slid 11%, while content and services revenue fell 6%, driven by lower playing hours and lower monetization in third-party and first-party content, partially offset by growth in Xbox Game Pass subscriptions.

The crown jewel of Microsoft is its Azure cloud service, the centerpiece of chief executive Satya Nadella's makeover of the technology giant, says Dan Romanoff, senior equity analyst at Morningstar. He considers Microsoft a wide-moat 4-star stock. It is trading at a 20% discount to his $352 fair value estimate.

Still, he points out, gaming represents 9% of Microsoft’s nearly $200 billion in total revenue and is growing at low double-digit rates. Romanoff has “no confidence that the gaming segment can generate excess returns over the next 10 years.” The high costs traditionally associated with gaming networks -expensive leading-edge consoles, games, headsets, and other accessories- may not be able to be maintained over the next decade.

Microsoft is in the process of acquiring pure-play video game developer Activision Blizzard, whose titles include Call of Duty, World of Warcraft, Diablo and Candy Crush. Activision reported a 28% drop in revenue in its second quarter ended June 30, citing weak sales and a lack of user retention in its Call of Duty franchise. It was its second straight quarter of weakness. Only its King Digital Entertainment segment with its free-to-play games that generate revenue from in-game sales and advertising on mobile platforms posted year over year growth.

Morningstar’s Macker believes Microsoft’s acquisition of Activision will be completed but likely not until mid-2023. In January, Microsoft agreed to pay Activision shareholders $95 a share in an all-cash transaction. Berkshire Hathaway’s Warren Buffett BRK.A is betting the deal goes through: he bought 9.5% of Activision’s stock throughout the spring as the price dropped below the purchase price.

Nintendo's sales dropped nearly 5% in its fiscal 2023 first quarter as production problems hampered availability of its popular Switch console and sales from mobile devices tanked nearly 17%.

“Unit sales for the entire Nintendo Switch family of systems declined by 22.9% year over year to 3.43 million units,” the company said. “In the first quarter of last fiscal year, titles from other software publishers helped drive hardware sales, particularly in Japan, but with the semiconductor shortages affecting production this first quarter, unit sales of hardware declined year over year.”

A bright spot: digital sales increased by 16% year over year and accounted for more than half of total software sales for the Nintendo Switch platform.

Another Pure play video game developer, Electronic Arts, found itself in the sweetest spot of the pack. It focuses on live services and sports games, such as FIFA and Madden NFL, Battlefield, and its newest, Apex Legends, played on mobile devices. The company posted better-than-expected results for its fiscal 2023 first quarter, with revenue rising 14% year over year, though its overall “net bookings,” as sales of digital products and services are known, dropped 3% year over year. Console net bookings fell by 8% due to fewer game launches.

Morningstar's Macker called it a "solid quarter," but considers the 3-star stock fairly valued. At a recent price of $133, Electronic Arts trades close to his fair value estimate of $142 per share, limiting its upside potential.

Macker’s best bet: Take-Two Interactive Software TTWO, which completed its acquisition of Zynga in late May, which will put it at the forefront of mobile gaming, where most of the industry’s profits are being generated.

“Its recently completed purchase of Zynga has transformed the firm into the traditional publisher most leveraged to mobile,” Macker says. “The $11.2 billion deal is the largest-ever closed video game acquisition, but we think Zynga will engender enough opportunities and benefits to justify the high price tag. One key opportunity will be developing mobile versions of Take-Two's premier franchises, including Grand Theft Auto.”

The company closed at $129.81 per share on Wednesday, trading at a 30% discount to his fair value estimate of $185.00. Take-Two is the video game company with the best potential for appreciation, Macker contends.

Take-Two will report its fiscal 2023 first quarter results Aug. 8.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PLMEDIM3Z5AF7FI5MVLOQXYPMM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/I53I52PGOBAHLOFRMZXFRK5HDA.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CEWZOFDBCVCIPJZDCUJLTQLFXA.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)