Few Places to Hide for Non-U.S. Equity Funds in Second Quarter

Value-focused and China-heavy funds fared best amid the global selloff.

/s3.amazonaws.com/arc-authors/morningstar/b0c51583-b9a2-49eb-9a8f-5f25a8bda4a3.jpg)

Value-leaning and China-heavy non-U.S. equity funds managed to stay afloat a bit better than their growthier and China-shunning peers in 2022’s second-quarter selloff.

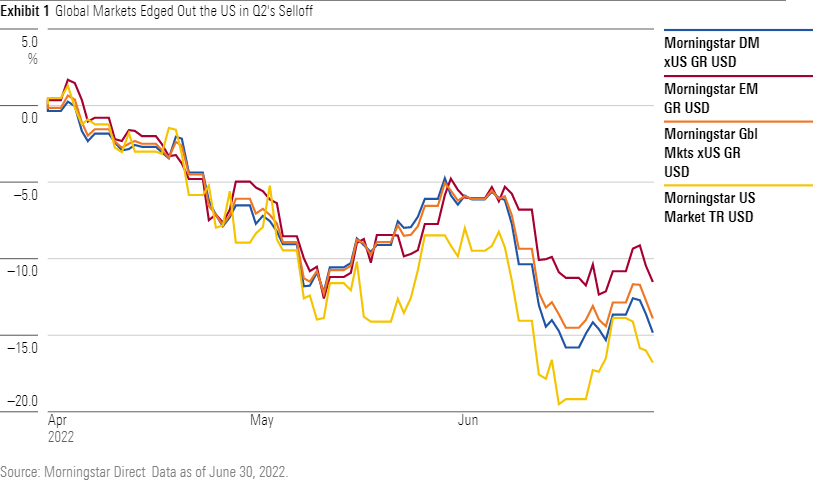

The Morningstar Global Markets ex US Index fell 14.0% in the second quarter after dropping more than 5% in the first quarter. Emerging-markets stocks held up better than developed-markets peers, as the Morningstar Emerging Markets Index declined by 11.6% compared with the Morningstar Developed Market ex US Index’s 14.9% drop. Both managed to edge the U.S. market, however, as the Morningstar US Market Index declined 16.9%.

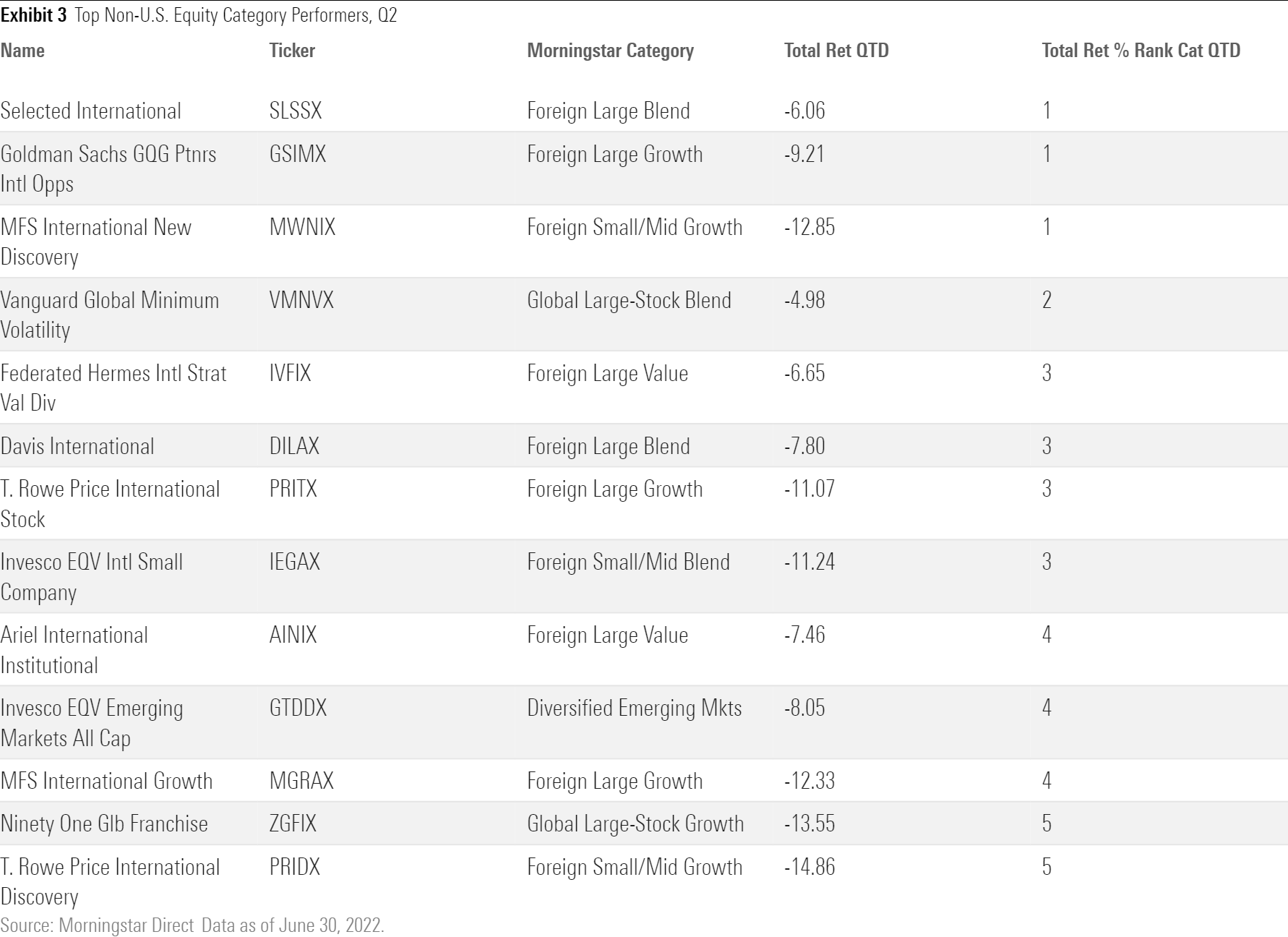

China was the only sizable country to post a gain for the quarter. The Morningstar China Index rose 2.7%, as a number of its top holdings like JD.com JD, Baidu BIDU, and Meituan MPNGY each rose in price following steep first-quarter declines. Just three non-U.S. equity strategies covered by Morningstar analysts gained ground in the second quarter, and all three—AMG Veritas China MMCFX, Matthews China MCHFX, and Matthews China Dividend Investor MCDFX—are China-focused offerings. China funds still have plenty of ground to make up, though, as the Morningstar China Index remains down more than 30% over the trailing 12 months. Large exposures to Chinese stocks finally paid off for both Davis International DILAX and Davis Global DGFAX, two funds with Morningstar Analyst Ratings of Bronze whose China stakes hindered returns in the last couple of years. Each has more than 25% in China and landed in the top quintile of its respective category.

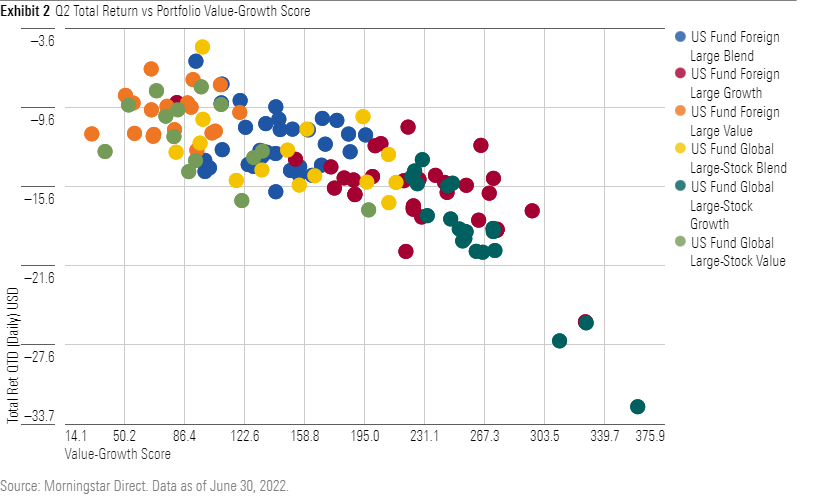

Whether a fund tilted toward growth or value ultimately determined its performance fate, as shown above. Value funds did better than blend funds, which lost less than growth funds; and within each category, value-leaning funds tended to beat their peers.

The growth selloff continued from the first quarter. Rising interest rates, inflationary pressures, and a muddy demand outlook weighed on higher-multiple stocks. The Morningstar Global Markets ex US Value Index shed 12.5% in the quarter, much less than the Morningstar Global Markets ex US Growth Index’s 14.8% drop. Funds with heavy growth exposure took it on the chin, including Morgan Stanley Institutional International Opportunities MIOIX, which lost 27.3% in the quarter following a more than 25% decline in the first quarter. Several of its fast-growing top-10 holdings, including MercadoLibre MELI, Shopify SHOP, and Spotify SPOT, dropped by more than 35%. MercadoLibre, as well as U.S.-based highfliers Amazon.com AMZN and ZoomInfo ZI, also dragged down the similarly aggressive Baron Global Advantage BGAIX, which dropped more than 32%.

Value-leaning funds, on the other hand, held up relatively well. T. Rowe Price International Stock’s PRITX 11.1% loss in the quarter, for instance, was much less than the category average’s 16.6% because it is more mindful of valuations than many of its foreign large-growth Morningstar Category peers and owned stocks like Dutch conglomerate Prosus PROSY, which gained 30%. Similarly, MFS International New Discovery’s MWNIX quality-focused process and 4% cash stake helped it land in the top 1% of foreign small/mid-growth category. It still lost 12.9% in the quarter, but that was considerably less than its average rival’s 19.2% decline.

Chinese exposure alone was not enough to offset growth headwinds, though. Artisan Developing World APHYX, for instance, had a fourth of its assets in Chinese stocks as of March 2022 yet lost 24.4% and ranked in the bottom 1% of the diversified emerging-markets category because the aggressive growth funds’ top four non-Chinese holdings—Airbnb ABNB, Nvidia NVDA, MercadoLibre, and Sea LTD SE—which represent over a fourth of the fund’s assets, each dropped by more than a whopping 44%.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b0c51583-b9a2-49eb-9a8f-5f25a8bda4a3.jpg)