The Best S&P 500 Funds

The tip of the indexing pyramid.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Winnowing the Field

Note: This is an updated (and much-revised) version of an article from Nov. 8, 2021, titled “The Best and Worst S&P 500 Funds.”

At first glance, selecting an S&P 500 fund is a bewildering task. Morningstar’s database contains more than 250 mutual funds and exchange-traded funds with “500” in their names.

However, many of those offerings, particularly among the ETFs, are not conventional S&P 500 funds. They short the market, or they are leveraged, or they seek to improve upon the benchmark. Examples of the latter include funds that hold equal positions in each stock instead of weighting by market cap, or funds that invest in a portion of the index, such as Invesco S&P 500 Momentum ETF SPMO.

Other funds roughly echo the S&P 500 but do not attempt to mimic the benchmark exactly. The most notable case is Fidelity ZERO Large Cap Index FNILX. Although the fund invests in “stocks of the largest 500 U.S. companies,” it is not in fact an S&P 500 clone. Thus, while the index gained 28.7% last year, Fidelity ZERO Large Cap Index placed 2 percentage points lower, at 26.7%. An unpleasant surprise for those who had not been paying attention!

Many of the remaining S&P 500 funds cannot be purchased by do-it-yourself investors. They either sell only to institutions, or they distribute through financial advisors. Determining the status of such funds is laborious. It is easy enough to recognize the intent of “institutional” or “retirement” share classes, but what about funds that are marked with a “G” or a “K” or a “Y”?

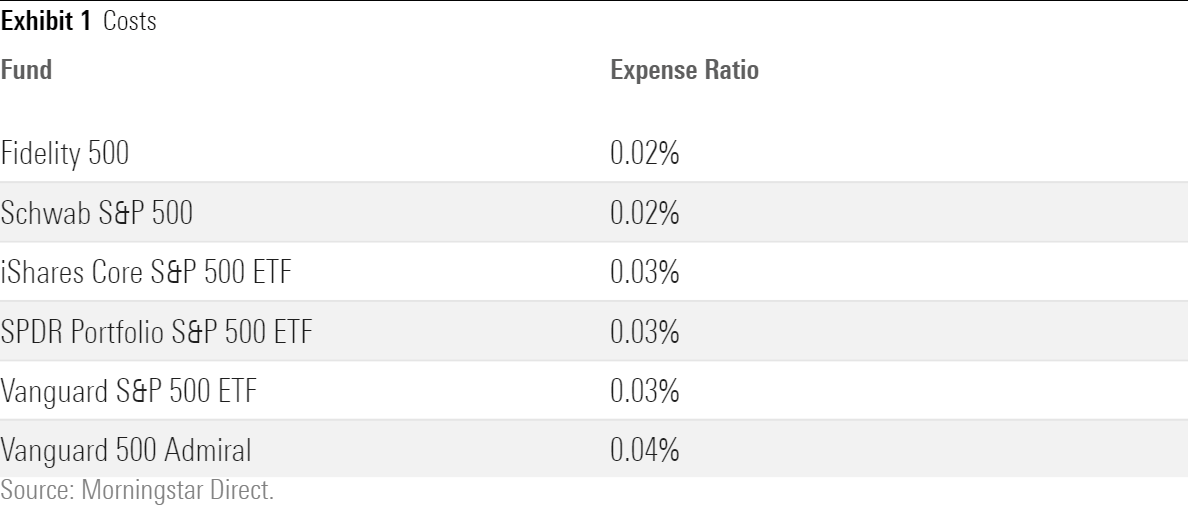

The Cheapest 6

Eventually, after much data mucking, I narrowed the field down to 17 true S&P 500 funds that are available for retail investors who buy their funds directly. Eleven of those funds can safely be discarded, as their expense ratios are above 0.05%. By ordinary standards, that expense cutoff is exceedingly low. However, with cheaper options readily available, there’s no reason to pay more.

The finalists consist of three mutual funds and three ETFs. The table below ranks them in order of their 2021 expense ratios. Unsurprisingly, these funds dominate the marketplace, controlling two thirds of all retail S&P 500 indexed assets. Not only are they cheaper than the competition, but the six funds are also sponsored by industry leaders. They face no danger of languishing for lack of attention.

If all S&P 500 funds were identically managed, those expense ratios would tell the entire story. Subtracting each fund’s costs from the index’s theoretical return would provide the take-home performance. That precept largely holds; although some benchmarks are difficult to replicate, because they contain a great many securities and/or inflict high transaction costs, the S&P 500 offers an easy target. Professional managers who have enough assets to put to work, as those who run these funds certainly do, have little trouble emulating the benchmark.

Missing the Mark?

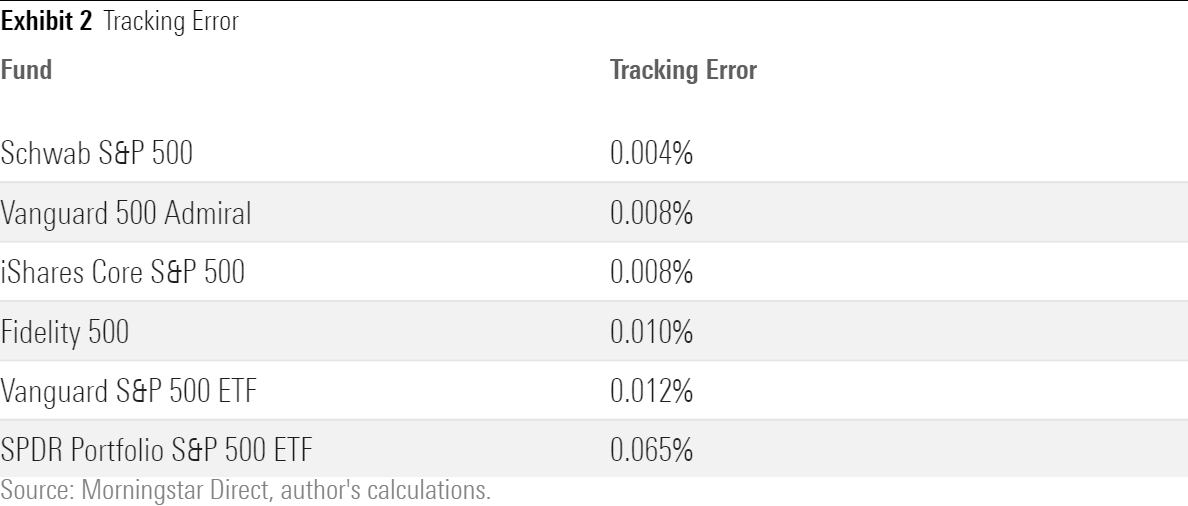

Still, all index funds occasionally wander. We can measure their deviations by assessing their tracking errors. To calculate tracking error, we add a fund's expense ratio to its reported total return. This gross return is then compared against the benchmark's results, with any differences classified as tracking errors.

The following table shows the annual tracking error for the six funds, computed by averaging tracking error over each of the past 10 calendar years. Again, the funds are presented in order of their rankings.

Those amounts are tiny! Aside from SPDR Portfolio S&P 500 ETF SPLG, which recorded a somewhat larger but still modest average annual tracking error of 0.06 percentage points, the finalists routinely landed within a single basis point of their targets. Tracking errors for the also-ran S&P 500 funds can be substantially larger, but among the elite they are barely worth mentioning.

Considering Returns

Any discrepancies among the funds' total returns come from the combination of expense ratios and tracking error. The relationship is not predictable, because while expense ratios can only lower a fund's returns, tracking error works in both directions. Sometimes, when one index fund bests another, the winner deserves blame rather than credit. It erred but got lucky.

Nevertheless, evaluating the funds’ total returns is a valid exercise. After all, shareholders ultimately spend what their funds earn. The next table provides each fund’s average annualized 10-year return, calculated from January 2012 through December 2021. Also depicted is the result for the index itself.

(The 10-year numbers differ by more than one would expect, given how closely the funds’ expense ratios and tracking errors cluster. The divergence occurs because during the early years of the study period, some of the funds had higher expense ratios than they do today.)

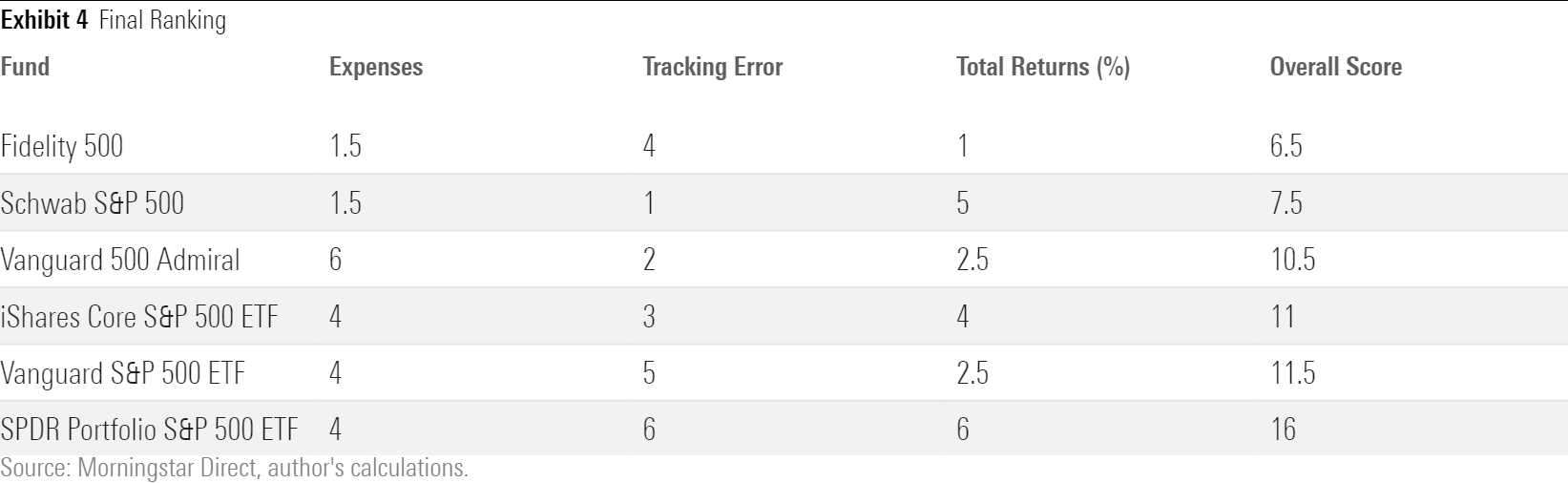

To determine the top overall S&P 500 fund, I combined the rankings for each of the three tables.

Fidelity 500 Index FXAIX triumphed by a whisker, closely followed by Schwab S&P 500 Index SWPPX. The last time I addressed this topic, Fidelity’s fund was just shy of posting a 10-year record and thus was ineligible for review. It amply made up for the missed opportunity.

Wrapping Up

Two additional items are worth noting. First, the differences between the funds are extremely slight. When putting new monies to work, one might reasonably select Fidelity or Schwab’s funds instead of, say, the SPDR portfolio, but I certainly wouldn’t advocate switching assets that have already been invested. Doing so is unlikely to be worth the bother.

More important yet, for those holding their index funds in a taxable account, is avoiding Uncle Sam’s tax bill. In fact, such investors will wish to tweak this column’s list, by favoring the three ETFs. Mutual funds that index the S&P 500 are highly tax-efficient. However, because of their construction, ETFs are even more so. For those with taxable assets, the tax-dodging properties of the leading S&P 500 ETFs outweigh any theoretical advantages possessed by their mutual fund rivals.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-09-2024/t_e87d9a06e6904d6f97765a0784117913_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)