What Should Accompany Stocks: Cash or Bonds?

The benefits of taking the middle ground.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Theory Into Practice

Common sense suggests that investors should offset their risky securities with a safe security. Academics concur. For example, William Sharpe won a Nobel Prize for demonstrating that portfolios require only two positions, one being a fund that contains all stocks, and the other a "risk-free investment." The allocations will differ, per individual circumstances, but not the positions themselves.

Although Sharpe’s model has since been attacked on the grounds that it contains several unrealistic assumptions, few have quarreled with its principle that stocks should be cushioned by something secure. Sharpe, however, did not specify what that holding should be. His concept was hypothetical: a security with “zero risk” that pays the “pure interest rate.”

In this world, as opposed to Sharpe's hypothetical construct, all investments contain risk. (As the joke goes, economists do enjoy assuming the ladder.) Even if a debt obligation existed that could never default—which is regrettably not the case—its payment schedule would introduce uncertainty. When interest rates shift, an existing note or bond will gain or lose value. Changes in the inflation rate can also affect the prices of such allegedly "safe" securities.

Although there are no true risk-free investments, securities issued by the United States Treasury are acceptable substitutes. They can default, but they are highly unlikely to. And, by and large, they perform well when stocks do not. The question then becomes, which version of Treasury is most appropriate for hedging an equity portfolio: cash, intermediate-term notes, or long bonds?

The First Test

To answer: There are two reasons to prefer one type of Treasury to another. The first is long-term gain. All things being equal, seek the security with the highest return. (Never let it be said that I overlook the obvious.) The second is bear-market performance. As the risk-free assets exist to cushion losses, how they act during downturns is more important than how they behave in bull markets.

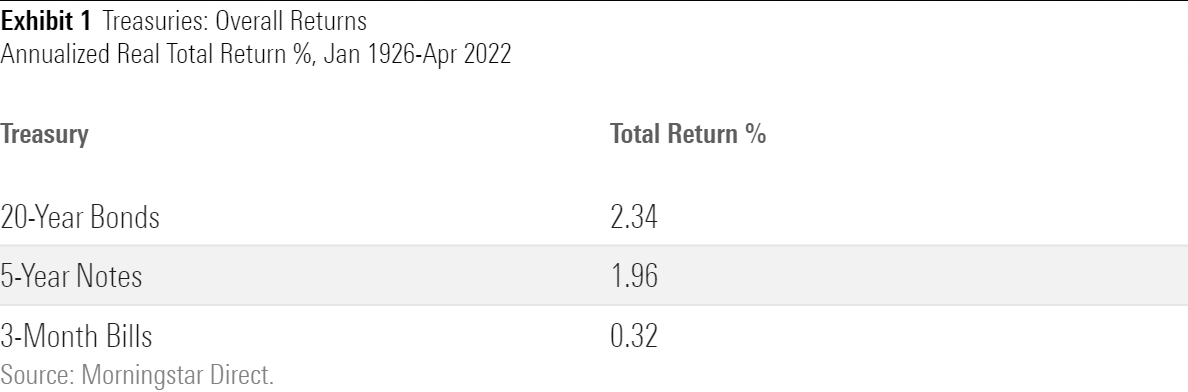

That can readily be determined, as I have at hand nearly a century’s worth of performance figures for 1) three-month Treasury bills, 2) five-year Treasury notes, and 3) 20-year Treasury bonds, courtesy of Ibbotson Associates. The table below displays the average annualized return for each of the three risk-free candidates since 1926. Each performance, for this and subsequent tables, is shown in real terms—that is, after the effect of inflation.

Bonds and notes recorded similar returns. However, the gap between those two investments and that of cash is large. If the risk-free asset accounts for 40% of the investor’s portfolio, as with a balanced fund, then the difference between holding bonds or notes and holding Treasury bills amounts to about 0.75 basis points per year–a significant handicap. Settling for cash has been a costly decision.

The Second Test

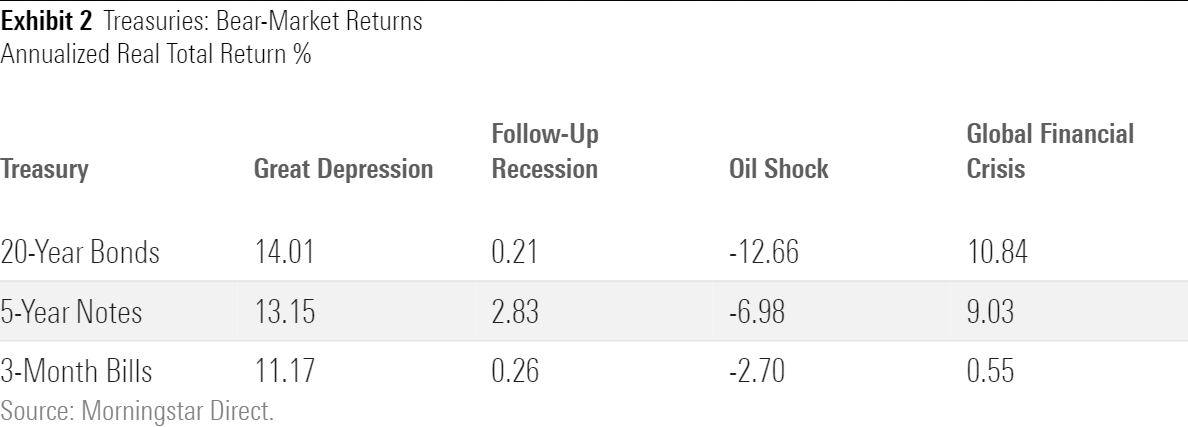

That said, if cash has reliably beaten notes and bonds during the worst of stock-market times, its weaker long-term results may be forgiven. By my count, there have been four truly awful bear markets since 1926. I list them below, along with the stock market’s real cumulative total return during those periods.

- The Great Depression: September 1929-May 1932, -79.00%

- The follow-up recession: March 1937-March 1938, -50.04%

- The 1973-74 oil shock: January 1973-September 1974, -51.82%

- The global financial crisis: October 2007-February 2009, -51.04%

This is how each version of Treasury obligation performed during those periods.

The outcomes are difficult to summarize. One time all Treasuries performed well, another time they all struggled, on yet another occasion they all dogpaddled, and during the final trial bonds and notes profited but cash didn't. In particular, the contest between the ends of the barbell was mixed. Bonds once whipped cash and once edged it, while cash once whipped bonds and once edged them.

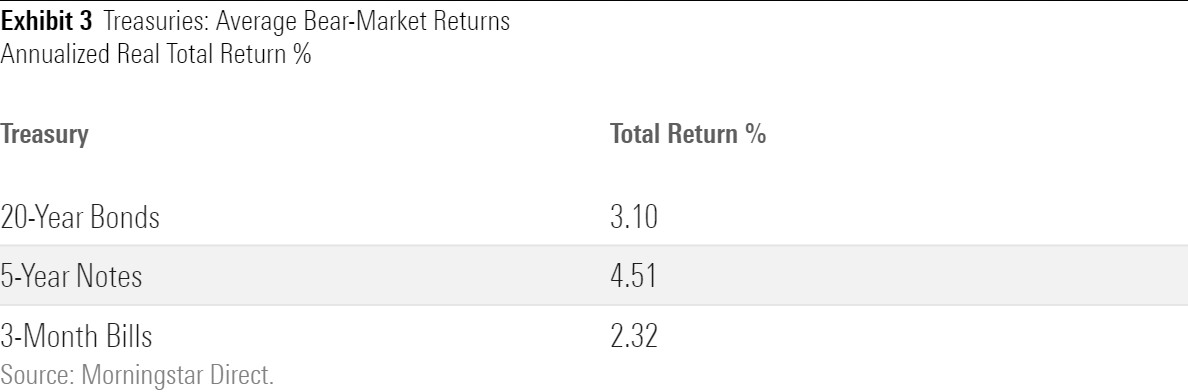

That said, while the bear-market totals do not support holding either bonds or cash, the middle ground appears decidedly more attractive. During the three instances when either bonds or cash triumphed, five-year notes acted more like the winning choice than they did the loser. And during the fourth period, when each version of Treasury performed similarly, notes led. Consequently, the average bear-market result for five-year Treasuries was comfortably ahead of its rivals’.

The Upshot

To address the headline’s question of which investment better accompanies stocks, I would split the difference by replying, “Neither cash nor bonds are ideal. Choose notes instead.” Happily, that is how mutual fund and exchange-traded fund shareholders have invested, as bond funds possesses twice the assets of money market funds, and intermediate-term funds are by far the most popular type of bond fund. Indeed, the biggest bond fund, Vanguard Total Bond Market II Index VTBNX (as with the Mad Max movies, the sequel surpassed the original), pretty much fits the bill.

Normally, I would hedge my bets by stating that, although it seems that five-year Treasuries combine the best of both worlds, it does not hurt to diversify among the available options. But doing so here seems pointless. In almost a century, five-year notes have answered every call, staying close to long-term bonds when Treasuries have rallied, avoiding much of their volatility when Treasuries have struggled, and reliably providing bear-market protection. Just keep things simple.

There is one caveat: spiking inflation. In three of the four bear markets, there was no advantage to holding cash rather than notes. There were also, however, no inflation worries. Prices barely rose during 2008, were exactly flat in 1937, and plunged at the onset of the Great Depression. Only during 1973-74 was inflation a concern. That was the one instance in which Treasury bills performed best.

Thus, while intermediate-term Treasuries should typically be used to offset the risk of a stock portfolio, there is some logic to holding a shorter portfolio today: say, a mix that consists half of five-year notes and half of Treasury bills. Of course, there is no guarantee that the next few years will emulate the bad old days of the mid-1970s, but stagflation has become a realistic possibility. It might be worth forgoing some return to mitigate that potential problem.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YQGRDUDPP5HGHPGKP7VCZ7EQ4E.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)