Is an Economic Recession Likely? (And How Much Does It Matter?)

Here's why investors are focused on the wrong question.

/s3.amazonaws.com/arc-authors/morningstar/010b102c-b598-40b8-9642-c4f9552b403a.jpg)

With high inflation sticking around longer than expected, and the Federal Reserve embarking on an aggressive path of raising interest rates, concerns about an economic recession are on the rise.

It’s a legitimate worry that a recession could be a byproduct of the Fed’s quest to tame inflation. For now, a recession in the next two years is not in our base case economic forecast, though its probability is meaningfully above zero.

More importantly, we think the intense focus on the question of “will a recession occur?” misses the point. Recessions come in many different varieties, and if a recession does occur, we think it will be relatively short and mild.

What Is an Economic Recession?

A recession occurs when the economy shrinks. It is generally defined as at least two consecutive quarters of decline in gross domestic product, or GDP, which functions as a measure of economic health. When economists talk about "official" or define recessions, they're often referring to the dates of a recession determined by the National Bureau of Economic Research. The last recession, caused by the pandemic lockdown, began in February 2020 and ended in April of that year, according to the NBER.

Will There be an Economic Recession in the Next Few Years?

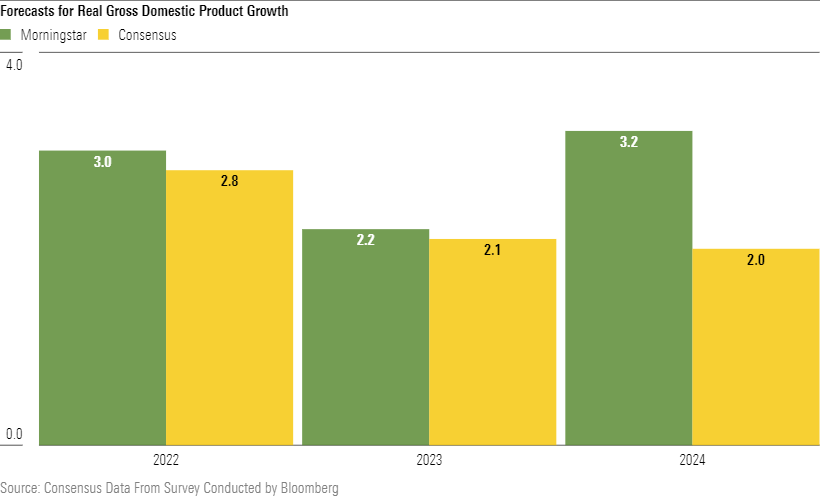

For now, an economic recession isn’t in our base case. Although we’ve recently lowered our near-term GDP forecasts owing to headwinds from the war in Ukraine and other factors, we’re still expecting growth to remain in positive territory. Our near-term views are broadly in line with consensus estimates.

The fundamentals underpinning economic expansion were strong going into 2022, with consumers maintaining a healthy appetite to spend and normalization from the pandemic providing further tailwinds. But aggressive monetary policy tightening is dampening the outlook for economic growth, driven by the Fed’s quest to quell high inflation. Ultimately, we think the inflation problem will not be so severe as to force the Fed to engineer a recession. There is a small possibility that the Fed could trigger a recession by mistake.

Interest rates have been raised twice, lifting the federal-funds rate from zero to 0.75%, with an aggressive half-point increase in early May. In the bond market, investors are expecting the Fed to boost interest rates by another half of a percent in June and for the funds rate to be around 3% by the end of this year.

Very Unlikely That Q1 GDP Dip Marked Start of Recession

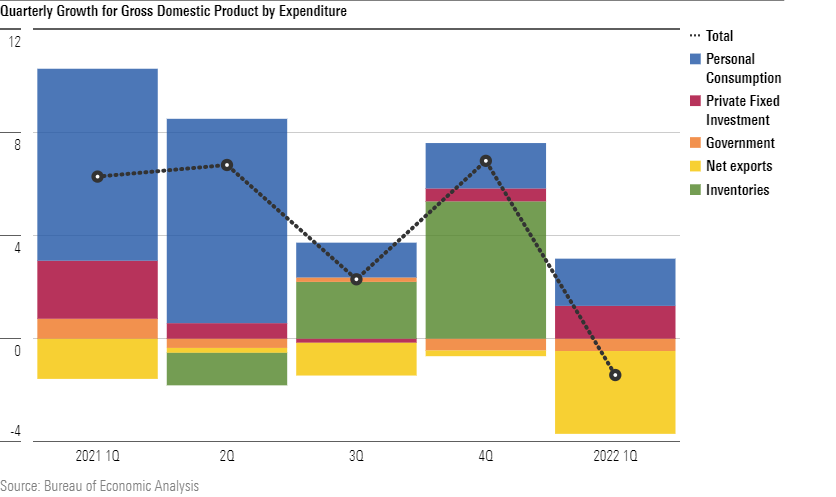

Real GDP fell 0.36% in the first quarter of 2022, or 1.4% annualized. This is the first decline since the start of the pandemic. However, we don't think this marks the start of an economic recession, as the decline was driven mostly by net exports, which is one of the most volatile components of GDP. The decline was due to a rise in imports, which counts as a negative in the GDP calculations.

Final domestic demand, which is consumption plus fixed investment, including spending by businesses to grow production capacity, grew at a healthy 2.5% annualized despite supply-side headwinds.

It’s unusual for GDP to decline when domestic demand is increasing, especially given the large increase in labor supply in the first quarter. As puzzling as the dip in GDP is in light of the broader data, we suspect later estimates to the first quarter numbers will be revised upward. Regardless, growth for the rest of 2022 should stay in positive territory.

Where Could We Go Wrong?

There are two main areas where we could go wrong in our expectation that a recession won’t occur. The first scenario is where expected inflation gets too high. Expectations of high inflation can be a self-fulfilling prophecy, and once that takes place, difficult to dislodge.

In order to tame high inflation in this scenario, the Fed would be forced to raise interest rates much more aggressively than is currently expected in order create a significant slowdown in the economy. This might entail a mini version of the 1981-82 recession, which was severe but relatively short-lived. Once the Fed eased off on rate hikes, the economy quickly returned to expansion mode.

A second scenario is if the Fed is too aggressive and boosts rates more than needed to tame inflation. This is plausible because of the long lags between when monetary policy is implemented and when it effects the economy, which makes overshooting possible. Most of what the Fed is doing today in terms of tightening won’t show up in terms of economic activity until 2023. The Fed can only make an educated guess as to how much tightening will be required to bring inflation back down without tipping the economy into recession.

Economic Recessions Come in Many Different Varieties

Ultimately, we think investors are overly focused on the binary question of “will a recession occur?” A more important question to ask is “will a severe, long-lasting recession occur?” Economic recessions come in many different varieties, so merely asking the question of whether a recession will occur isn’t very meaningful for investor outcomes or the long-run trajectory of the economy.

If an economic recession did occur in the next two years, we think it would be relatively mild and short. For example, in the scenario of a recession caused by Fed over-tightening, the the central bank could make a course correction which would kick the economy back into expansion.

We see very little reason to think a repeat of the severe, long-lasting Great Recession would occur. This event still looms large in the psychology of investors. But we shouldn’t take the Great Recession to be a template for every recession. Many post-WW II U.S. recessions were accompanied by very temporary impacts to economic activity and asset prices.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/F2S5UYTO5JG4FOO3S7LPAAIGO4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/7TFN7NDQ5ZHI3PCISRCSC75K5U.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/QFQHXAHS7NCLFPIIBXZZZWXMXA.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/010b102c-b598-40b8-9642-c4f9552b403a.jpg)