When Everything Declines at Once

From the archives: Past correlations are a hazardous guide for the future.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Opening Note: This column was originally published on March 27, 2019. While I would love to bask in the glow of its foresight, the sad truth is that I had partially forgotten its lessons when this year arrived. Therefore, I have been more surprised than I should have been by the recent and simultaneous decline in global stocks, global bonds, cryptocurrencies, and gold bullion. I should have revisited this topic sooner!

Kitchen Chat

Every Morningstar floor has a soda dispenser, coffee machine, and sink. The other day, I went to get some water. The dispenser was broken. No worries, I would pour some coffee instead. Foiled again: That machine was shut down and, it turns out, so was the sink. Everything was out.

This puzzled me. Sure, the soda dispenser, as with the copy machine and my car, is unreliable. It was no surprise to see it shuttered. The coffee machine is more dependable but occasionally misfires. It was therefore possible to envision both contraptions being simultaneously out of commission. But the sink? It had never failed before. Peculiar that the one time that it did, the two appliances were also not working.

As you may already have surmised, there was nothing strange about that situation at all. The three items were all served by the same water pipe, so when it became clogged, none of them could function. Plumbing 101.

My mistake was basic. I had not wondered what physical relationships might exist between the dispenser, machine, and sink. My expectations were formed entirely by what I had observed. Using the past as my guide for how the kitchen’s units behave had sufficed for several years, but when something unusual occurred--in this instance, the water pipe choking--history failed.

History’s Limits

By now, you may be thinking that your author is a special sort of idiot. That could indeed be true, but I will offer two defenses. First, I had never directly thought about the subject. My views had been formed subconsciously. Second, a similar mistake is routinely made by otherwise intelligent (and wealthy) people, and by professionals who serve them, in the business known as “investment advice.”

I refer to correlations. When allocating assets, it is customary to consider the possibility that future returns may differ from those of the past and to adjust one’s forecasts accordingly. Such efforts occur less often with standard deviations and correlations. For the most part, even among institutions, what happened before is expected to happen again.

In other words, the estimates of asset-class correlations that underlie investment portfolios, even when made by highly sophisticated parties, tend to be created as I did my kitchen calculations. Watch what transpires over several years, assume that pattern will continue, and be surprised--even shocked--if something occurs that has never occurred before.

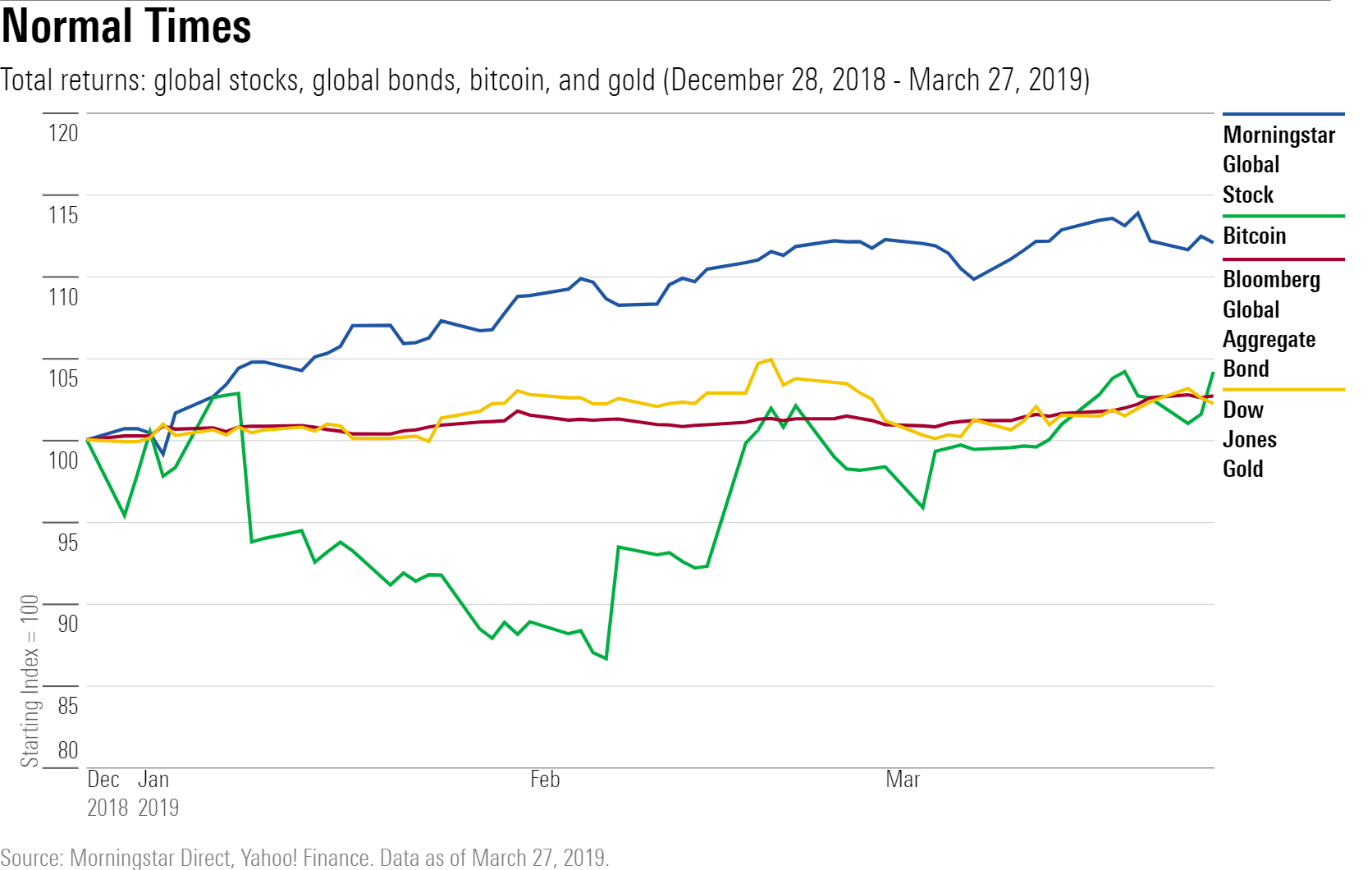

Usually, the pattern is that there isn't a pattern. The following chart shows how global stocks, global bonds, gold, and bitcoin performed in the three months before this column was originally published. As it happened, global bonds and gold moved together (somewhat unusually), but otherwise the four assets behaved differently.

Adjusting the Analogy

This isn’t a criticism. Unlike with my kitchen example, wherein slight effort upgraded my mental model, it’s difficult to see how investment professionals could improve. Determining the meaningful connections between the three kitchen items is straightforward. Not so, for example, in attempting to foresee all circumstances that might simultaneously torpedo U.S. stocks, gold bullion, and mortgage bonds.

Worse, the financial markets are self-referential. The soda dispenser can’t be bothered with how the coffee machine is acting. Investment participants, however, are sentient, meaning that they react not only to what occurs outside of asset prices but also to changes within asset prices. They are susceptible to contagion. Even if analysts could accurately map every economic relationship between assets--an impossible task--their predictions would be derailed by investor behavior.

(The problem increases for the special case of very large funds that make very large wagers. One of the reasons that the hedge fund Long-Term Capital Management imploded was that other institutions knew how it was invested. When LTCM began to struggle, its rivals sold any positions that LTCM held--in effect, running for the exit door. Their trades depressed the prices for LTCM's holdings, thereby accelerating the vicious pricing circle.)

Remembering the Foundation

Where investors do deserve blame, sometimes, is for taking their imperfect methods too seriously. It is one thing to recognize that, in the absence of a better approach, assuming that the future will resemble the past is a good starting point. Doing so outperforms the null assumption. It is quite another to treat correlations as if they measure something tangible and the investment task as if building a bridge.

Few if any investment professionals will confess to such a sin. They realize that their inputs are only estimates--just ask them. And I believe them, to a point. They realize the assumptions that support their tools. However, when doing prolonged computations, as with asset-allocation optimization software or value-at-risk assessments, it's easy to forget the foundation's instability. All too often, the answers to the calculations are regarded as solutions, not suggestions.

Reasonable minds can differ about the usefulness of quantitative routines that rely upon asset-class correlations. They don’t appeal to me, but many Morningstar researchers disagree. (The disclaimer at bottom strongly applies to this column.) What cannot be questioned is that mathematically derived asset allocations should also be appraised qualitatively.

Mental Models

In, particularly, their protections. Investors rarely fail to envision a portfolio’s rewards. The reason they invested in risky assets in the first place was the chance of achieving higher gains than if they held cash. In my experience, though, many do not consider how their portfolios might flop. What economic and/or financial-market conditions would be particularly harmful?

Conducting such exercises strikes me as more valuable than putting portfolios through quantitative tests. Once again, there is no escaping the past; as with hard-edged calculations, soft assessments begin with history. They, too, are imperfect. However, I find them to be more useful than black-box results because they provide a framework for thinking about adverse outcomes. They help with investment discipline.

Among the situations to be envisioned are: 1) recession; 2) an inflationary surge; and 3) widespread investor panic, perhaps due to market dysfunction. Those are merely brief examples. Outlining the various ways by which a portfolio might head south, all at once, is a topic for a future column. This article merely intends to persuade that such a thing can be likelier than one would have believed.

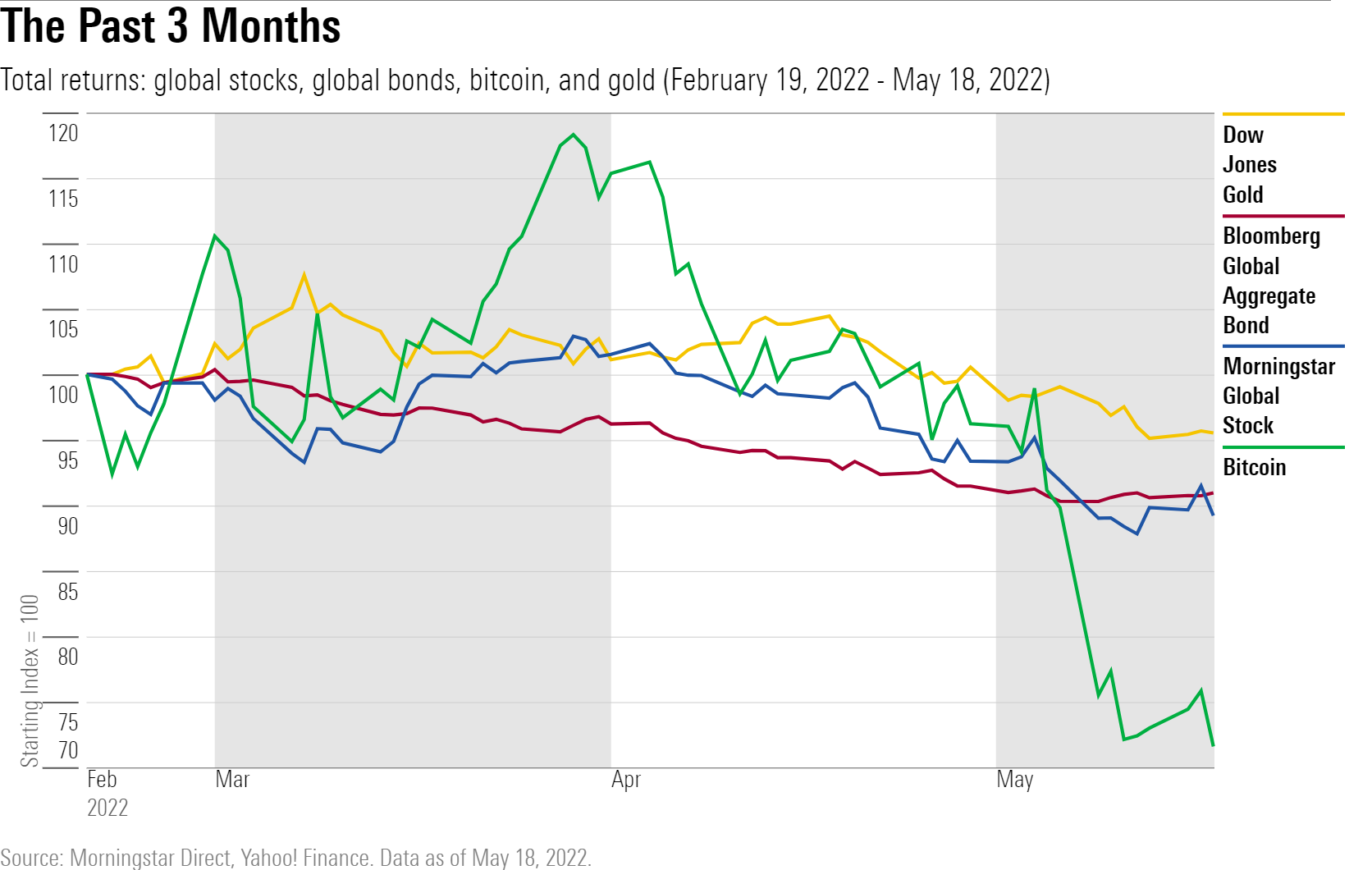

Cue recent performance. Since April began, all four assets have moved together, regrettably in the wrong direction.

Concluding Note: The answer to what might cause everything to fall at once, it turns out, is 2) an inflationary surge, along with the potential fear of 1) recession. At least this time around.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)