What Are Real Yields and Why Do They Matter to Stocks?

Real yields have been pointed to as a culprit in 2022's stock market selloff.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

As stocks have sold off this year, fingers have been pointing to a new culprit: rising real yields.

Real yields are a relatively obscure bond market indicator. At the most basic level, real yields are the returns that a bond investor earns from interest payments after accounting for inflation. So, why would rising real yields be bad for the stock market?

It's a question even longtime observers are asking. The answer, unfortunately, is "it depends."

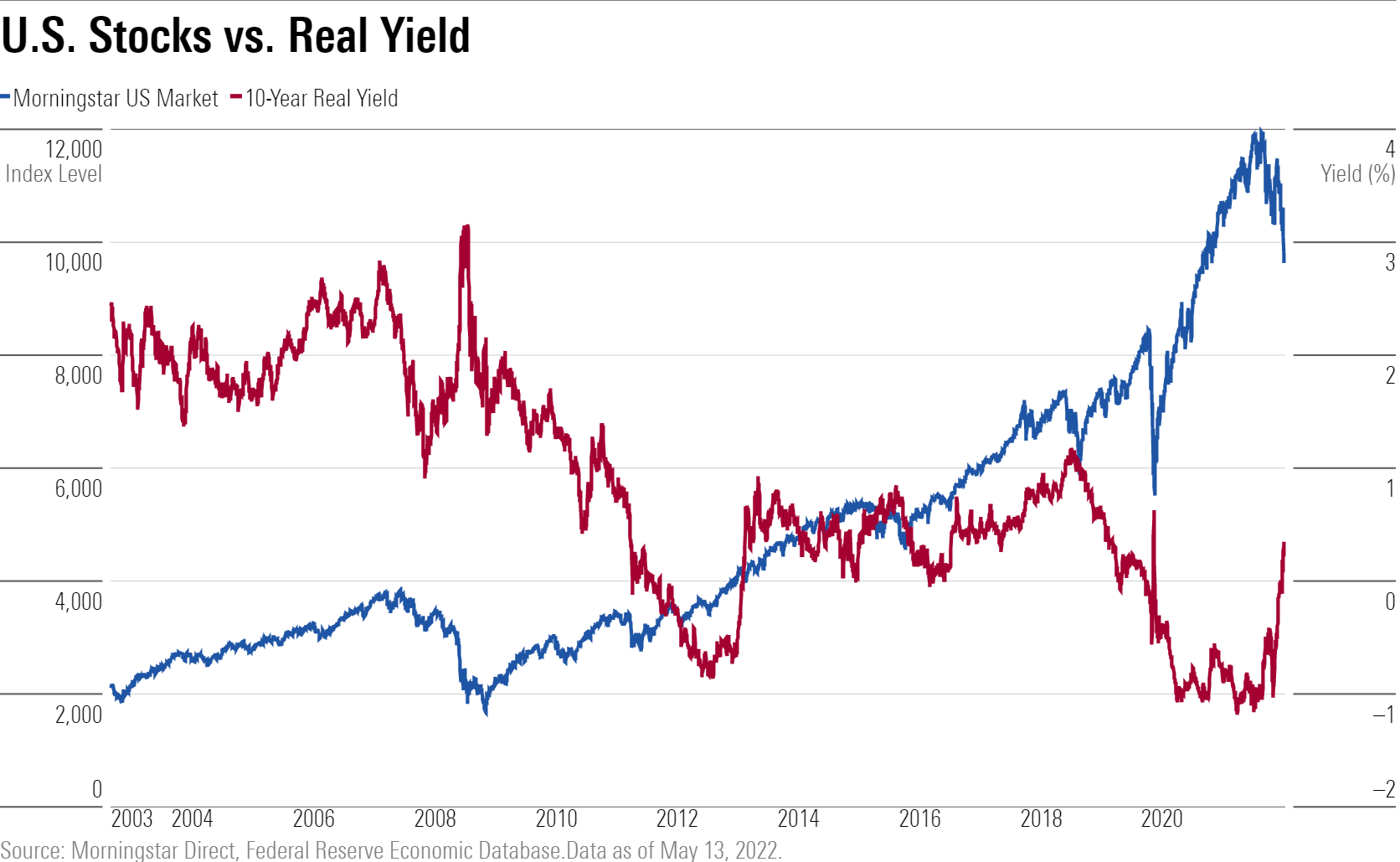

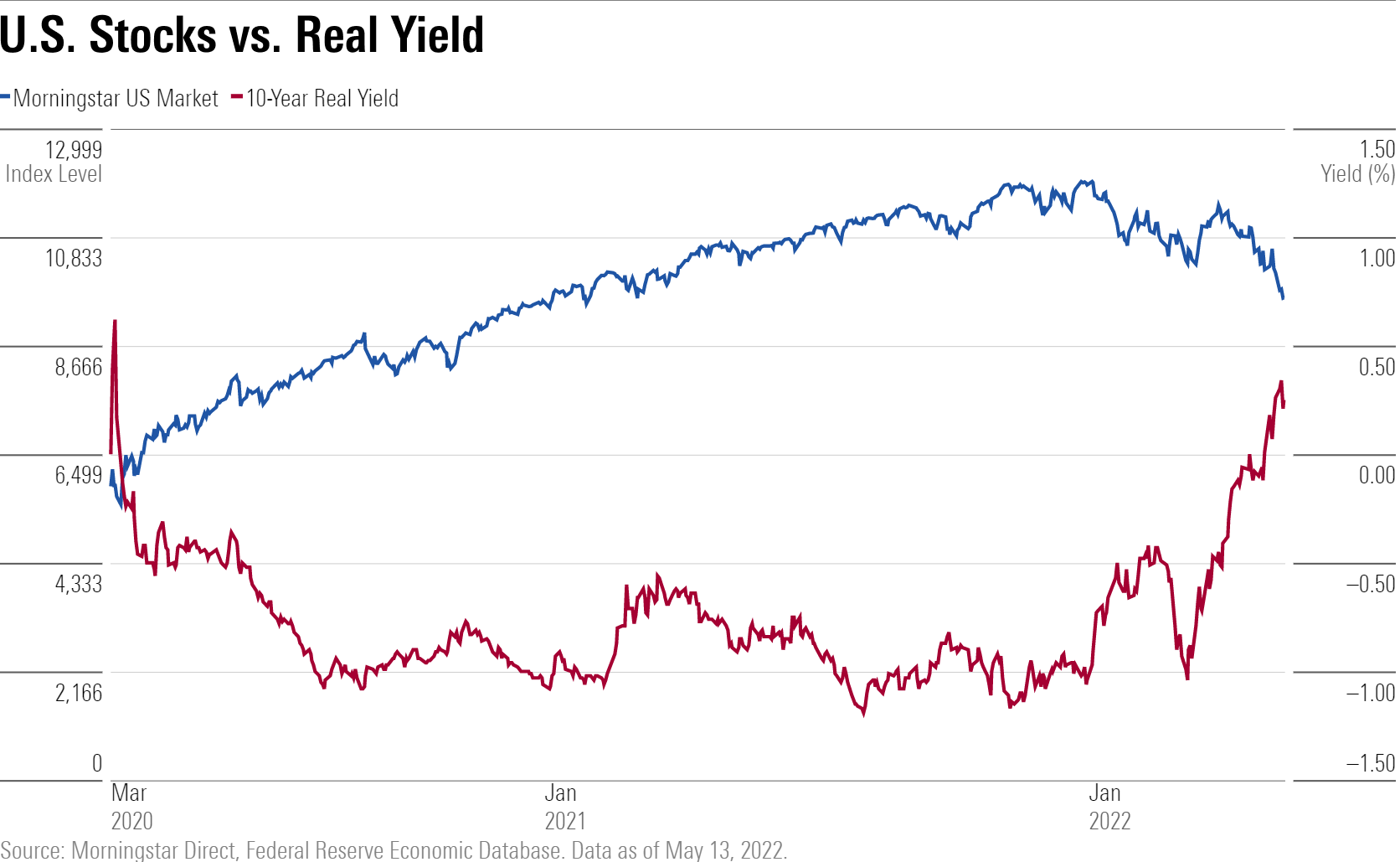

History offers a mixed picture around this indicator. The bottom line is that while rising real rates can at times be a negative sign for stocks, in the past, equities have still done well when real rates are rising and at higher levels than they are today.

But in the current environment, where interest rates were at rock-bottom and stock valuations high at the end of 2021, rising real rates across the board have been one of the factors leading to a repricing of stocks to sharply lower levels.

Why Do Interest Rates Matter for Stocks?

There's no question that interest rates matter a heck of a lot to stocks. Here are four basic reasons why:

1) matter at the big-picture level, when it comes to their impact on the economy, which in turn filters through to the profits that companies make. Rising interest rates act as a brake on economic growth, which in turn can slow profits, and therefore can be a negative for the stock market. (Of course, some companies are more sensitive to the ups and downs of the economy than others, depending on their particular business lines.)

2) When bonds are offering higher interest rates, those yields can make fixed-income investments more attractive to investors. At the same time, when yields are higher on safer bond investments, stocks—which are a riskier investment—need to offer higher returns to compete. Bonds look more attractive than stocks in this environment, until stock valuations fall.

3) Real interest rates can also have a direct impact on stock valuation estimates, according to some in the markets. Valuation models incorporate interest rates into the assessment of how much a stock's future earnings are worth today. When rates rise, it diminishes the value of those future earnings and thus reduces the value of the stock. Analysts point to this dynamic as being a prime catalyst in the selloff of technology and other fast-growing companies whose value is heavily dependent on earnings growth far off into the future.

4) Yet another avenue for rates filtering through to the stock market is another in-the-weeds—but very important—concept: equity risk premiums. The equity risk premium is the return an investor expects to earn above that of a risk-free investment. Another way of looking at it is that the equity risk premium is the reason that investors own stocks; in order to offset the risks of owning stocks, an investor expects to earn more than they would on a safe U.S. government bond.

The calculation for the equity risk premium generally involves subtracting the 10-year real yield from expected returns on stocks. When real yields move higher, that lowers the equity risk premium, which means stocks are less attractive.

How Do You Calculate Real Yields?

A real yield is calculated by subtracting the expected inflation rate from a bond's nominal yield. Real yields can be positive or negative, depending on the combination of the two. The question is which inflation rate to use.

Because real rates are a forward-looking measure, using the government's reported inflation data won't help; it's a backward-looking measure.

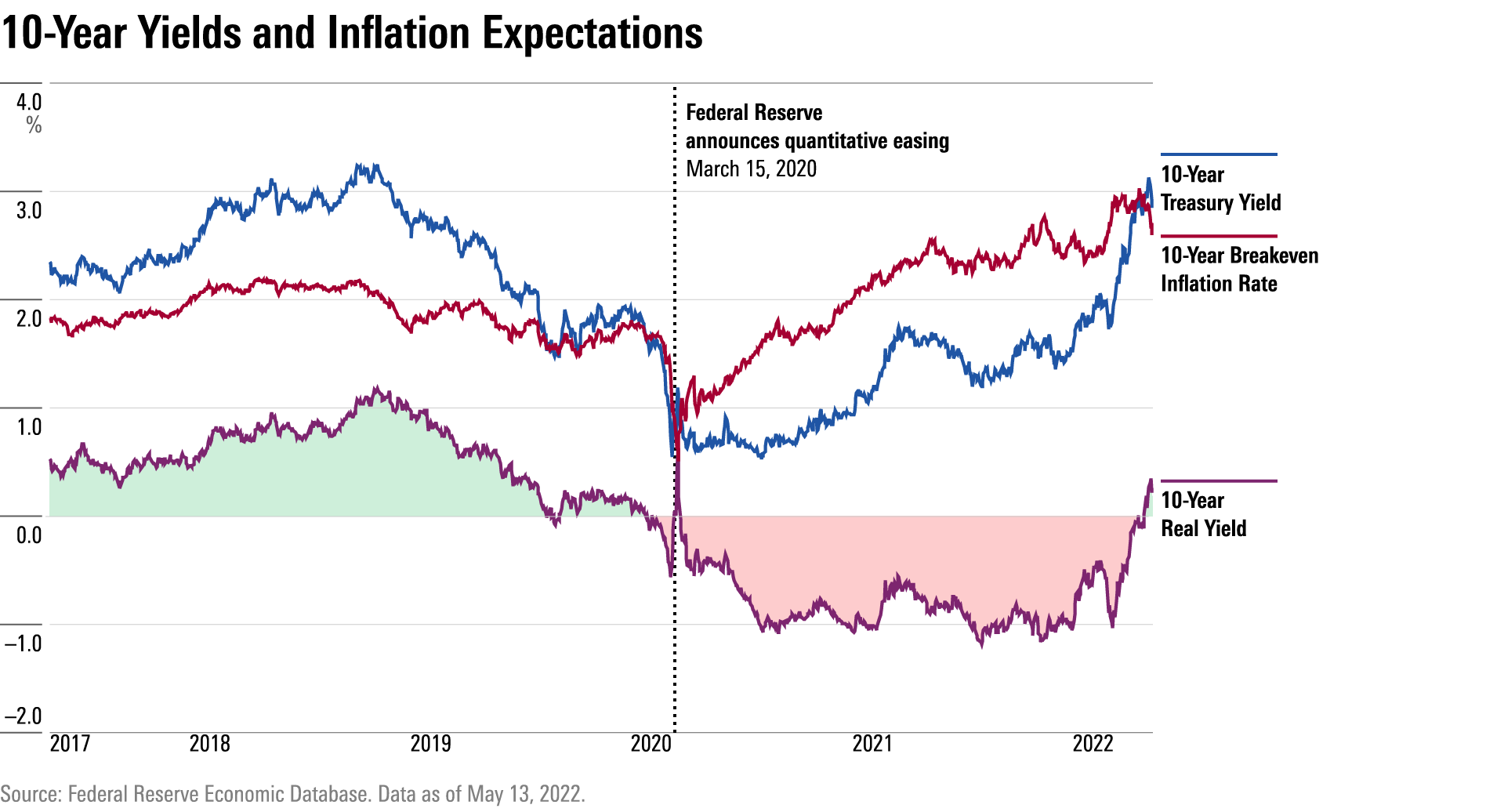

For that reason, calculating real yields requires yet another step: looking to the Treasury Inflation-Protected Securities market. TIPS provide a reading on inflation expectations known as the breakeven rate. For example, to see what the market's expectation is for inflation over the next 10 years, investors look at the difference between the 10-year nominal Treasury yield and the 10-year TIPS (that's known as the 10-year breakeven rate). Right now, the 10-year breakeven rate is 2.69%. With the regular—aka nominal—U.S. Treasury 10-year note yielding 2.84%, the 10-year real yield is 0.15%.

Most of the time, real yields are positive. But in unusual circumstances, real yields can go negative. That's been the case for the past two years. This was the result of the Federal Reserve's quantitative easing efforts to support the economy during the pandemic recession through massive purchases of bonds in the market that had the effect of pushing yields down well below the long-term trend for inflation of roughly 2% per year.

How Did Negative Real Yields Affect Investors?

In a more normal environment than the one seen after the pandemic, the calculus might be 2% expected inflation and a 4% Treasury yield, making for a real yield of 2%. "If you want to earn more than 2%, you go out on the risk curve," into investments such as equities, says Steve Sosnick, chief strategist at Interactive Brokers.

However, for the past two years, "you had the situation where we had positive levels of inflation and interest rates near zero, so you couldn't earn a positive rate of return without assuming some risk," Sosnick says. "If you wanted safety it was going to cost you purchasing power."

"You had no real choice but to move up the risk curve, and that's why real yields get blamed,' for the stock selloff now that they are moving higher, Sosnick adds.

How Did Negative Real Rates Affect Stocks?

Barry Knapp, director of research for Ironsides Macroeconomics, says that on the surface, the biggest beneficiaries in the stock market would have been economically sensitive companies, which would benefit from lower rates. But that wasn't the case the past two years.

"What do these asset purchases do for stocks? They don't help economically sensitive stocks, but they do help those with bondlike characteristics," says Knapp. "You wouldn't think of mega-cap technology stocks having bondlike characteristics, but they have monstrous cash flow and buy back a ton of stock," he says.

He points to Apple AAPL stock, which finished 2021 at a price/earnings ratio of 30. That level would usually be found on a fast-growing company, but Apple is posting earnings growth of around 10%, he says. "But they have this monstrous, stable cash flow, and (Apple stock) started to act like bonds when you drove real yields down to ridiculous levels."

What Is Happening Now With Real Yields?

Since the start of 2022, real yields have turned higher, with a particularly sharp increase since the beginning of March. At the very end of April, 10-year real yields turned positive for the first time in two years.

How Much Do Real Yields Matter?

Not all observers give as much credit to real yields.

While the stock market has been moving in lockstep with real yields of late, that isn't always the case. Outside of the two periods where the Fed has been either launching or reversing quantitative easing – moves taken in response to the global financial crisis and the pandemic – stocks can move independently of real rates. For example, in 2017 and 2018, real yields more than doubled as the Morningstar US Market Index rose a total of 27%.

"It's a useful metric, but there is correlation confused for causation," says Raheel Siddiqui, senior investment strategist at Neuberger Berman. "This correlation exists but it's not the cause and effect that people make it out to be."

"Real rates are not causing the selling," he says. "Stocks are not in the business of looking at 10-year yields, not directly; they are primarily in the business of figuring out what is happening to earnings."

Siddiqui points to the relative performance of stocks that traditionally trade closely in line with the bond market, such as utilities. "The bond proxies should be selling off, and the stocks that trade like bonds should be selling off," he says. "But utilities are doing very well."

Fidelity's director of global macro Jurrien Timmer says that the rise in real yields is both warranted and a positive for the stock market.

"Sharply negative real rates are valuable to fight a recession, but for an economy that's running above potential, there is no justification for negative real rates at this point in the game," he says.

In addition, Timmer says, that while negative real yields can be very stimulative, they can also lead to more volatility. "The longest and most stable expansions were ones where real interest rates were modestly positive," he says.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MFL6LHZXFVFYFOAVQBMECBG6RM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EGA35LGTJFBVTDK3OCMQCHW7XQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)