What Rising Inflation Means for Your Portfolio

Continued higher inflation would have far-reaching implications for portfolio diversification, but there’s no need to panic.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

In our recently published 2022 Diversification Landscape report, we took a deep dive into how different asset classes performed in the past couple of years, how correlations between them have changed, and what those changes mean for investors and financial advisors trying to build well-diversified portfolios.

Now that resurgent inflation has started raising its head, we also looked at how a continued period of higher inflation might affect the link between stocks and bonds. The upshot: If inflation remains above-average for an extended period, Treasuries and other high-quality bonds might be less reliable diversifiers, although they still have merit as core portfolio holdings.

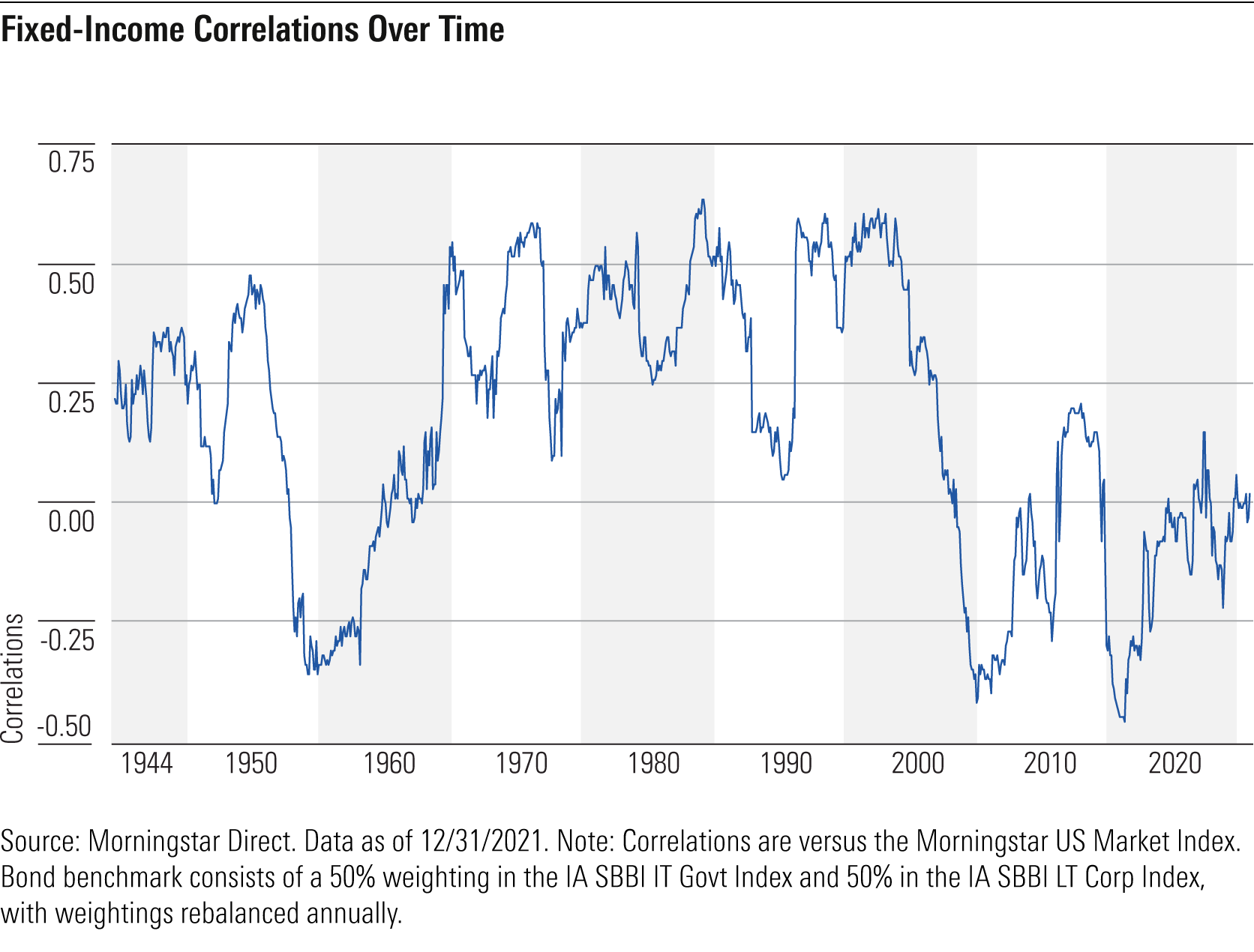

Learning From History

Until recently, the past 30 years have been unusually benign from an inflation perspective. Aside from a brief increase in the mid-2000s, inflation was generally running well below its long-term historical average of about 2.7%. This, in turn, created close to ideal conditions for stock/bond correlations. With inflation mostly a non-issue, stocks and bonds moved largely independently; in fact, rolling three-year correlations between stocks and bonds had been consistently negative (or barely above zero) since November 2000.

Exhibit 1

While most institutional investors currently expect the recent spike in inflation rates to moderate over the coming quarters, an extended period of higher inflation would likely be negative for both stock and bond returns, potentially increasing the correlation between the two asset classes. In fact, correlations between stocks and bonds moved into positive territory in 2021, with a correlation coefficient of 0.19 between the two asset classes for the full year.

Previous inflationary periods shed some light on what might happen in the future. As shown in the exhibit above, the stock/bond correlation has often been positive over multi-year periods. For example, trailing three-year correlation coefficients between the two asset classes were consistently above zero from August 1966 through August 1974. Stock/bond correlations were also consistently positive from January 1941 until late 1950.

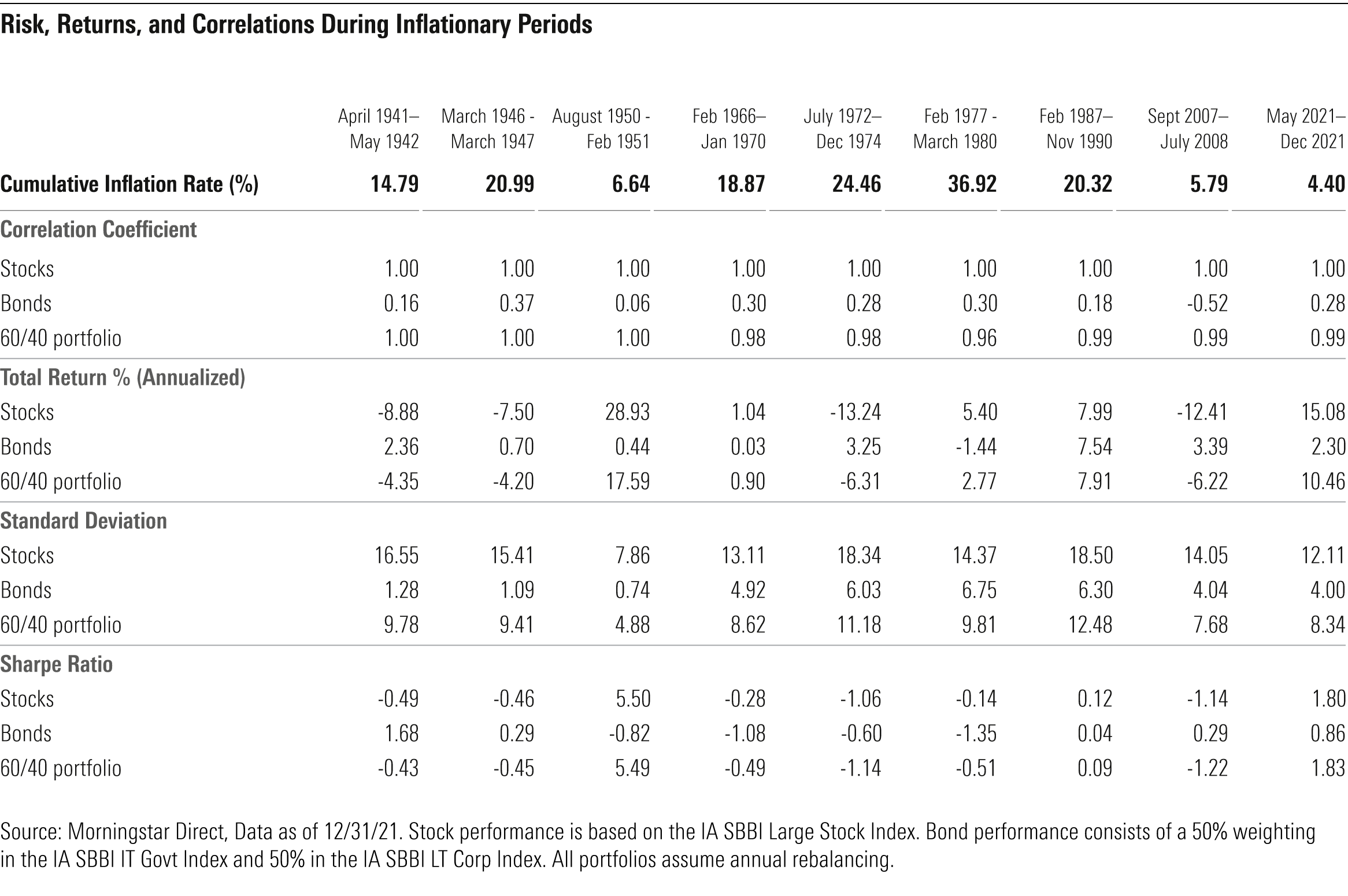

We also looked at correlations over specific periods of higher inflation, generally defined as periods when year-over-year inflation increased by at least 5% and remained high for at least six months.

As shown in Exhibit 2, correlations between stocks and bonds increased during some but not all periods. In general, correlations increased the most during periods when inflation was both high (in the double digits) and protracted (lasting at least three years). The post-World War II era saw an unusually high spike in inflation (driven by the removal of wartime wage and price controls, combined with large numbers of troops coming home), but the increase in consumer prices lasted only about a year. More recently, surging economic growth in China fueled rising consumer prices in 2007 and 2008, but inflation remained below 6% and lasted less than a year.

Exhibit 2

The most dramatic correlation upturns took place in the periods from February 1966 through January 1970 (driven by low unemployment and surging economic growth) and February 1977 through March 1980 (driven by soaring oil prices, the oil embargo and related price shocks, and expansionary monetary policies). Correlations ended up in a similar range (0.26 and 0.28, respectively) in both periods. That, in turn, reduced the benefit from adding bonds from a portfolio perspective.

Portfolio Implications

There are several key lessons to draw from these patterns. For one, investors probably shouldn’t expect a dramatic rise in correlations unless consumer prices continue increasing at a rapid rate for at least three years. But at the same time, the deeply negative stock/bond correlations that we’ve seen over most of the past couple of decades may not be repeatable, either. If correlations between equities and fixed-income securities remain above zero, that would reduce the diversification benefit from adding bonds, which could be exacerbated by lower returns if interest rates eventually increase. (We’ve already seen a preview of these trends in 2021 and early 2022, as interest rates and inflation have both been trending up.)

That doesn’t necessarily mean investors should shift assets from bonds to stocks, however. Stocks and bonds tend to move more in tandem during inflationary periods, but bonds can still provide significant diversification benefits, as well as play a critical role in providing ballast and reducing risk at the portfolio level.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MFL6LHZXFVFYFOAVQBMECBG6RM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HCVXKY35QNVZ4AHAWI2N4JWONA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EGA35LGTJFBVTDK3OCMQCHW7XQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)