7 Charts on the Stock Market’s Wild January

Volatility leads stocks to their worst start since 2009.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

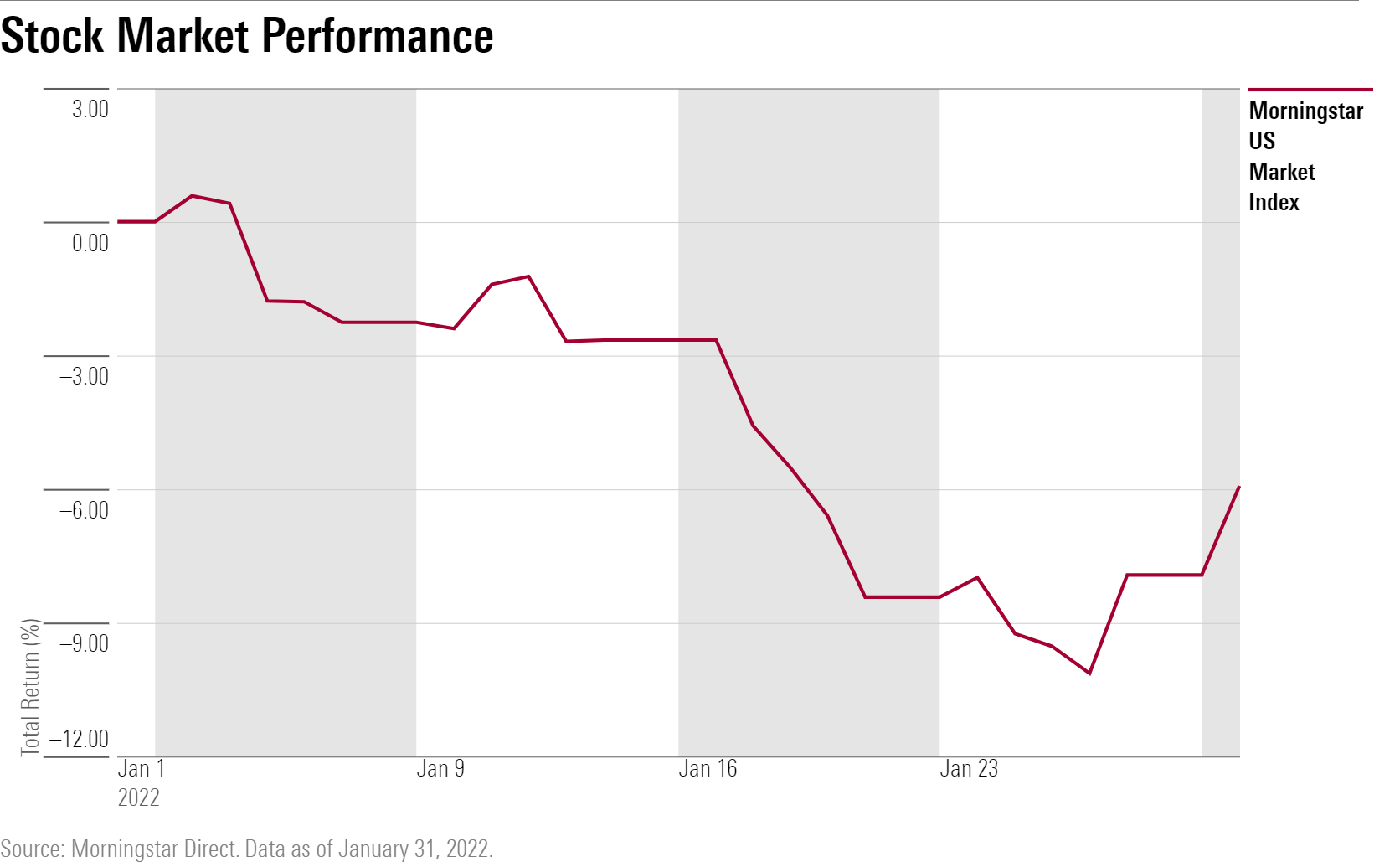

From start to finish, January was one wild month for the stock market.

Equities went from hitting record highs at the start of January to falling into “correction” territory of double-digit losses, only to roar back with strong gains on the final day of trading.

When the dust settled Monday:

• The U.S. Market Index lost 5.9% in January, the worst start to a year since 2009

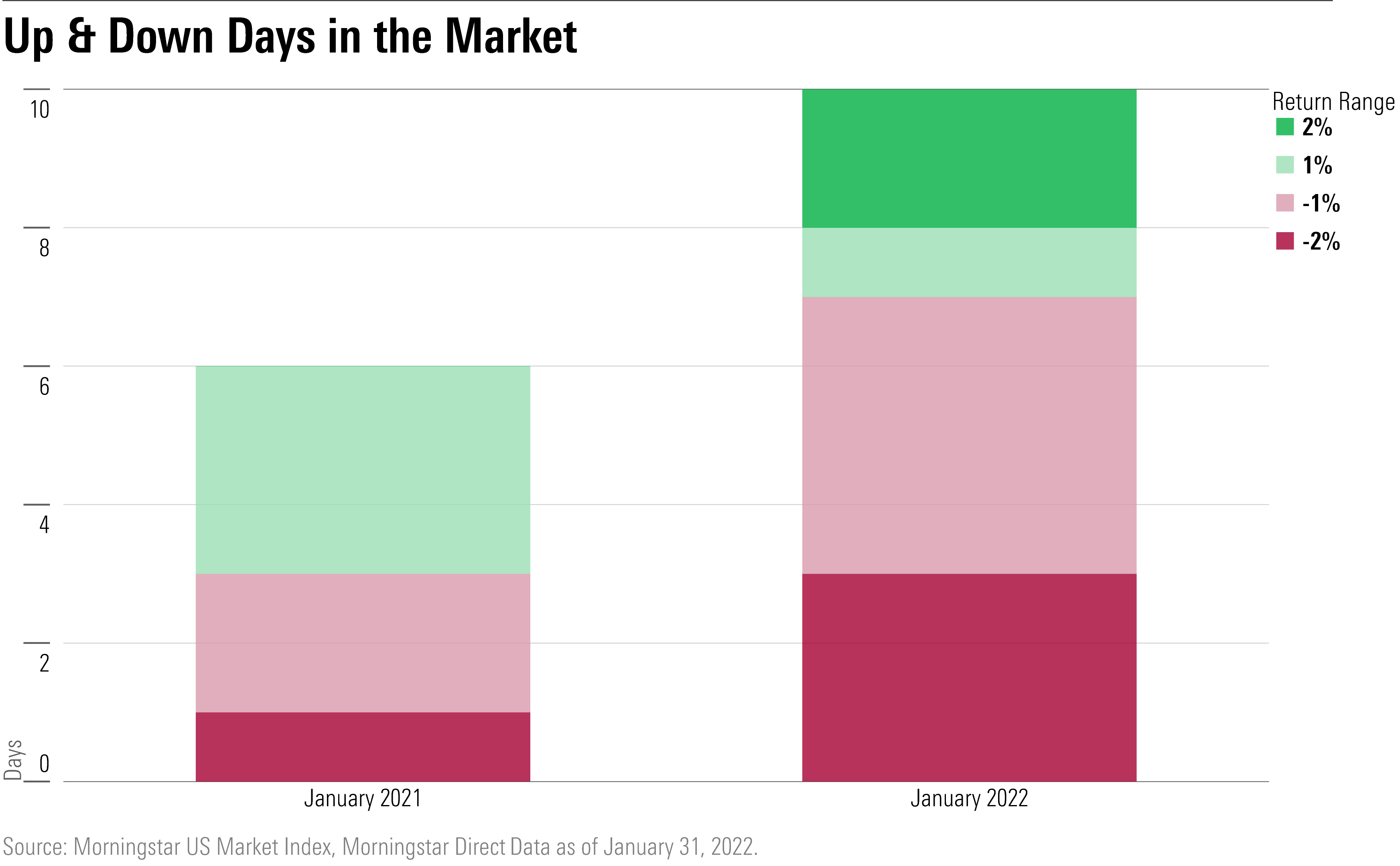

• During January, there were five days where the U.S. market moved 2% or more, and ten days where the U.S. market moved more than 1%

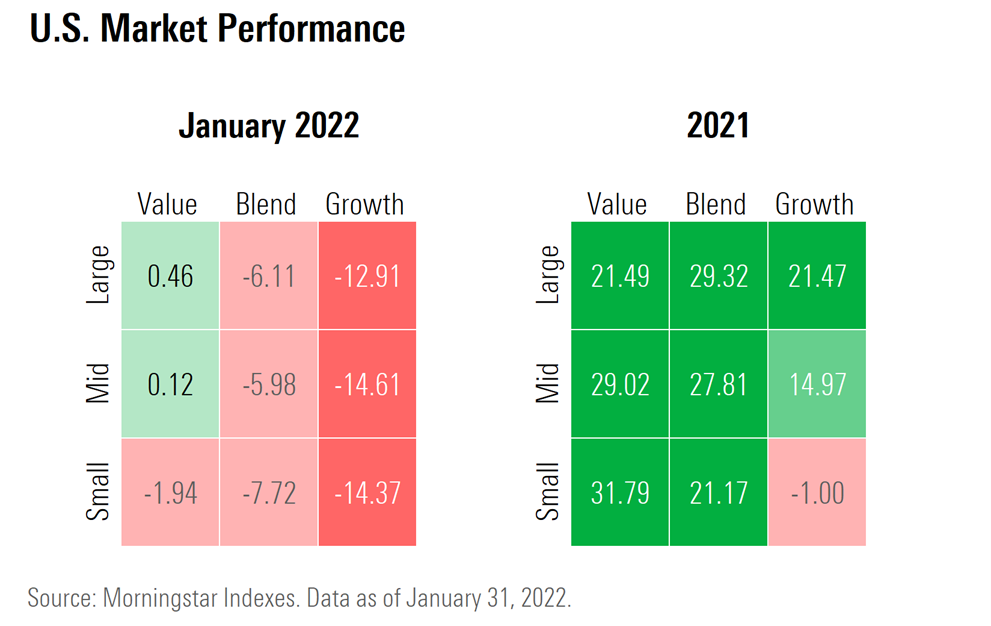

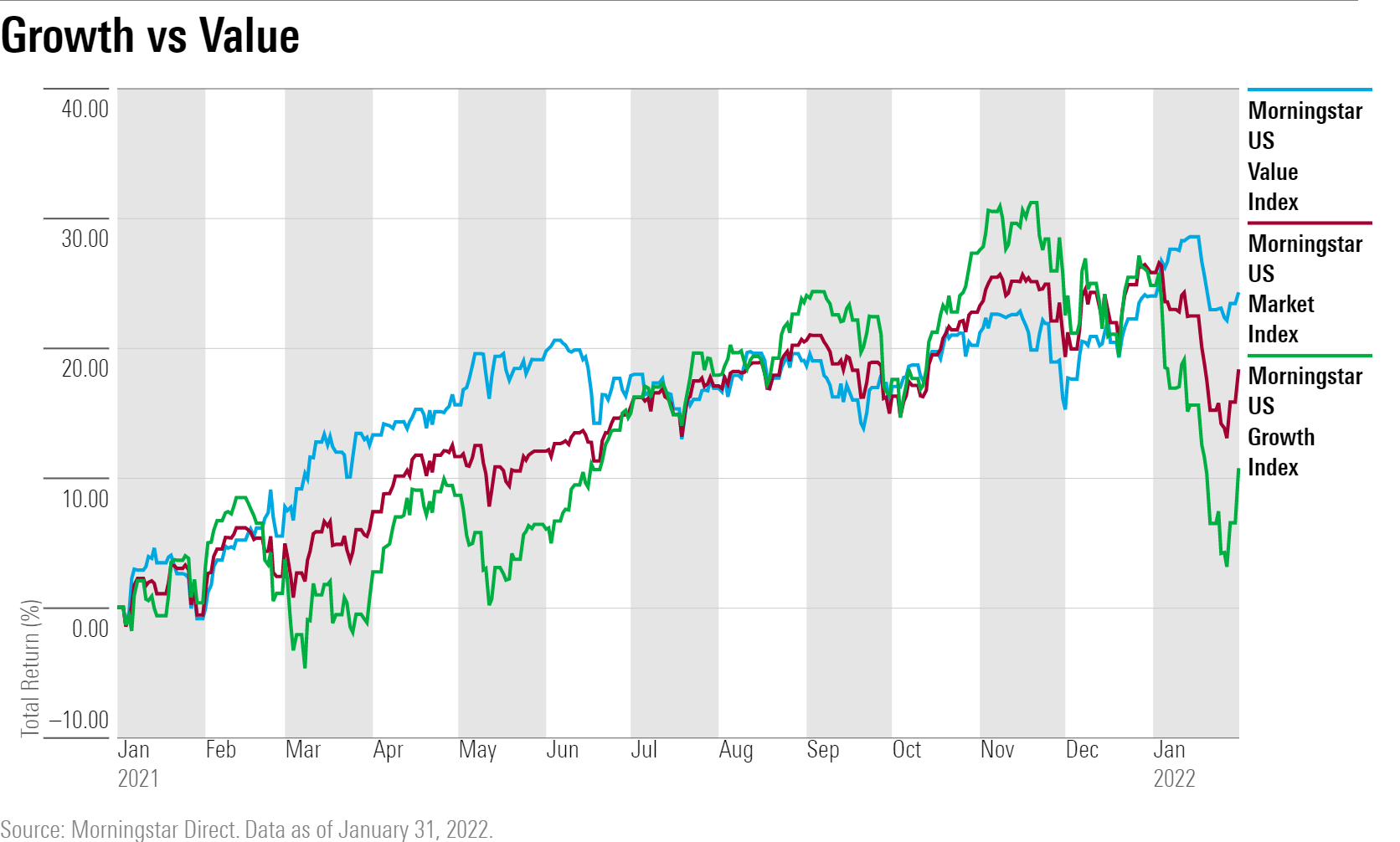

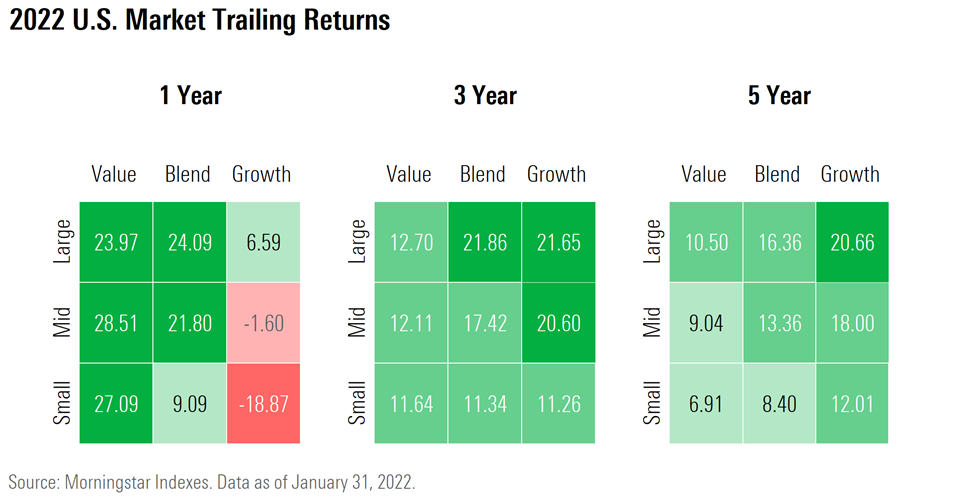

• Value stocks outperformed growth by 11 percentage points, the widest gap since February 2001

• Large growth stocks lost 12.9% and mid-cap growth stocks dropped 14.6%

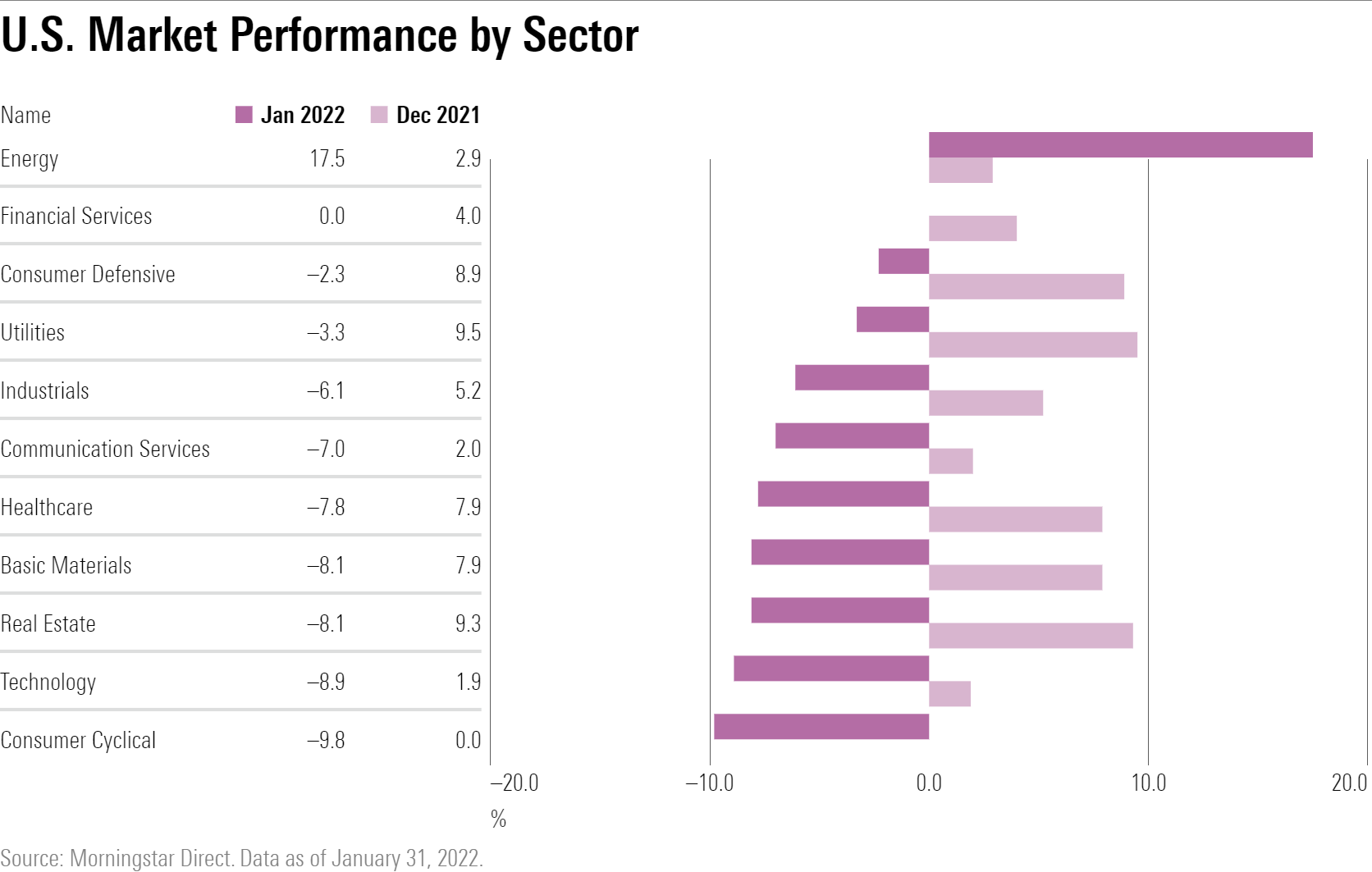

• Technology stocks slid 9%, the worst month of declines since March 2020

• Consumer cyclical stocks fell 10%, the sector's worst monthly performance since March 2020

• For tech stocks it was the worst January since 2008

These wild swings in the market came against a backdrop of a significantly shifting landscape for Federal Reserve policy and interest rates. With inflation surging in late 2021, investors had to recalibrate their expectations for the Fed. Rates are now expected to rise higher and faster this year.

With stocks starting off the year at relatively lofty valuations, the market was vulnerable to the kinds of declines seen over the course of the month. That was especially true of many technology and consumer cyclical names that had led the market higher in 2021.

“You can really see the lopsidedness of the selloff,” says Marta Norton, chief investment officer for the Americas at Morningstar Investment Management. “What was selling off the most was the favorites and what was holding up was the less attractive stocks of the last few years. You had an element of levelling out of the market.”

After a strong 2021, where stocks were bolstered by surging corporate profits and a strong economic recovery from the pandemic recession, the U.S. Market index hit a new high within days of starting the year. However, things quickly turned south.

With that decline came a noticeable spike in volatility and a white-knuckle ride for investors. To some degree measuring the market’s swings by the close of trading each day didn’t do it justice. For example, on Monday, Jan. 24, stocks collapsed by some 4% in the morning only to finish the session little changed.

Two of the biggest trends in January were the rolling over of technology and consumer cyclical stocks, and the collapse of growth names in general.

Within the Morningstar Style Box, the performance gap among stocks was stark and driven by where they landed on the value vs. growth style spectrum. That contrasted with 2021 performance where the market value of a stock played had a greater link to performance than whether it was undervalued or a fast-grower.

For growth stocks, January’s steep declines reversed a substantial portion of 2021’s gains.

But over longer time frames, growth and blend stocks still generally hold a substantial advantage over value. That's in part due to value's woes in 2020 when growth outperformed value by record margins. Large- and mid-cap growth stocks in particular remain far ahead compared to value stocks and smaller companies.

The other big trend in January was the collapse of technology and consumer cyclical stocks. These sectors had been major drivers of the market’s 2021 rally and many of these stocks were trading at lofty valuations. The tech sector's declines have come as investors adjusted to an outlook of higher interest rates and moderating economic growth for this year.

Among the big-name technology and consumer stocks that have taken a hit in January are NVIDIA NVDA, which lost 17% in January after a 125% rally in 2021, Microsoft, off 7.5% last month after a 52.2% gain in 2021, and Tesla TSLA, down 11.4% so far in 2022 after a 49.8% gain last year.

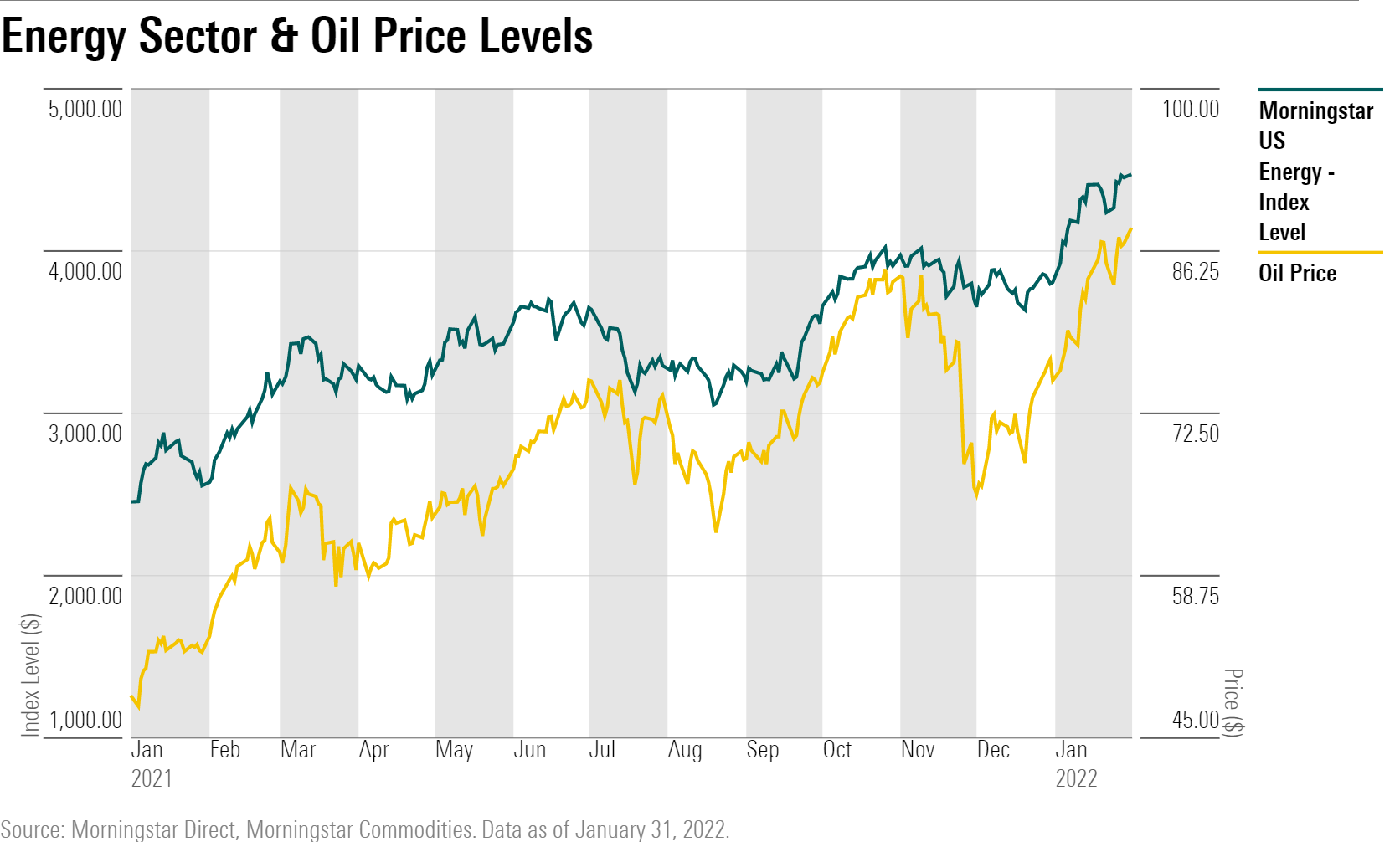

Energy stocks rallied strongly in 2021 and started strong in 2022 on the back of rising oil prices.

ConocoPhillips COP, for example, gained 22.8% in January following an 85.4% rally in 2021. Continental Resources CLR, meanwhile, is up 16% in 2022 following a 177.4% return last year.

Correction: An earlier version of this story included incorrect data on the U.S. market index, value and growth index performance and sector performance. This story has been updated to reflect those changes.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T5MECJUE65CADONYJ7GARN2A3E.jpeg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)