Sustainable Index Funds Produce Strong Gains in 2021

Performance bolsters the case that ESG ratings and metrics can deliver competitive returns.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

ESG index funds continued to deliver strong returns in 2021, both in absolute and relative terms. Last year's performance adds to the evidence that investments that use environmental, social, and governance ratings and metrics to select securities and structure portfolios can deliver competitive returns. This is good news for anyone interested in sustainable investing. It is especially welcome news for those financial advisors who have been hesitant to address their clients' sustainability concerns because they do not want to steer them into underperforming investments.

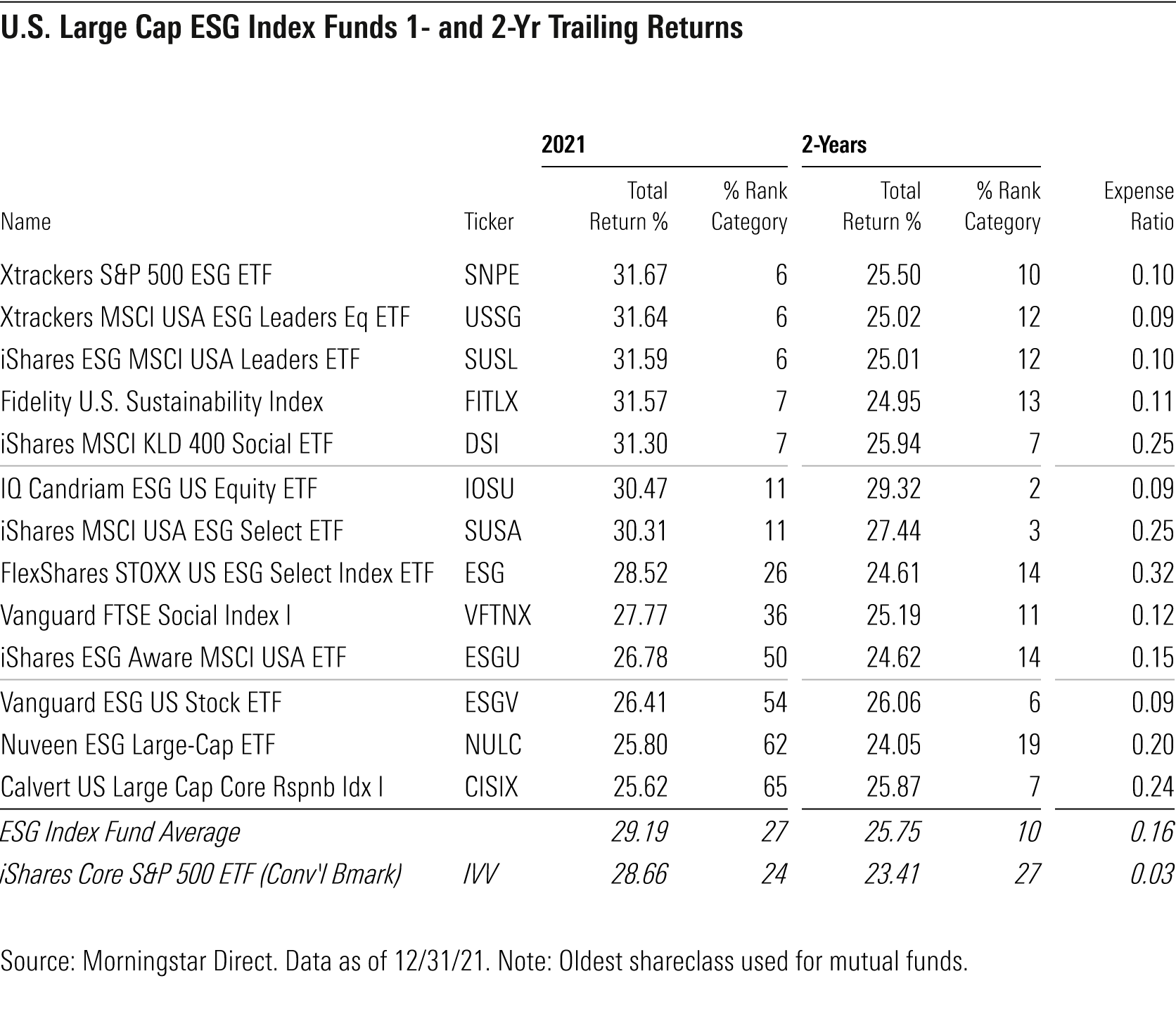

The 13 ESG index funds available to U.S. investors that follow broad, diversified indexes of U.S. large-cap stocks posted gains ranging from 25.6% to 31.7% in 2021. Their average return was 29.2%. The S&P 500, represented here by iShares Core S&P 500 ETF IVV, returned 28.7%. Seven of the ESG index funds gained more than 30%. Of all funds in the large-blend Morningstar Category, less than one in four outperformed IVV.

Two funds distributed by DWS' Xtrackers exchange-traded fund group led the way. Xtrackers S&P 500 ESG ETF SNPE posted a 31.67% return and Xtrackers MSCI USA ESG Leaders Equity ETF USSG posted a 31.64% return.

The picture looks even better over the trailing two years. Every one of the baker's dozen ESG index funds outperformed the S&P 500 during the 2020-21 period, and all finished comfortably in the category's top quartile. IVV's two-year return, by contrast, placed just outside the top quartile. I include the two-year comparisons because the period corresponds with the pandemic and several of the funds do not yet have three-year records.

Top performers over the two-year period were IQ Candriam ESG US Equity ETF IQSU, which gained 29.32% annualized, and iShares MSCI USA ESG Select ETF SUSA, which gained 27.44% annualized.

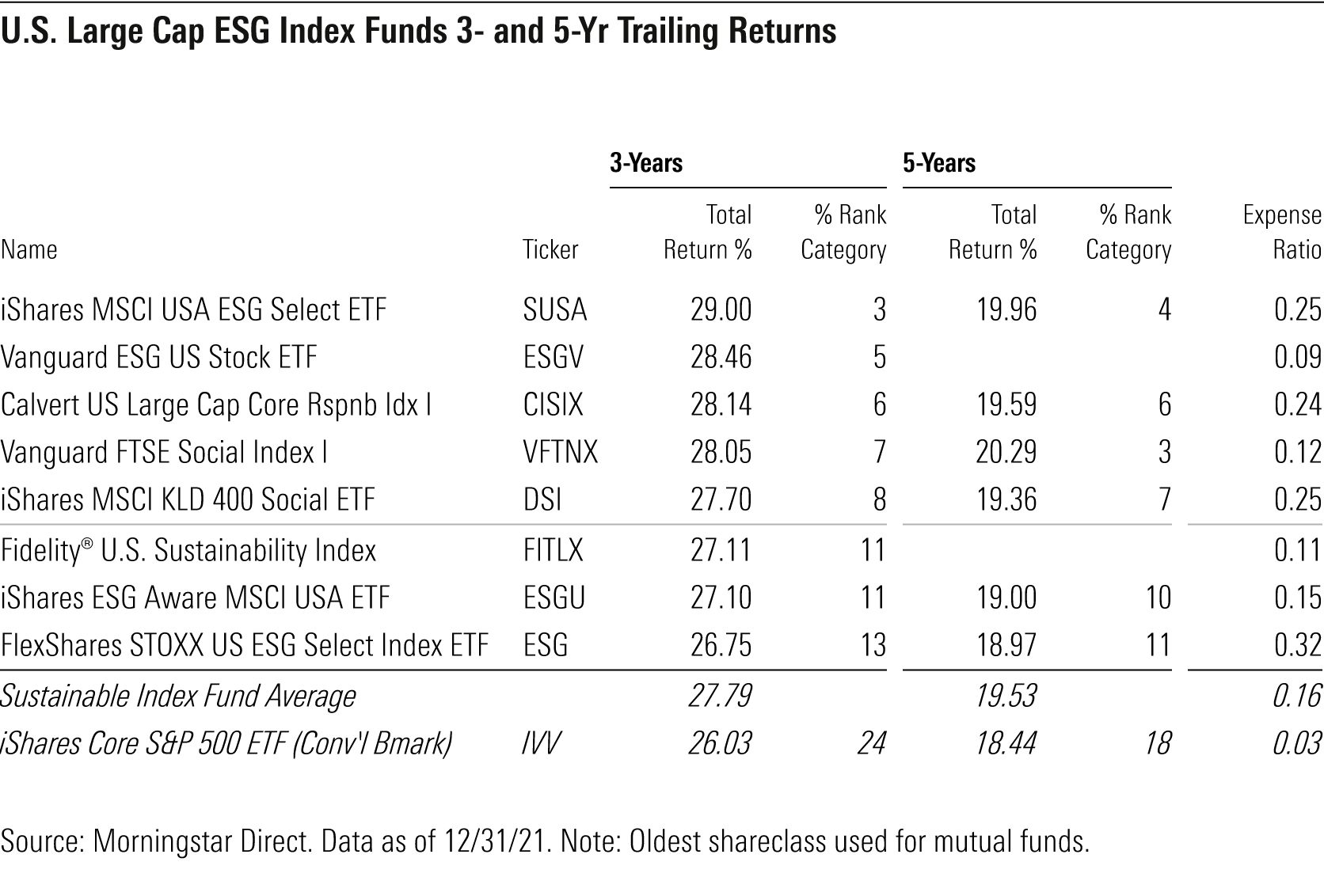

Only eight of the 13 ESG index funds have three-year records, but again for this period, all of them outperformed the S&P 500 on an annualized basis, and all of them placed in the category's top quartile (in fact, all placed in the top 15% of the category).

For the trailing five years, the story remains the same. While only six of the 13 funds have five-year records, all of them outpaced the S&P 500 by comfortable margins. The "worst" ESG performer over the trailing five years still beat IVV, our S&P stand-in, by more than 0.5% annualized. All six ESG index funds placed in or near the top decile of the large-blend category.

Even more notable, four of the six funds outperformed the S&P 500 stand-in over the trailing five years despite having expense ratios ranging from 0.24% to 0.32%. IVV's expense ratio is only 0.03%. And two of them, iShares MSCI KLD 400 Social ETF DSI and SUSA, had expense ratios of 0.50% at the beginning of the five-year period. Both funds cut their fees in half in the first half of 2018, but their outperformance is even more notable because they had to overcome their higher fees.

On the subject of fees, let's be clear: IShares should not be hitting shareholders of DSI and SUSA ($8.5 billion in combined assets) with 0.25% fees for funds that should cost no more than 0.10%. Two other, newer iShares ESG index funds are on the list and they only charge 0.15% and 0.10%.

In sum, ESG index funds are perfectly good options for broad U.S. equity exposure and most of them charge reasonable fees. Investors should not expect these funds to outperform every year, but neither should they avoid them altogether in the outdated belief that funds that consider ESG factors cannot deliver competitive returns.

Keep in mind that ESG index funds are not alike in the way that, for example, S&P 500 index funds are. The ESG index funds discussed here differ not only in the amount of fees they charge but in the underlying indexes they follow. ESG indexes differ on the exclusions they employ and on how they use company ESG ratings and metrics to determine which stocks to include and how to weight them. The funds also differ in how strongly they push ESG issues in their engagements with companies and how strongly they support ESG-related proposals via proxy voting.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/XTXQYAMAL5EKRLGIS3IDVAZ3R4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/3J75DKCBIZCTJMRFWSSJSHHCJ4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DJVWK4TWZBCJZJOMX425TEY2KQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)