For Retirees, When Inflation Arrives Is as Important as Its Magnitude

A look at retirees, inflation, and sequencing risk.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Assets and Liabilities

The danger to retirees of immediate stock losses has been well documented. The timing of stock-market performances doesn't matter to those who are preparing for retirement, assuming they stay the course. Ten years of poor returns followed by 10 years of strong returns is the same when reversed. Either way, investors reach the same place. Not so for retirees: Early declines cause more damage.

The reason is twofold. First, if the bear market holds off long enough, retirees may no longer be around to experience it. Second, the investment math differs for those who are retired. Unlike accumulators, retirees cannot shrug off investment losses; they must instead sell into weakness to meet their required withdrawals. Preferably that will occur later in retirement, when the time horizon is shorter (and the portfolio size is perhaps larger), than when entering that stage.

What happens to retirees' assets, though, is only half the story. The other half involves their liabilities--that is, what they wish to spend. Those also change. Sometimes liabilities shift because of personal circumstances. While important, such instances resist generalization. However, everybody faces inflation. The higher that rate, the more that retirees must remove from their portfolios.

Once again, the timing does not affect those who have yet to retire. As with investment returns, high inflation for those accumulating for the future that is followed by low inflation is a wash. The overall rate of inflation matters to such investors, but not its sequence. Once again, the math for retirees is different. As before, they benefit when the bad news is delayed.

The Final Year

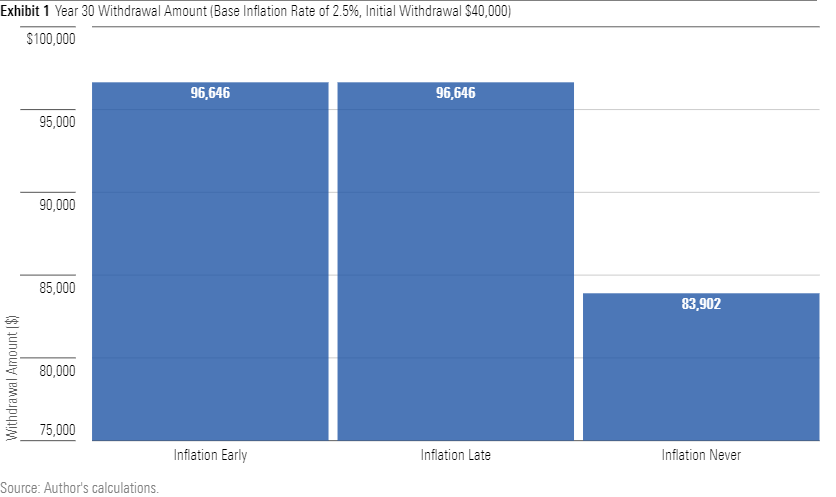

This is not initially apparent, because when calculating future spending needs, the final amounts do not depend upon inflation’s timing. Exhibit 1 shows the year 30 withdrawals for three hypothetical retirees. Each investor had a 30-year time horizon and an initial withdrawal amount of $40,000, adjusted each year for the effect of inflation. However, each faced different inflation conditions.

The retiree with the catchy name of "Inflation Early" endured an inflationary surge during the first five years of retirement, when the rate doubled to 5%. Subsequently, for years six through 30, inflation subsided to 2.5%. "Inflation Late" had the opposite fortune, with inflation averaging 2.5% for the initial 25 years before doubling during the retiree’s final five years. "Inflation Never" came off best, with annual inflation remaining at a muted 2.5% throughout the three decades. In summary:

- Inflation Early: five years at 5%, 25 years at 2.5%;

- Inflation Late: 25 years at 2.5%, five years at 5%;

- Inflation Never: 30 years at 2.5%.

Naively, one would expect the year 30 withdrawal amounts for Inflation Early and Inflation Late to agree, as each investor experienced the same average inflation rate (of 2.92%) during their retirements. That is indeed what occurs.

The Bigger Picture

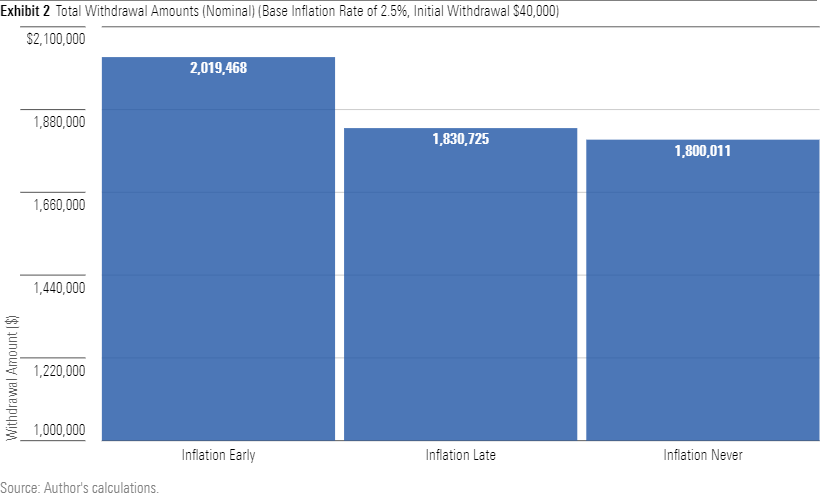

So far, so obvious. However, the year 30 evidence is incomplete, because it ignores what came before. Different paths carry different costs. Rather than assess solely the size of the final payment, one should evaluate the total withdrawals. After all, each party realizes the same real income: $1.2 million, consisting of 30 annual payments of $40,000, as expressed in year zero dollars. All things being equal, one would prefer to spend less to achieve that outcome.

The next illustration demonstrates the point: Inflation is forever. When prices rose for Mr. Inflation Early from Years 1 through 5, forcing him to withdraw additional monies, the effect was not limited to that period. During year five, Inflation Early removed $51,052 from his portfolio, as opposed to $45,256 for his counterparts. That gap persisted. Thus, in year 25, Inflation Early spent $83,653 while the other two parties withdrew $74,158. In aggregate, the difference was substantial.

Considering Time Value

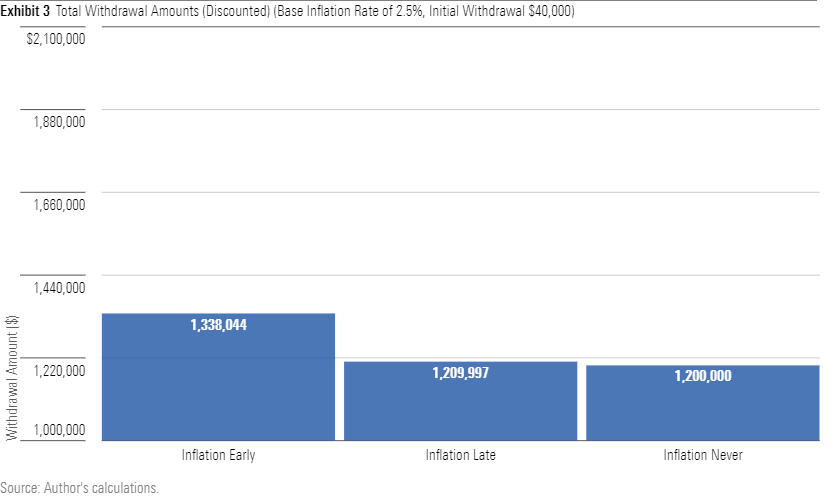

While instructive, this portrait oversimplifies the inquiry, because it ignores the time value of the withdrawals. Just as a dollar received today is more valuable than a dollar received in the future, so too is a dollar spent today more costly than one that is spent in the future. To conduct the analysis properly, one must treat all withdrawals equally, by translating their future values into present terms. (If this reads like jargon, my apologies. Explaining discounted cash flows lies outside this column's scope. However, this article explains what I have neglected.)

Discounting all cash flows by the base inflation rate of 2.5% (note that using a different discount rate changes the numbers but not the conclusion) strengthens the argument that inflation is best served cold. The damage from the additional inflation experienced by Inflation Late is limited because it so occurs so many years after the starting point. After the cash flows are discounted, only Inflation Early truly felt the inflationary surge.

The Bright Side

Fortunately, things aren’t quite so bad for Inflation Early as this picture suggests, unless he was rash enough to have invested fully in long conventional bonds, which can’t increase their payments when inflation rises. Other investment strategies, though, provide retirees with the possibility of catching up with higher inflation. Short- to intermediate-term bonds, purchased through ladders, are likely to offer steeper yields after inflation surges. And, for equity investors, companies that can pass along their additional costs to customers will prosper.

Thus, it would be hasty to conclude that if today’s inflation spike persists, recent retirees will suffer. Their portfolios may adjust and absorb the damage, even if they do not hold inflation hedges such as Treasury Inflation-Protected Securities, commodities, or real estate. What we do know, however, is that an inflationary uptick carries the potential to cause long-term damage. The longer that such an event can be postponed, the better.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)