What Are Fund Providers Doing to Improve Shareholders' Returns?

Every little bit helps.

/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)

A version of this article previously appeared in the September 2021 issue of Morningstar ETFInvestor. Click here to download a complimentary copy.

The fee fights among providers of index mutual funds and exchange-traded funds that dominated headlines in recent years have since faded into the background. Investors emerged clear winners. Today, an investor can build a portfolio of index funds representing virtually every stock and bond on the planet with a blended expense ratio of 0.06%. That's just $6 for every $10,000 invested.

As tiny fees become the new standard, it's time to look at other ways that the providers of ETFs and index mutual funds can add value back to shareholders. Now that these funds' fees have been squeezed, these practices may matter more than a 0.01 percentage point difference in expense ratios. This article will explore a few methods already employed in the index fund industry that haven't grabbed as many headlines as funds with no fees.

Passive but Not Idle

With their wide scope and low turnover, broad market-cap-weighted index funds are often considered the ultimate long-term owners of the securities in their portfolios. But instead of sitting on these securities, many funds put them to work on behalf of their shareholders. Funds will often loan out portfolio securities in exchange for a lending fee, a practice commonly referred to as securities lending. The bulk of the revenue generated from these loans gets passed back to shareholders, adding to funds' returns. But there is risk involved. To protect fund shareholders against potential borrower default, the transaction typically requires collateral from the borrowers, which could be cash or noncash securities. If the collateral is noncash, that is, government securities (U.S. Treasuries or U.S. agency debt) or a letter of credit, the transaction is straightforward: The borrowers pay the fee and the lenders deliver the securities after the collateral is received. On the other hand, if the collateral is cash, lenders often reinvest the collateral and the income generated can offset the lending fee, sometimes entirely. The current market best practice is overcollateralization of at least 102% of the borrowed securities' value for domestic securities and 105% for foreign securities. After the 2008 global financial crisis, when aggressive cash collateral investment resulted in losses for some lenders, the SEC began suggesting conservative investment of cash collateral in highly liquid securities.

There are also costs involved. Not all the income generated through securities lending is passed back to fund shareholders. A portion of these revenues covers the costs associated with running these programs. The revenue split between fund providers and fund shareholders varies depending on the fund in question. The percentage of gross lending revenue passed on to fund investors can range anywhere from 60% to 100%. Fund companies can use a third-party broker or an affiliated lending agent. There are advantages and drawbacks to both. While a third-party agent might charge a higher fee, having an in-house lending unit can raise concerns about potential conflicts of interest. We examined this in great detail in our 2018 white paper on securities lending.

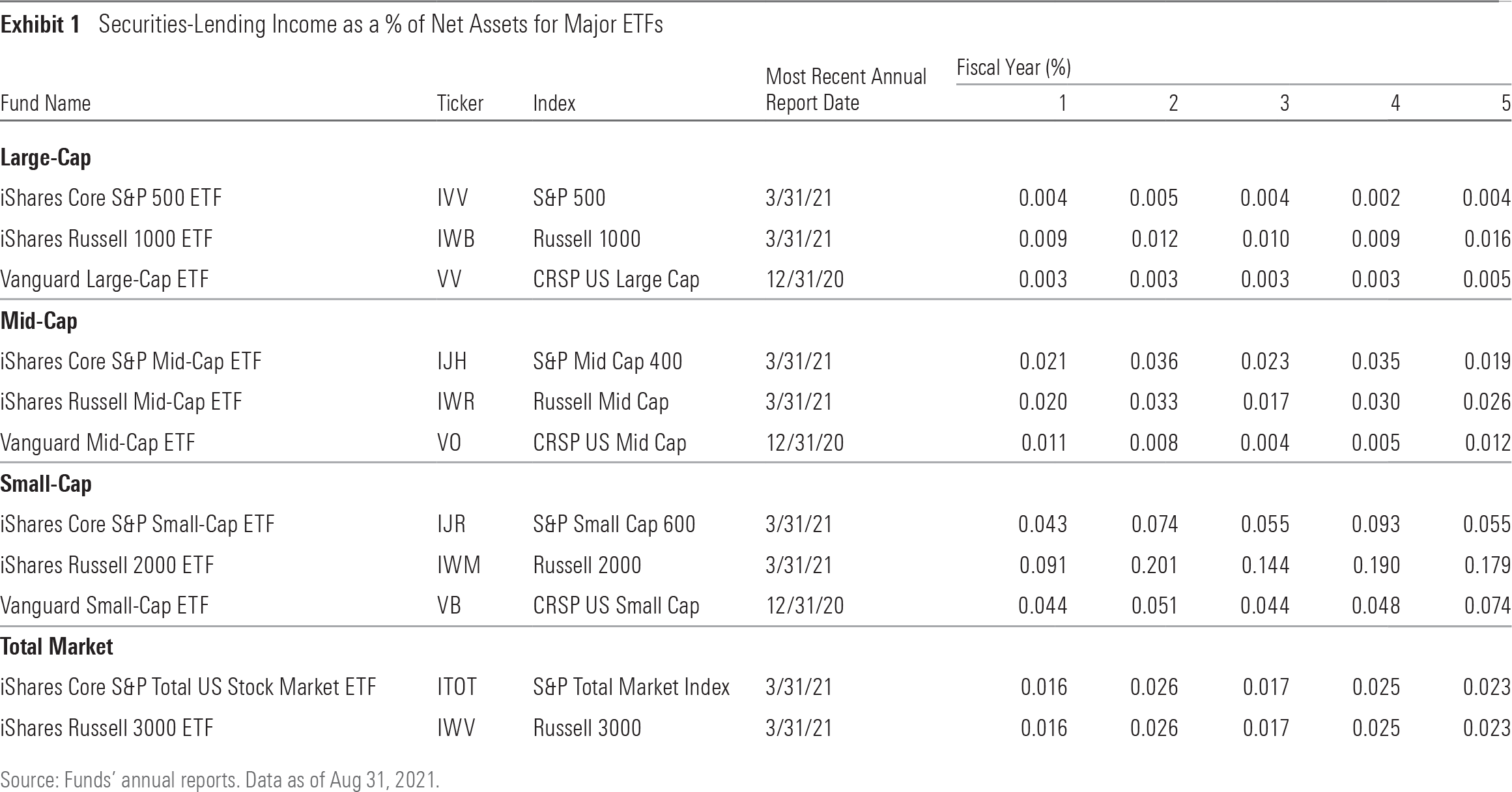

Fund shareholders can find details on funds' securities-lending income in the income statement of their annual reports. For most funds, this number is immaterial. Most of the demand in the securities-lending market centers around smaller stocks, which are particularly popular among short-sellers--the most common borrowers. Small-cap stocks typically take up a small portion of most broad market-cap-weighted funds' assets. But for dedicated mid- and small-cap funds, securities-lending income can be a big deal. Exhibit 1 shows the annual securities-lending income generated by a sample of prominent funds representing different market-cap strata. More comprehensive data on funds' securities-lending activity began being reported to the SEC through Form N-CEN in 2018. This data is available on the SEC website and Morningstar Direct. The figures in Exhibit 1 are calculated using end-of-period net assets and might be different from the N-CEN figures, which use average daily assets.

Small-cap funds consistently reap the greatest gains from securities lending. The poster child for this phenomenon is iShares Russell 2000 ETF IWM, which is the most prolific lender of portfolio holdings among major index funds. IWM often generates approximately 0.20% of additional annual return on a yearly basis--often enough to cover its 0.19% expense ratio. As a result, IWM lagged Vanguard Russell 2000 ETF VTWO by just 0.02% annually from VTWO's 2010 inception through August 2021, despite the fact that IWM currently charges a fee that is nearly twice VTWO's. (VTWO shaved its fee in 2019, but it had previously been 5 basis points lower than IWM's expense ratio.)

Taming Turnover Costs

In indexing, precision is paramount. In addition to lending out positions to generate additional income and pull their funds' returns closer to their target, index-fund managers also focus on minimizing the costs of turnover.

Turnover costs generally take two forms. Some, like commissions and bid-ask spreads, are readily measurable. Others are more elusive. Chief among these immeasurables is market impact cost--the degree to which these funds' turnover pushes the prices of the securities they are buying away from them. For example, how much did S&P 500-tracking index portfolios' purchases of Tesla TSLA shares push the stock's price higher when the firm was added to the index in 2020? To quote the old Tootsie Pops commercial, "The world may never know."

Index fund managers have to make price-insensitive trades to mimic their benchmarks; they don't have the same luxury as active managers who can trade what, when, and how much they want to. In the constant trade-off between tracking performance and transaction costs, the scale has often tilted toward the former. But that's begun to change.

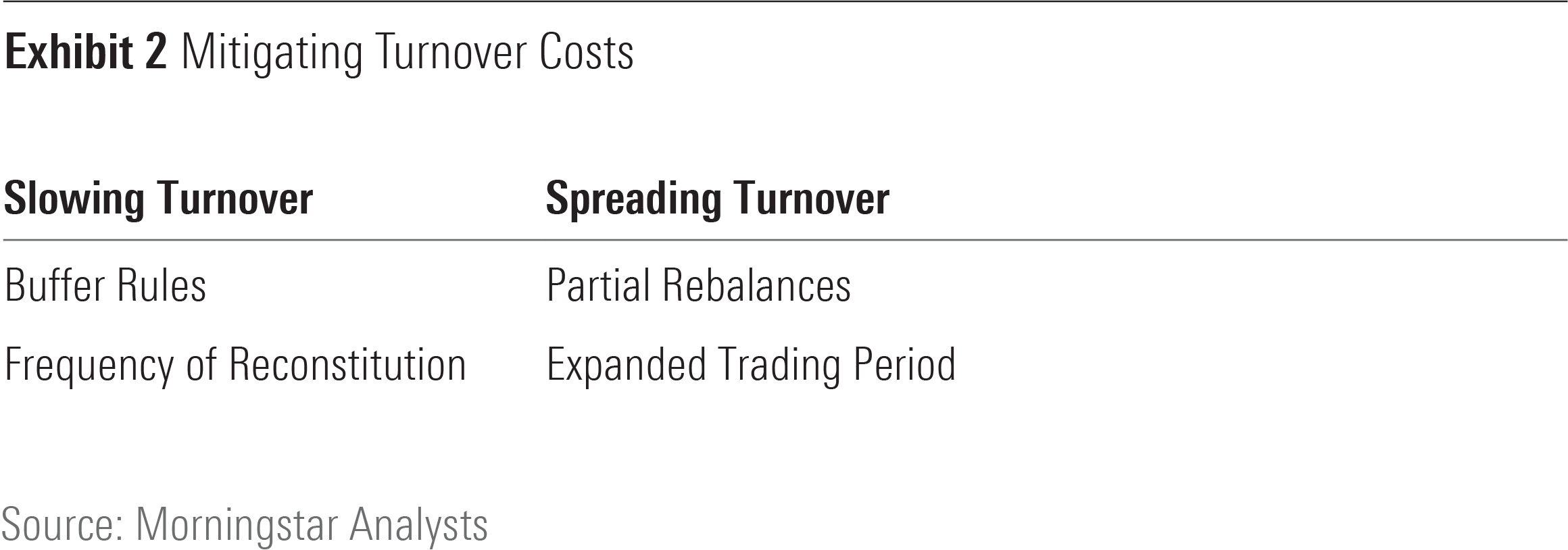

As index funds have grown and the technology their managers employ has improved, many index providers and fund sponsors have tried to tame turnover costs. The tactics they've employed often manifest themselves in the methodologies of the indexes that underpin these funds. In general, the approaches taken by these benchmarks are designed to either slow turnover or to spread it out. Exhibit 2 provides a snapshot of common techniques designed to meet each objective.

Slowing Turnover

The first line of defense against transaction costs is to reduce the frequency and volume of turnover. Fewer changes to the index lineup means less trading for fund managers and lower transaction costs.

Some index providers intentionally reduce the frequency of index reconstitution as a means of curbing turnover. The S&P 500, for instance, has no fixed review schedule and reconstitutes on an as-needed basis at the index committee's discretion. While this approach is not transparent, it can lower turnover compared with a recurring review schedule. Many broad-market indexes reconstitute annually and opt to include IPOs at their quarterly or semiannual rebalances.

Buffer rules that allow current constituents to temporarily stray from indexes' eligibility criteria have slowly become the new norm for rules-based indexes. Securities that flip-flop around these thresholds are given leeway to reduce unnecessary turnover. Most major broad-market indexes have adopted some form of buffer. The ones that don't do so stand out, perhaps most notably the Russell 2000 Index. The lack of a buffer at the widely followed index's lower threshold has resulted in meaningful transaction costs over the benchmark's long history.

However, these buffering approaches tend to work better for broad, market-cap-weighted indexes than those that base security selection and weighting on more-targeted and timely data, like those targeting momentum. Reducing turnover often means drifting from a factor exposure or theme.

Spreading Turnover

Many indexes have also introduced means of spreading turnover across a longer period and/or splitting it up across multiple, partial rebalances. This can help to reduce the market impact of turnover and may reduce the influence of rebalance timing luck on some indexes' performance. For example, Research Affiliates' RAFI index series--save for the FTSE RAFI indexes--rebalances in four tranches. The portfolio is split into four identical tranches, and each tranche takes its turn rebalancing at its designated quarterly rebalance. CRSP indexes move positions through a "packeting" approach. This approach can both slow and spread rebalancing. The methodology entails moving just 50% of a position that may be straddling size or style borders between its benchmarks at any given reconstitution.

Increasingly, many indexes are also spreading rebalances over several days instead of doing it all in one go on a single date. CRSP indexes--which underpin many of Vanguard's U.S. equity ETFs--were first movers on this front. They switched from a one-day rebalance to a five-day rebalance in 2017. The S&P Dividend Growers index series, the new indexes for the Vanguard Dividend Appreciation funds, rebalances over three days. In November 2020, iShares MSCI USA Momentum Factor ETF MTUM switched to a new variant of its original benchmark. Its new bogy rebalances over three days instead of one. As the funds that track them get bigger, these indexes are being tweaked to tread more lightly in an effort to minimize their market impact.

All the Small Things

As index-tracking funds' fees have shriveled and their assets have swelled, small things like securities lending and turnover costs have become a bigger deal. These two topics only scratch the surface of the myriad improvements in implementation that the managers of index funds look to make to their processes on a day-to-day basis to eke out every last basis point of performance on behalf of fund shareholders.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)