Asset Allocation for Retirees: What Will the Future Bring?

The case for a balanced portfolio.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

A Different Time

Friday's column suggested that retirees hold equities. Rarely during the past 90 years have investors been punished for owning stocks, assuming they retained their positions. Not only have 100% equity portfolios reliably permitted higher spending rates during retirement than have bond portfolios, save for when the Great Depression began, but such allocations have roughly matched the rates obtained by balanced portfolios, while carrying higher growth potential. Win-win.

Today's article complicates that wonderfully simple precept. (Investment writers can never leave well enough alone.) The precept of "the more stocks the better" assumes that the future will look something like the past. That seems a sound bet, given the amount of investment data. However, the sample size is small, as it contains only three independent 30-year periods spanning a full century. What's more, stocks have become unusually costly. History may thus prove an unreliable guide.

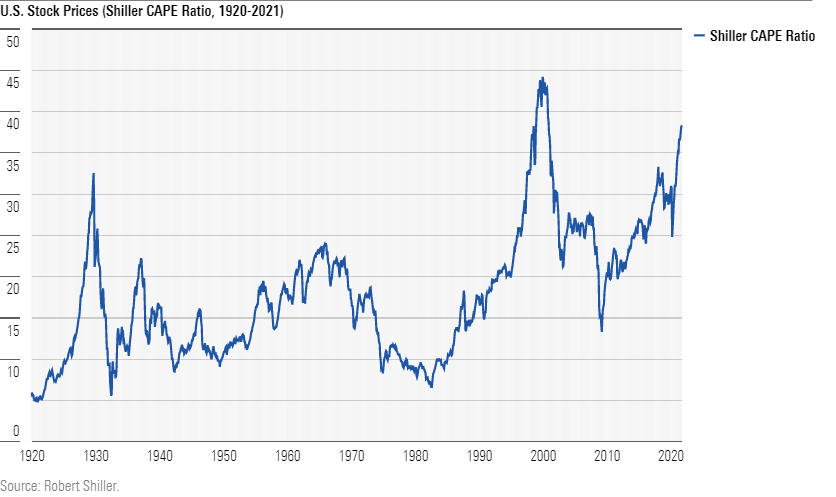

The chart below testifies that U.S. equity valuations currently occupy strange waters. Obtained from data on Nobel laureate Robert Shiller's website, it depicts the 100-year history of the stock market's CAPE ratio, which divides the market's current capitalization by its constituents' average earnings over the previous decade. The higher the figure, the more optimistically that equities are priced.

The current CAPE ratio of 38 has only once been exceeded, in December 1999, when the measure reached 44. (The date should please millenarians.) So far, investors who stayed put have prospered, because although stocks cratered in the spring of 2000 and crashed again in 2008, they have since rebounded so overwhelmingly that their CAPE ratio now outstrips the previous second-place figure, which occurred on the less-than-auspicious date of October 1929.

Considering the Alternative

That stocks recovered almost immediately was not inevitable. Equities might well have bounced along for many years at their post-2008 valuations, which, after all, resembled their previous norm. Had that occurred, the argument that retirees prefer equities would require a few asterisks.

Morningstar's researchers anticipate such a market outcome. The wing of the company that forecasts asset-class returns, Morningstar Investment Management, predicts that U.S. equity valuations will decline to something approaching their long-term average, then remain at that level. Consequently, their estimates for the next 30 years' stock returns are muted. (Researchers at the world's largest asset manager, BlackRock, reach a similar conclusion.)

Less controversially, the group also expects a weak bond performance. That almost certainly will occur. Over the past century, long U.S. Treasury yields have averaged 5.0%. Today, 30-year Treasuries pay 1.7%. With yields at that level, there's no realistic profit potential for bonds, unless U.S. inflation were to disappear entirely, becoming outright deflation. Otherwise, the best that fixed-income securities can do is muddle along.

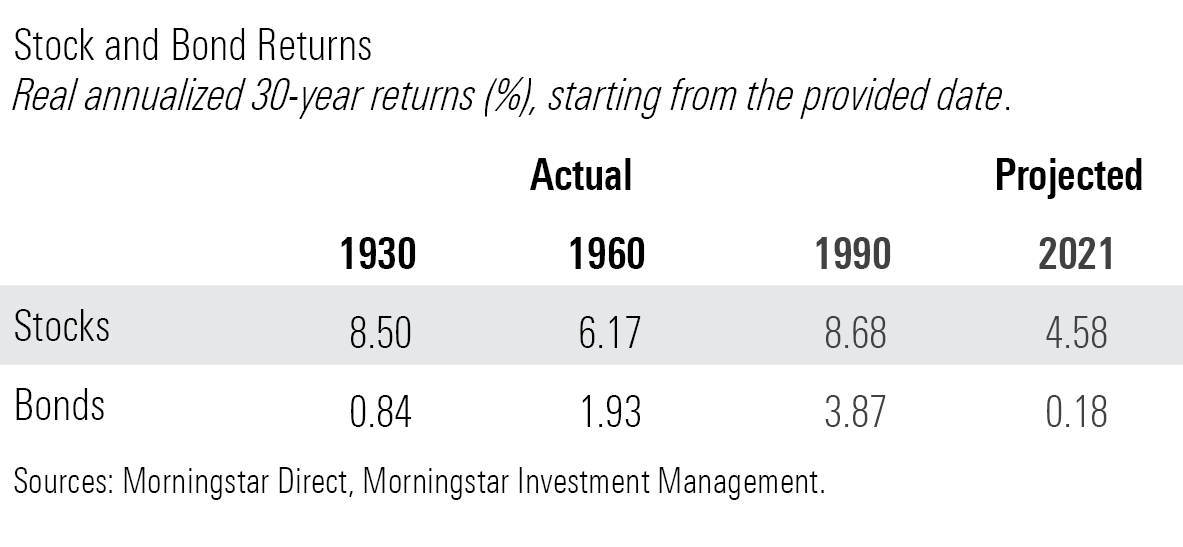

The following table shows the real annualized rates of return (that is, the after-inflation performances) for U.S. stocks and bonds over four different periods: 1) from 1930 through 1959; 2) from 1960 through 1989; 3) from 1990 through 2019; and 4) from 2021 through 2050. The first three series depict actual results, while the fourth series contains Morningstar Investment Management's estimates. The latter, of course, carries no guarantees. Nevertheless, it provides a useful testing ground, for evaluating what retirees should do if stocks cease to be unfailingly generous.

Morningstar Investment Management expects real stock returns for the next 30 years to be much lower than from 1930 through 1959, which included the Great Depression. Initially, that projection struck me as indefensibly pessimistic. But when I reconsidered the matter, I realized that stocks have recorded 5% real annualized gains over several 20-year periods, including from 2000 through 2019. So, it scarcely seems unreasonable to believe that they could do so for the next 30 years.

The bond forecast also trails history's results, but this prediction is, if anything, optimistic. The yield on 30-year Treasury Inflation-Protected Securities is currently negative 0.56%, meaning that investors who possess those securities have willingly accepted receiving half a percentage point per year less than the inflation rate. In that light, expecting even a slight gain from bonds seems hopeful.

Spending Rates

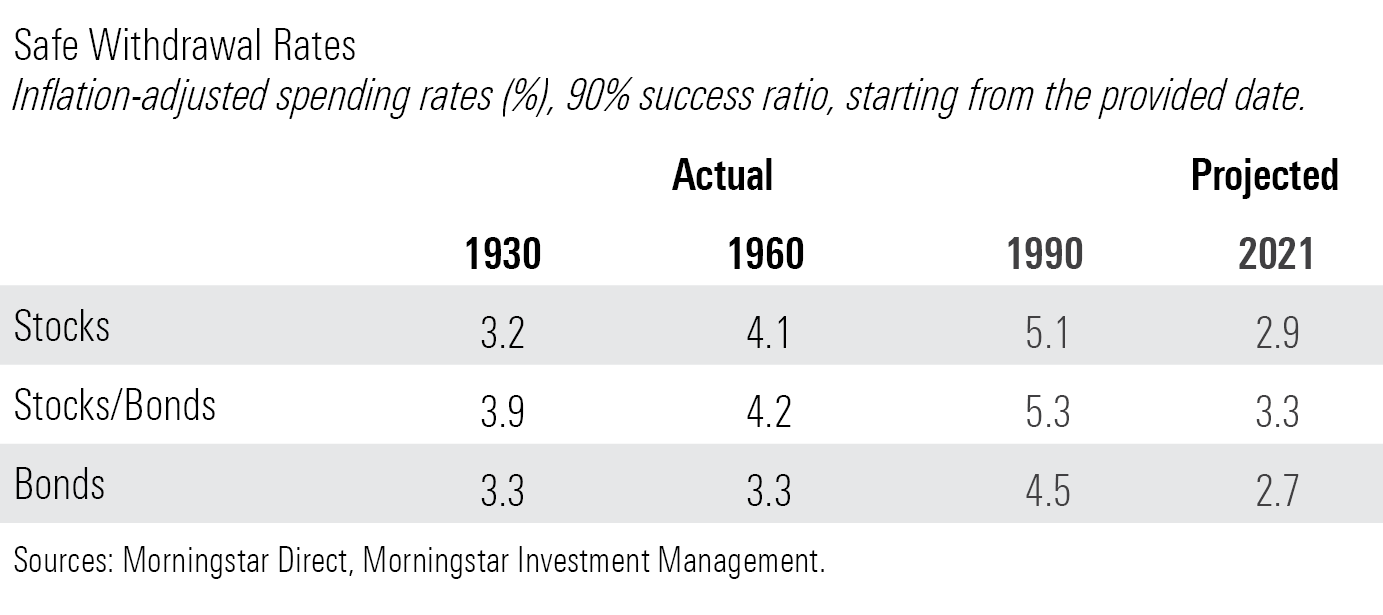

Plugging the forecasts into a withdrawal-rate model that computes safe spending rates for given levels of asset-class performances and inflation rates--for further details on those calculations, see Friday's column--generated estimates for today's crop of retirees. They appear below, along with the comparable figures for the earlier periods. (The three portfolios consist of: 1) 100% stocks, 2) 50% stocks, 40% bonds, and 10% cash, and 3) 90% bonds and 10% cash.)

The table tells three stories. First, whether aggressive, moderate, or conservative, the projected spending rate for each portfolio trails what history has permitted. Upcoming retirees should therefore reduce their withdrawal-rate expectations. Second, despite their unimpressive forecast, bonds will nearly match the spending rate that can safely be extracted from an all-equity portfolio. In the past, stock returns were so high that they fully compensated for equities' extra volatility. Morningstar Investment Management no longer believes that will be the case.

Third, balanced portfolios show well. Their calculated withdrawal rate is 40 basis points per year above that of an all-equity portfolio, which is an unusually high victory margin. Only from 1930 through 1959 did the stock/bond portfolio confer a larger spending-rate advantage. Not that Morningstar Investment Management, nor any other reputable organization, forecasts a repeat of the Great Depression. That is not the claim. The point instead is that the best time to diversify is when investments have become expensive, implying that returns may be weak.

In Summary

After taking a short detour to review the details, I can once again offer straightforward counsel. Retirees who regard the market's lessons as constant should favor equities. They need read no further than Friday's column. However, those who believe that the stock market may have finally exhausted its good fortune, such that any downturn will not promptly be followed by a sharp rally, should invest only moderately in equities. From 30% to 50% seems appropriate.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)