Bitcoin ETFs: Should You Jump on the Bandwagon?

Bitcoin believers have better options.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

Even as the first bitcoin-tracking exchange-traded fund pulled in buckets of money, ProShares Bitcoin Strategy ETF BITO was showing why funds of its kind are a bad deal for investors.

The issue isn’t with the fact that the ProShares ETF, along with another new entrant, Valkyrie Bitcoin Strategy ETF BTF are bitcoin-tracking strategies. It’s how they do it.

Rather than investing in bitcoin itself, these funds invest in bitcoin futures contracts. This may sound like a technicality, but it’s not.

This strategy--based on what we’ve seen over the past week in the futures market--could end up reducing investor returns by a double-digit percentage per year compared with the actual returns on bitcoin. And a key futures-market trading deadline at the end of this week could highlight this gap.

Not only that, the bigger these funds get, the more they could lag returns on bitcoin. As we said last week, “these aren’t the bitcoin ETFs you are looking for.”

A Big Debut

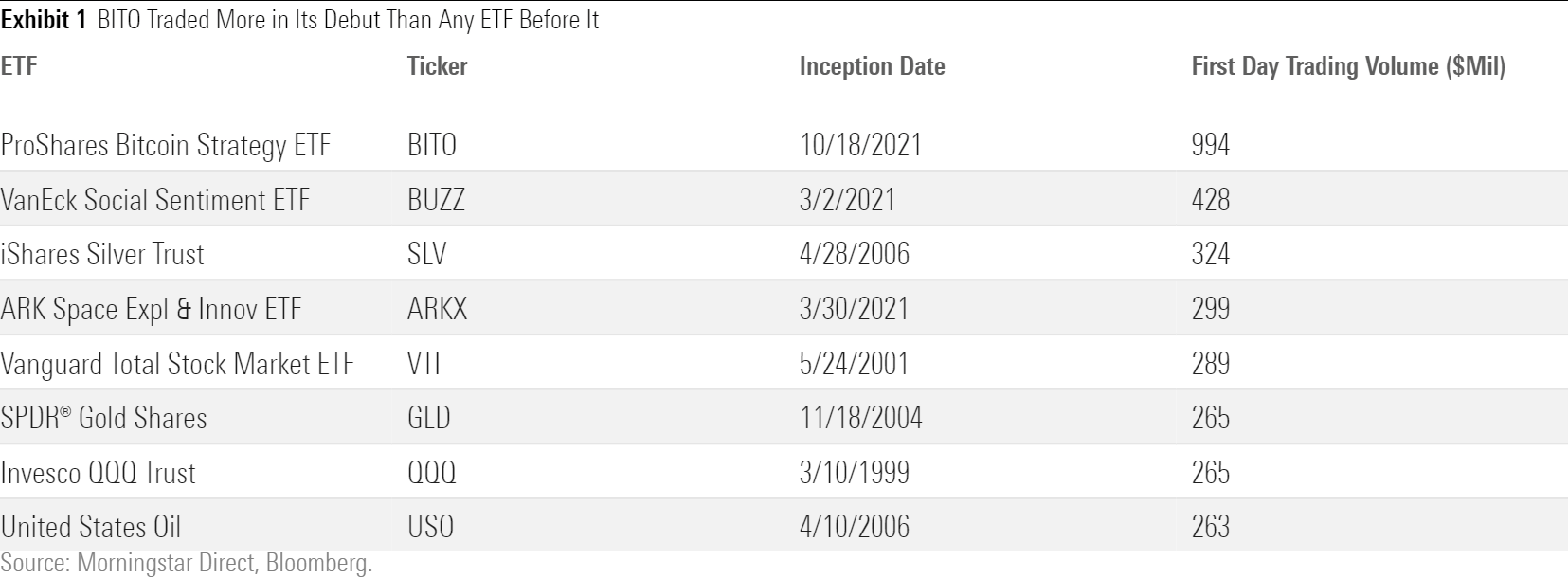

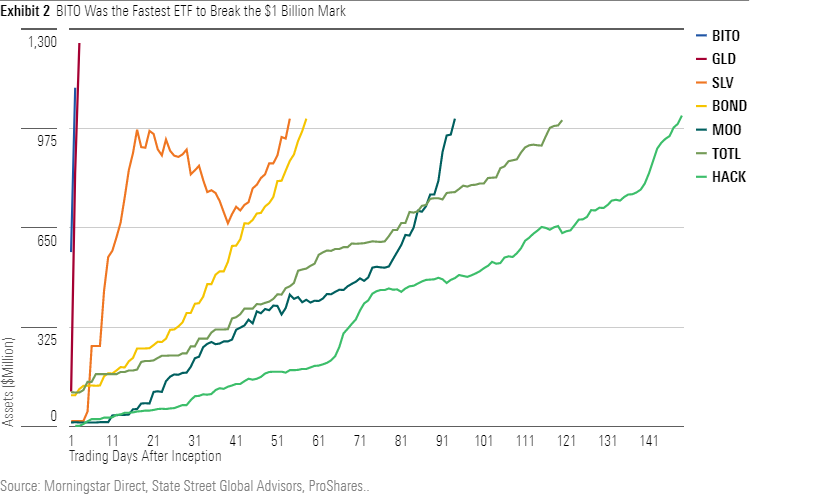

BITO’s launch broke records. It saw more trading volume on its first day than any ETF in history, and it topped $1 billion in new assets faster than any ETF that came before it.[1] BTF was a fast follower, but apparently not fast enough--its first day trading volumes were a fraction of BTO’s, and it netted about $30 million in new assets in its debut.

These Aren’t the Bitcoin ETFs You’re Looking For

BITO, BTF, and other Bitcoin(ish) ETFs that may soon follow do not invest directly in Bitcoin. Again, they do not invest directly in Bitcoin. Instead they invest in Bitcoin futures contracts. It is critical to understand the difference.

Futures contracts are an agreement between two parties to buy or sell a specific asset on a specific date in the future at a specific price. In the case of Bitcoin futures ETFs, that asset is Bitcoin (Bitcoin futures are actually cash-settled, but Bitcoin is the reference asset), that date is usually the last Friday of each month, and the price will vary, but it is based on the Bitcoin Reference Rate, or BRR, which averages Bitcoin spot prices from five major Bitcoin exchanges: Bitstamp, Coinbase, Gemini, itBit, and Kraken. Investing in Bitcoin futures is much different from investing directly in Bitcoin.

Bitcoin futures contracts, like all futures contracts, expire. Bitcoin futures ETFs will regularly sell the contracts they own and buy new ones. This process is commonly referred to as “rolling.” The costs (or benefits) of rolling futures contracts depend on the differences between their prices. When subsequent months’ contracts are trading at prices higher than the current month’s contract, the futures curve is upward-sloping. This is a state known as contango.

As an investor, contango is not the kind of dance you want to be doing. When the futures curve is in contango, futures-based strategies are forced to sell relatively low-priced contracts and purchase higher-priced ones. At risk of stating the obvious, selling low and buying high is not a successful investment strategy.

Conversely, when subsequent months’ futures contracts trade below the current month’s contract, the curve slopes downward, a state referred to as backwardation. Backwardated futures markets can give futures strategies a bit of a boost, as they will be selling high and buying low.

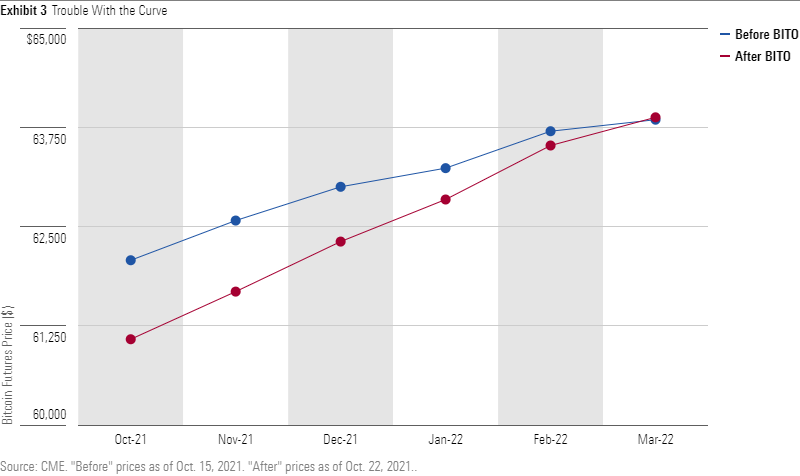

As of the close of trading on Friday, Oct. 22, the Bitcoin futures curve (see Exhibit 3) was in contango. The October contract closed at a price of $61,080, while the November contract closed at $61,680. Based on these prices, the implied annualized cost of rolling from one month to the next (also known as the roll yield) would be around 11.8%.

The costs of regularly rolling into higher-priced contracts will compound over the long term. As a result, if the futures market is typically in contango, investors who own futures contracts will experience much lower returns than those who own the asset directly. To date, this has been the case with Bitcoin. Since Bitcoin futures were launched in December 2017, the futures curve has been in contango more often than not. As a result, the Horizons Bitcoin Front Month Rolling Futures Index ER (an index that owns the front-month futures contract and regularly rolls into the next) cumulatively underperformed the spot price of Bitcoin (Source: CoinDesk) by 93 percentage points from Dec. 15, 2017, through Oct. 21, 2021. Investors relying on futures contracts for long-term exposure to bitcoin are likely going to leave a lot of coin on the table.

Clearly, roll costs have been a headwind for investors in Bitcoin futures. Now that Bitcoin futures ETFs have arrived, this headwind may become stronger and more persistent. Since BITO launched on Oct. 18, the futures curve has gotten steeper (see Exhibit 3). The implied annual roll cost at the end of Friday, Oct. 15 (the last trading day before BITO launched) was 9.7% versus 11.8% as of the end of trading on Oct. 22.

Bitcoin futures ETFs’ arrival has created a large and growing source of demand for both the front-month futures contracts as well as those further out on the curve. This has clearly had an impact on futures prices, and it could have meaningful, negative long-term impacts on investors in these funds. This impact will be felt in the coming days, as the October Bitcoin futures contract expires on Friday, Oct. 29.

Capacity Concerns

BITO’s success in gathering assets may be cause for concern. This is because there are limits on how many futures contracts these funds can own. On Sept. 30, 2021, CME Group announced that the limit on the number of front-month futures contract any one entity could own would increase to 4,000 from 2,000, beginning with the November 2021 contract. As of Oct. 22, BITO owned a total of 3,812 Bitcoin futures contracts, split between the soon-to-expire October contract and the soon-to-be-front-month November contract. The fund’s rapid growth has it quickly pushing toward its limits.

If BITO and its peers continue to take in new money, these limits will loom larger, and the steps that they take to stay in bounds may work against them. The funds can avoid hitting position limits by spreading their assets across multiple futures contracts. But as they move further out on the futures curve, they risk pushing the prices of longer-dated, less-liquid futures higher, potentially increasing roll costs in the process. Also, the more of their assets these funds invest in longer-dated futures contracts, the less sensitive their prices will be to movements in Bitcoin spot prices.

In the event that Bitcoin futures ETFs hit absolute limits on their overall positions in Bitcoin futures contracts, there is a chance that they would be forced to stop issuing new shares. In such an event, the ETFs’ prices could come unmoored from the value of their assets. There are precedents here: Both United Stated Oil Fund USO and United States Natural Gas Fund UNG experienced such dislocations in the past after their capacity to tap into their underlying markets via futures and other derivatives was tapped out.

How big is this risk for Bitcoin futures ETFs? It is difficult to say, as it depends on how much new money they rake in, how far out the curve they can spread it, other measures their sponsors may take to throttle inflows, and whether the CME will be accommodative with its position limits, increasing them further as they just did at the end of September. Until there is more clarity, capacity concerns will linger.

There Are Better Options

Futures-based ETFs are a lousy option for long-term exposure to Bitcoin. Roll costs and fund fees will likely lead these funds’ long-term returns to lag the performance of Bitcoin--probably by a wide margin. Capacity concerns and the potential for the ETFs’ price to dislodge from their net asset values are a wild card to consider. All told, these funds are best left for the traders, who will gravitate to them based on Bitcoin futures’ volatility (traders love volatility) and the fact that many of these funds will also have options contracts tied to them (BITO already does).

There are so many ways for Bitcoin believers to purchase Bitcoin directly, most of them far superior alternatives to buying futures-based ETFs.

[1] Exhibits 1 and 2 exclude ETFs that were launched with significant seed investment.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HTLB322SBJCLTLWYSDCTESUQZI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TAIQTNFTKRDL7JUP4N4CX7SDKI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)