What's in a Meme ETF?

A non-clickbait look into a few clickbait tickers.

/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)

A wave of new investors has flocked to the market during the post-pandemic market boom, and investment firms have been actively trying to get in front of them. Some have taken to social media to dole out investing content. Take, for example, this TikTok from Fidelity about mutual funds. From a marketing perspective, it makes sense to leverage these platforms to reach younger investors. But does turning online chatter about today's hottest stocks into an actual portfolio make sense? Some asset managers think so, and they've launched a number of funds that try to leverage insights from their investors and social media platforms into market-beating returns. This article will dissect four of these exchange-traded funds: Are they worth a shout-out, or they should go on the blocked list? The lineup features VanEck Social Sentiment ETF BUZZ, Tuttle Capital Management FOMO ETF FOMO, SoFi Social 50 ETF SFYF, and the recently filed but yet-to-be-launched Roundhill MEME ETF.

Know Your Memes

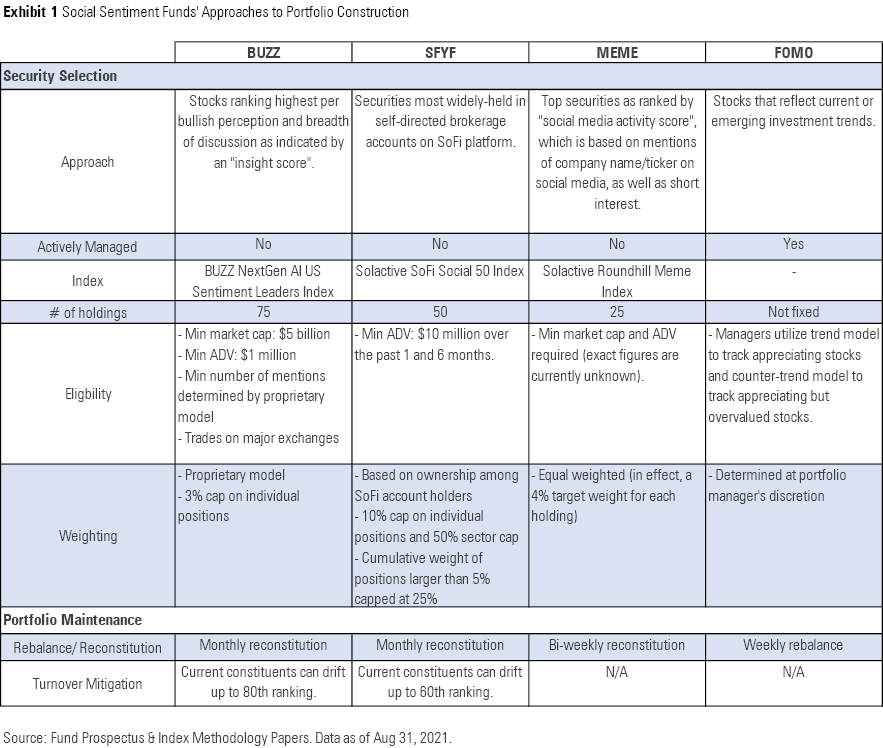

As with any investment strategy, an assessment of the investment process is the centerpiece of our due-diligence effort. Exhibit 1 summarizes the four funds’ approach to portfolio construction.

Step 1: Picking Stocks

Each of these funds has a very different stock-picking strategy.

SFYF has the most straightforward approach. The strategy sweeps in the 50 most-popular stocks held by clients of its brokerage platform. The accounts it surveys are self-directed, so the fund is getting its picks straight from the hivemind of SoFi’s individual investor clients. This also means it is exclusively dependent upon SoFi’s base of customers and their investing preferences and habits. As SoFi has yet to achieve a major slice of the brokerage market, the makeup of SoFi accounts’ owners is unlikely to be representative of the average U.S. investor. According to the fund’s prospectus, there were more than 300,000 self-directed SoFi accounts as of May 2021. Given that SoFi started out as a student loan refinancing service focusing on young, high-income individuals, its individual investor community will likely mirror this demographic for a while. So far, SFYF’s top holdings have ranged from industry giants such as Amazon.com AMZN and Shopify SHOP to the meme-iest of meme stocks like AMC Entertainment AMC and GameStop GME.

BUZZ and MEME take a somewhat similar tack. Both funds’ indexes rank stocks based on social media chatter. A few factors can lead to meaningful differences between the two benchmarks’ portfolios, including the platforms they gather data from, how long their lookback periods are, and how they identify and gauge sentiment. MEME’s index uses trailing 14-day data to score stocks, a relatively short time span that can help it stay on top of more dynamic trends. Although BUZZ does not disclose its exact lookback period, its index methodology mentions reviewing four quarters of data on a rolling basis. BUZZ’s relatively longer lookback explains, in part, why it was late to include some Reddit darlings like GameStop and AMC. While both funds’ indexes are fairly opaque, we can gauge the general objectives of their approaches. BUZZ looks for stocks with bullish sentiment and considers the reliability of the social media users in deriving its signal. MEME’s index screens for high short interest in addition to general social sentiment indicators. The latter is a more-opportunistic approach, while the former tries to control for the quality of its picks.

SFYF, BUZZ, and MEME’s indexes have minimum trading volume and/or minimum market-cap requirements for securities to be considered for inclusion. These requirements can help them avoid illiquid securities and mitigate turnover costs, but they can also omit a significant portion of the investment opportunity set. For example, BUZZ’s $5 billion minimum market-cap requirement filters out virtually all small- and micro-cap stocks. For reference, the median market cap for the S&P SmallCap 600 Index is around $1.5 billion, the CRSP U.S. Small Cap Index's is $2.9 billion, and the Russell 2000 Index's is $1.2 billion.

FOMO, the lone actively managed ETF with a meme-y theme, has been around for just a few months. Its short track record does not offer much insight into the manager’s investment style. The fund’s prospectus claims it incorporates multiple investment models to catch stocks with “increasing value,” including ones that are overvalued. The fund started out on the value side of the style spectrum, with IBM IBM and Cisco CSCO occupying some of the top spots in its portfolio. It briefly shifted gear into mid-growth territory and has since moved toward the large-growth portion of the Morningstar Style Box. The fund also takes on large positions in names outside the United States, such as Bilibili BILI and NIO NIO. And while it is wide-ranging, the portfolio tends to be fairly compact, typically holding 70-100 stocks.

Step 2: Weighting Stocks

Each of these funds weights stocks differently. MEME’s index weights stocks equally. SFYF weights its holdings based on how much money its brokerage clients have invested in them at the end of each month. BUZZ’s approach isn’t very transparent, employing a proprietary weighting model. FOMO’s position sizes are determined at the portfolio manager’s discretion.

The number of stocks each fund holds and their weighting schemes result in varying degrees of concentration risk. FOMO spreads its bets quite evenly. Its top 10 holdings only claim around 15% of its assets. BUZZ makes more concentrated bets. The fund parks around 30% of its assets in its top 10 holdings. Both BUZZ and SFYF implement weighting constraints on individual position to prevent firm-specific risk. SFYF does have a sector weight constraint, but capping sector exposures at 50% of the portfolio is hardly confining. While larger wagers on certain stocks or sectors may result in larger rewards, they could also be a bust.

Step 3: Keeping Up With The Memeses

Trends in social sentiment tend to have a short life span. To keep up, these funds reconstitute and rebalance much more frequently than their typical broad-market counterparts. This should help them maintain purer exposure to their mandate. But more regular rebalancing will lead to higher turnover and associated trading costs, which can eat away at returns. BUZZ and SFYF attempt to curb turnover by implementing buffer rules that allow current portfolio holdings to temporarily stray. By virtue of being an actively managed strategy, FOMO’s turnover hinges on the portfolio manager’s opinions and transactions. Thus far, its turnover has been fairly high.

The End Product

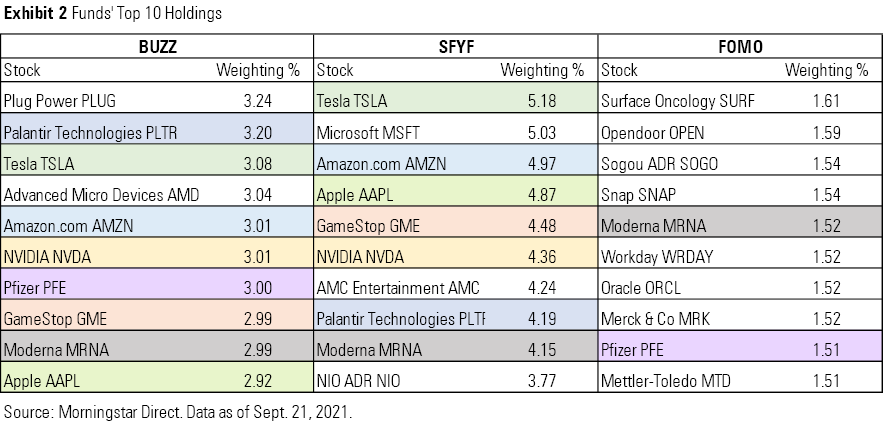

The top spots in these portfolios house a mix of leading growth stocks (Tesla TSLA, Apple AAPL, and NVIDIA NVDA, for example) and popular meme stocks (like Plug Power PLUG and GameStop). No matter what you think about each of these stocks individually, the variety on display in Exhibit 2 goes to show how different these portfolios will look despite having vaguely similar approaches. Though there is some overlap between BUZZ and SFYF’s top 10, the rank and weight of the positions varies. Take AMC, for instance. As of Sept. 21, 2021, the stock was the 13th-largest position in BUZZ’s portfolio, the 7th in SFYF’s, and the 65th in FOMO's. At the end of August 2021, AMC was the largest holding in all three portfolios. And even then, its weight varied quite a bit across each fund.

All Sizzle?

All four funds are making a similar bet: that sentiment contains a signal that can be turned into outperformance. But is there wisdom in these crowds, and are these funds capturing it?

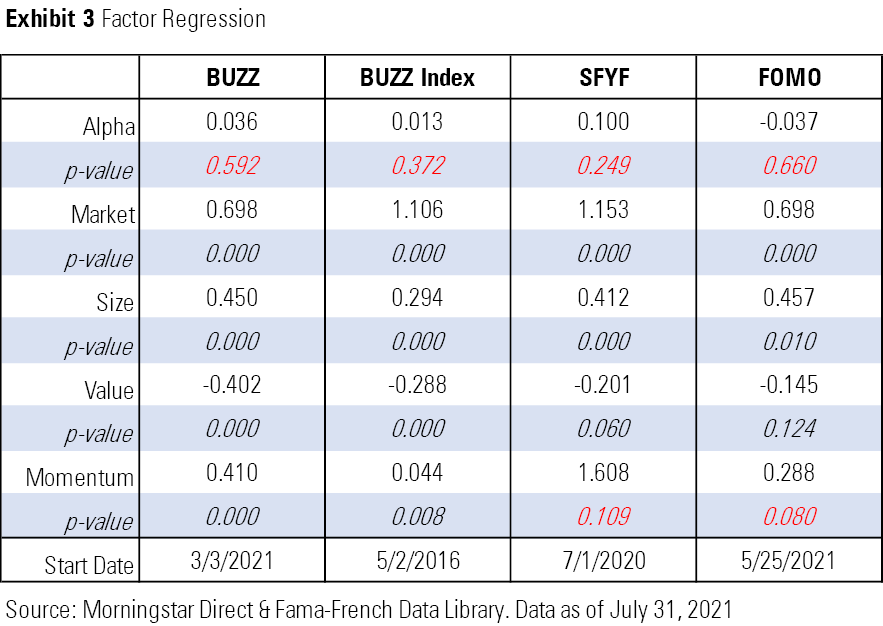

Let’s take a look at a factor regression to try to understand what’s really driving these funds’ returns. Is leveraging social sentiment and investor behavior backing them into known drivers of stock returns? Exhibit 3 contains the regression results of the four-factor model dating back to each fund’s inception. Given that each of the three funds has a brief history, it is important to take these results with a grain of salt. I also ran the regression on BUZZ’s benchmark index to get a longer lookback. It is important to note that SFYF switched from the Solactive SoFi U.S. 50 Growth Index to the Solactive SoFi Social 50 Index on June 30, 2020. Thus, I have used its performance history since the index change instead of going back to its May 7, 2019, inception.

While some might expect social sentiment and momentum to be tied together, only BUZZ and its index have a positive, statistically significant loading on momentum. SFYF’s momentum loading is positive but not statistically significant. The most consistent and significant factor driving these funds’ returns seems to be their sensitivity to the market--their beta. This is not surprising, as these funds tend to hold large stakes in the popular technology stocks that have propelled the market over the past year or so.

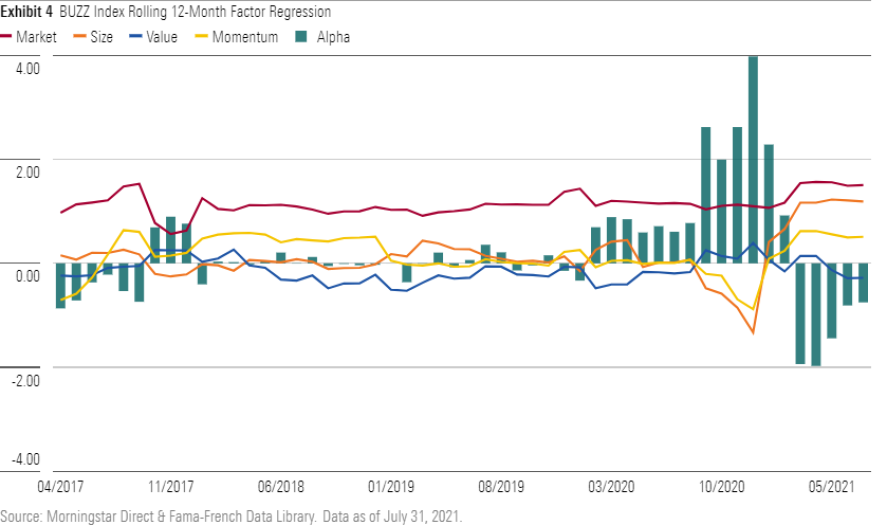

A deeper dive into BUZZ’s index reveals some interesting details. Exhibit 4 plots the rolling 12-month factor loading for the BUZZ NextGen AI U.S. Sentiment Leaders Index. It’s still clear that the market is doing the heavy lifting here, but the portfolio has benefited from its momentum tilt and small-cap exposure during the past year. Its bets on smaller momentum stocks, such as GameStop and Novavax NVAX, boosted its returns as markets bounced back from their early-2020 lows. However, while it did pick up Zoom ZM, Shopify, and Tesla heading into March 2020, this portfolio also held on to its stakes in General Electric GE and JPMorgan Chase JPM, which ultimately dragged it down. This exemplifies the uncertainty that comes with relying on online chatter to assess which way the wind might be turning next. There is no guarantee that social media consensus will be correct, especially in volatile markets where opinions can diverge wildly and turn on a dime.

Don’t Be Uncool

Staying on top of current trends is no easy feat, but what’s undeniably uncool is losing money. While nothing is stopping investors from putting some “funny money” in one of these funds, it is essential to do some basic due diligence and exercise caution. At the end of the day, these funds are chasing an investment theme that may prove a passing fad. Our framework for assessing these funds is required reading for those considering one of these options, or any thematic fund for that matter. While some thematic funds will deliver eye-popping returns, the fact is that most fail in the long run.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-09-2024/t_e87d9a06e6904d6f97765a0784117913_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)