Investors Can Ignore Debt-Ceiling Showdowns ... Usually

Debt-ceiling fights and government shutdowns have been nonevents for stocks, with one big exception.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

The news is once again filled with headlines about a legislative logjam in Congress that threatens to leave the United States unable to pay its debts, shut down the government, and destabilize the economy and the markets.

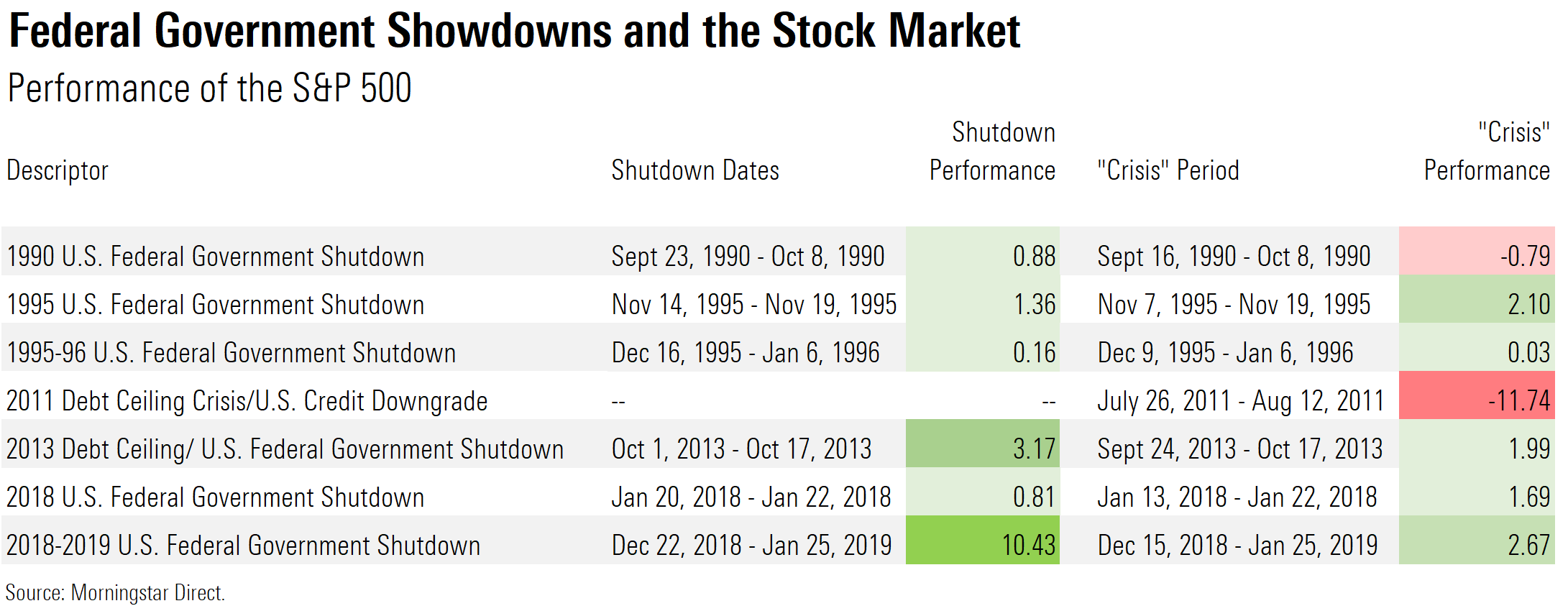

If this story sounds familiar, that’s because it is. Since 1980, there have been nine government shutdowns, and congressional games of chicken in several other years, around what is known as the "debt ceiling"--the legislative limit on how much money the U.S. government can borrow.

While this makes for great political theater and fodder for pundits, the common denominator is that this drama has had little impact on stock and bond markets. Take the October 2013 debt-ceiling battle that led to a 16-day shutdown of the federal government. From the week before the debt-ceiling deadline through its resolution, the stock market was essentially unchanged.

Of course, there are always exceptions--the big one being August 2011, when the debt-ceiling battle led to a surprise downgrade of the United State’s credit rating, and turmoil in the stock and bond markets ensued.

With the economic recovery from the coronavirus pandemic slowing amid the delta variant’s surge, and with investors simultaneously worried about rising inflation, the U.S. economy remains vulnerable to a shock. At the same time, stock prices are at record highs and by many measures--including Morningstar’s--richly valued, which leaves investors vulnerable as well.

The wrangling invariably revolves around the limit set by Congress on how much money the U.S. government can borrow to pay its debts and bills. The debt ceiling is largely a technical issue around how the federal government manages its finances that is separate from the appropriations process that determines how much the government spends and on what.

This time around, it looks like Congress will avoid forcing a government shutdown. But without an increase in the debt ceiling, forecasts say the U.S. could run out of money to pay back holders of U.S. Treasury bonds--aka default on the government’s debt--as soon as mid-October.

A default by the U.S. government on its debt has the potential to be calamitous, shaking global investor confidence in our markets. Thankfully, cooler heads have always prevailed.

But that is exactly what has made the debt ceiling into prime political theater for the past two decades.

So, we took a look at seven past debt-ceiling and government-shutdown episodes to see if history shows how concerned investors should be about this political brinkmanship.

To run the numbers, we examined two sets of scenarios. The first is actual government shutdowns, and the second is debt-ceiling crises where a last-minute deal was hammered out. To arrive at the time frames to examine, we considered that, while the political posturing begins well before the drop-dead date, investors generally tune out the early noise. But to capture any positioning as the deadline drew near, we looked at performance beginning in the week leading up to the date the Treasury Department said it would expect to run out of funding and continuing through the market close on the day after the deal was reached. (With the exception of the 2011 instance where we extended the period after the U.S. credit rating downgrade.)

For the most part, the debt-ceiling showdowns and government shutdowns have turned out to be nonevents for the market.

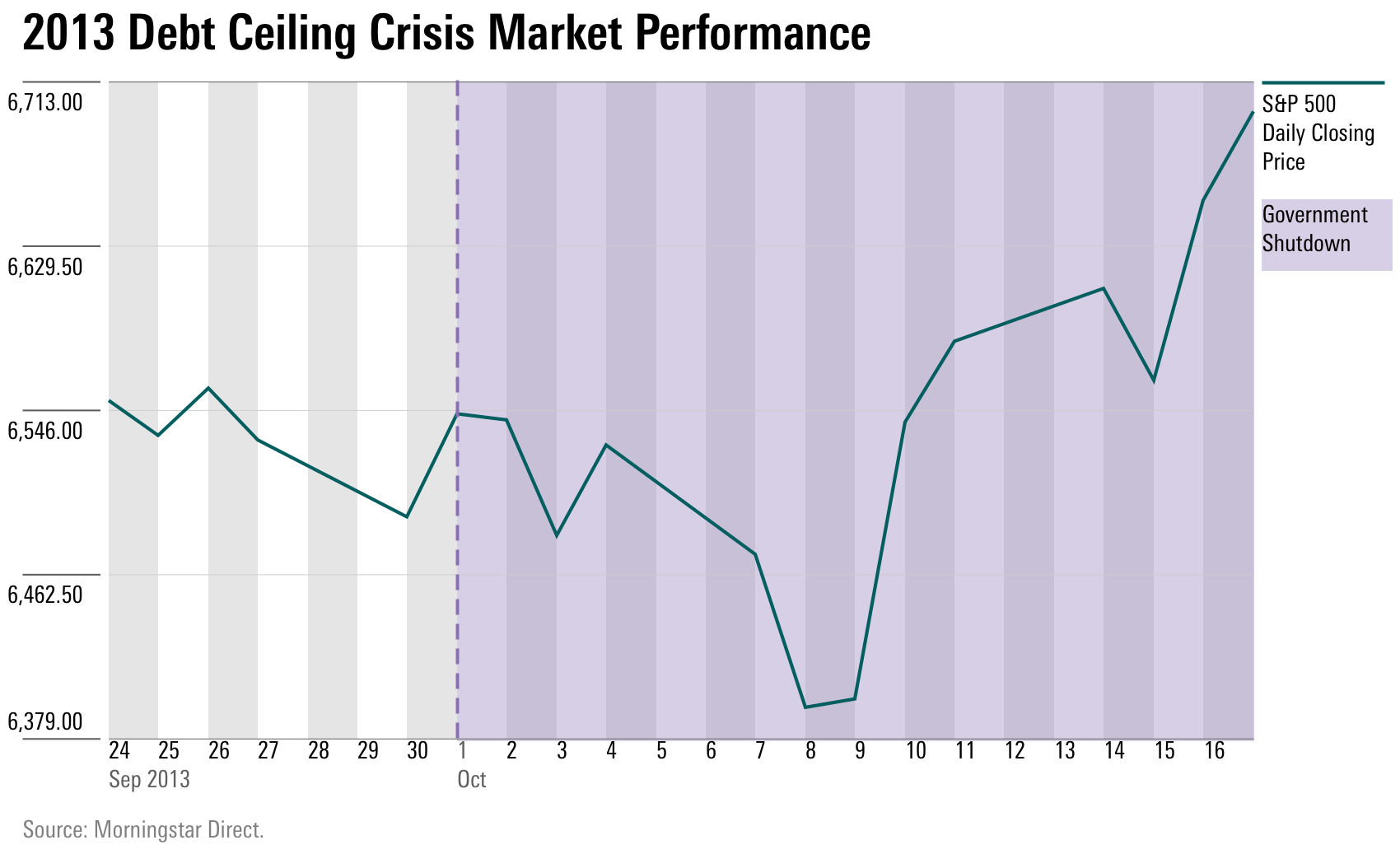

Taking a close look at the

, the political back and forth began in January of that year, but a combination of congressional compromises and maneuvering by the Treasury Department staved off a government shutdown and threat of default into October. A partial government shutdown began on Oct. 1, and the Treasury Department estimated it would run out money to pay the country’s debts in mid-October. The episode ended with legislation passed on Oct. 16, and federal workers returned to their jobs on Oct. 17.

Measuring from a week before the government shutdown through its resolution, the S&P 500 rose a grand total of 2%, more than reversing a decline of about the same magnitude suffered during the crisis period.

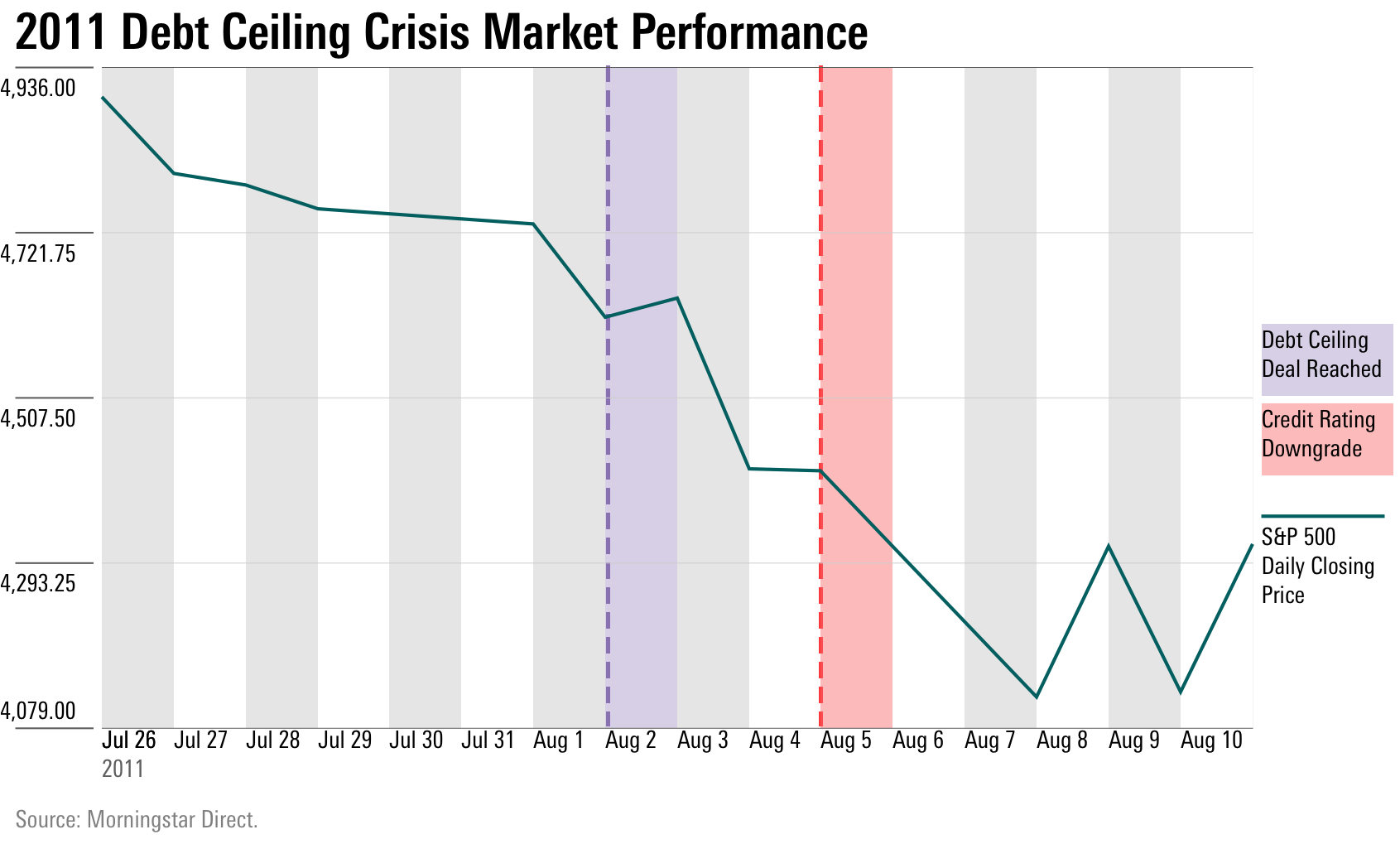

This kind of scenario has been the rule through the seven debt-ceiling debates we examined. But the exception that proves that investors should always be on their toes came in 2011.

That summer, investors were on edge amid the ongoing debt crisis in the eurozone, and memories of the 2008 global financial crisis were fresh. As the debt-ceiling limit approached, the U.S. stock market was already on the decline, falling more than 6% in the week leading up to Aug. 2, the day the government was expected to run out of money. Then with two days to spare, Congress reached a deal on lifting the debt ceiling, and it seemed investors could turn their attention elsewhere, especially to the still unsettled situation in Europe.

However, in the spring and early summer, ratings agencies warned that the pristine credit rating of the United States was in jeopardy of being cut thanks to the growing budget deficit and political polarization. Investors, for the most part, shrugged these warnings off. Then on Friday, Aug. 5, after the stock market closed for the day, investors were shocked when Standard and Poor's lowered the credit rating of the United States, sending markets into turmoil. That Monday, the S&P 500 fell another 6.6%.

In its announcement of the ratings downgrade, S&P said, “The downgrade reflects our view that the effectiveness, stability, and predictability of American policymaking and political institutions have weakened at a time of ongoing fiscal and economic challenges.” It added, “The difficulties in bridging the gulf between the political parties over fiscal policy ... makes us pessimistic about the capacity of Congress and the Administration to be able to leverage their agreement this week into a broader fiscal consolidation plan that stabilizes the government's debt dynamics any time soon.”

Needless to say, it’s chilling to read these words a decade later, at a time when polarization has only gotten more entrenched and budget deficits are the largest on record. Knock on wood, this time around, that the debt ceiling will be the kind of nonevent it usually is.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CFV2L6HSW5DHTFGCNEH2GCH42U.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/7JIRPH5AMVETLBZDLUSERZ2FRA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YWKBIVULT5DGJEIGAJGBA6H5ZA.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)