4 Undervalued Sustainable Stocks

Given their competitive advantages, these companies are poised to do well in a sustainable world.

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

As the world’s focus on environmental, social, and governance concerns intensifies, investors are asking how to find companies that pursue sustainability initiatives and also have a good chance of outperforming the market.

To find these kinds of companies, we looked at the Morningstar U.S. Sustainability Moat Focus Index. The index is designed to include companies with strong ESG characteristics and durable competitive advantages that help them outperform industry competitors.

To measure how effectively a company is managing environmental, social, and governance issues, the index incorporates the following data points:

- Sustainalytics' ESG Risk Scores, ratings that look at how much industry-specific ESG risk a company is exposed to and how well the company is managing that risk.

- Product Involvement metrics that measure the percentage of a company's revenue that is generated from controversial topics such as animal testing, pesticides, and tobacco.

- Sustainalytics' Controversy research, which keeps a daily pulse on corporate scandals and discusses the extent that relevant controversies can affect a company's financials as well as how the company mitigates controversy risk.

- Carbon Risk scores that give insight into companies that are well-positioned to succeed in a low-carbon economy.

The index also utilizes the Morningstar Economic Moat Rating, our analysts’ designation for companies with long-term competitive advantages that allow them to earn outsize profits over time. Every company in the index maintains an economic moat rating of wide, meaning that their competitive advantages are expected to last over 20 years.

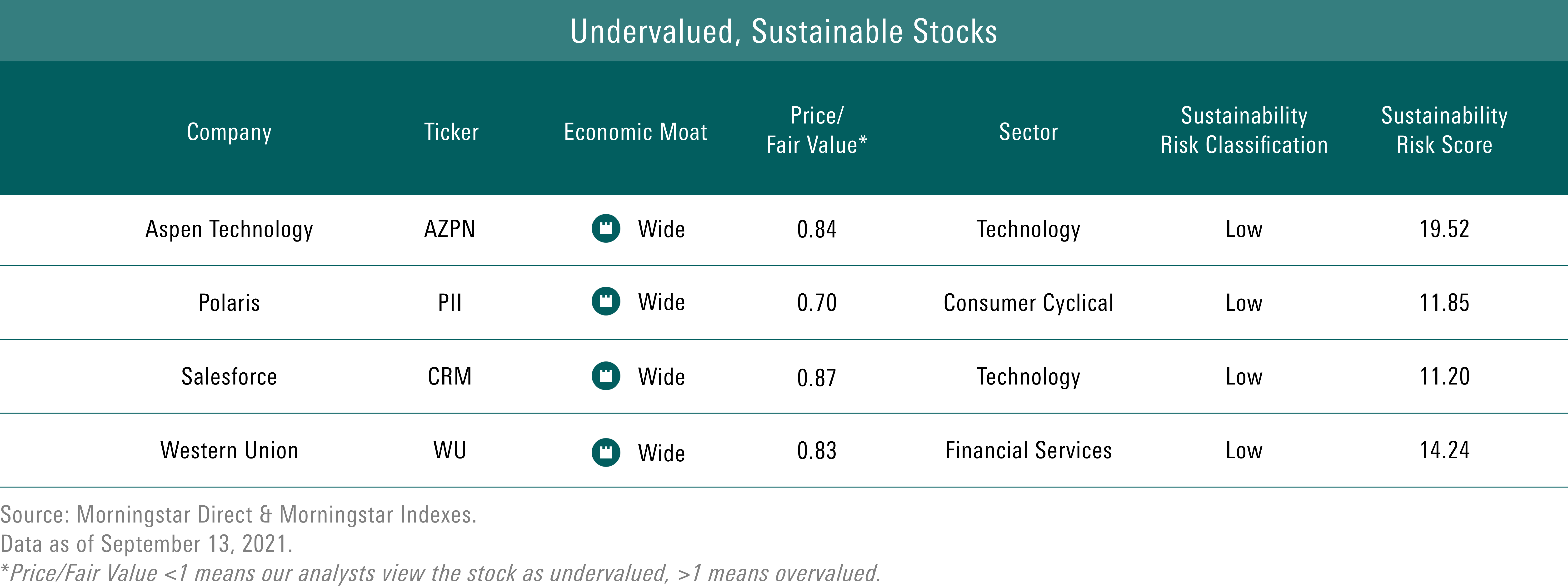

Here are four companies from the Sustainability Moat Focus index that our analysts believe are trading at bargain prices:

Here's a little bit about what our analysts have to say about each name.

Aspen Technology AZPN

“We believe Aspen Technology is a leader in the process automation software niche. We think the firm has ample room to grow over the next decade within its existing customer base, which tends to be particularly sticky, as evidenced by our wide moat rating.

“Aspen’s software optimizes asset design, operations, and maintenance in complex industrial environments. The AspenOne software platform helps improve process-oriented plant efficiency and thereby lower capital intensity, increase working capital efficiency, and improve margins. In an industry characterized by thin margins, users are obviously searching for ways to wring even modest improvements to operations out of its facilities, given a price tag of billions of dollars for a new oil refinery. A typical refinery will run 24 hours a day, seven days a week, and process around 200,000 barrels, so a 1% improvement in throughput can drive millions of dollars of operating profit. Aspen’s software enables improved efficiency, including throughput improvement, emissions reduction, and energy consumption.

“Aspen enjoys a roster of more than 2,300 clients and generates more than 60% of its revenue from outside the U.S. Eighty percent of revenue is derived from the firm’s top 350 customers, with about 60% of revenue from its engineering suite. Asset performance management, or APM, is generating a lot of interest from both new and existing clients, leading Aspen to invest more in both product and sales capacities.

“We think the broader market for industrial automation is in excess of $200 billion. However, Aspen’s narrow focus on software for process automation limits its total addressable market, or TAM, to $5 billion. We expect the TAM to grow over time as management adds features to the AspenOne platform and the company moves more meaningfully into areas outside of its core markets. APM should be a key growth driver in this regard over time. Aspen has made some diversification strides outside of its core petrochemical markets and now generates 5%-10% of annual spending from pharmaceuticals, paper and pulp, metals and mining, and consumer packaged goods. We expect these areas to grow within the mix over the next decade.

Dan Romanoff, Equity Analyst

Polaris PII

“Polaris is one of the longest-operating brands in powersports. We believe that its brands, innovative products, and lean manufacturing yield the firm a wide economic moat and that it stands to capitalize on its research and development, solid quality, operational excellence, and acquisition strategy. However, Polaris' brands do not benefit from switching costs, and with peers innovating more quickly than in the past, it could jeopardize the firm's ability to take price and share consistently, particularly in periods of inflated recalls or aggressive industry discounting.

“Polaris had sacrificed some financial flexibility after its transformational acquisitions of TAP (2016) and Boat Holdings (2018), but debt-service metrics have been rapidly worked down via EBITDA expansion and cost-saving scale benefits (with debt/adjusted EBITDA set to average less than 1 times over our forecast). This unlocks Polaris' ability to continue to serially acquire strategic businesses (with opportunities likely in the boat and parts and accessories segments), which could help stimulate incremental demand. For now, we anticipate a 21% top-line organic lift in 2021, as Polaris continues to backfill dealer inventory, before returning to more normalized mid-single-digit shipment growth in 2022 (with scarce dealer inventory levels remedied in 2023). International (low-double-digit percentage of sales) expansion over the long-term also remains promising and could drive demand upside, particularly as Polaris increases its global operating presence with a wider physical presence abroad.

“As evidenced by solid ROICs (at 17%, including goodwill, in 2020), Polaris still has topnotch brand goodwill in its segments, supporting consumer interest and indicating the firm's brand intangible asset is intact. However, with constraints in the supply chain, 2021 could see some volatility in market share gains, depending on the availability of certain products at retail (the motorcycle segment suffered this plight in the second fiscal quarter). We plan to watch market share trends unfold to ensure market share stabilization persists, signaling the firm's competitive edge is intact.

Jamie Katz, Senior Equity Analyst

Salesforce CRM

“We believe Salesforce.com represents one of best long-term growth stories in software. Even as revenue growth is likely to dip below 20% for the first time at some point in the next several years, we believe ongoing margin expansion should continue to compound earnings growth of more than 20% annually for much longer.

“After introducing the software-as-a-service model to the world, Salesforce.com has assembled a front-office empire that it can build on for years to come, in our view. Sales Cloud represents the original salesforce automation product, which streamlined process management for sales leads and opportunities, contact and account data, process tracking, approvals, and territory tracking. Salesforce.com’s critical differentiator was that the software was accessed through a web browser and delivered over the Internet, thus inventing the SaaS software delivery model. Service Cloud brought in customer service applications, and Marketing Cloud delivers marketing automation solutions. These solutions encompass nearly all aspects of customer acquisition and retention and, in our view, are mission-critical. Salesforce Platform also offers customers a platform-as-a-service solution, complete with the AppExchange, as a way to rapidly create and distribute apps. We believe this further strengthens the substantial community of Salesforce users.

“In our view, Salesforce will benefit further from natural cross-selling among its clouds, upselling more robust features within product lines, pricing actions, international growth, and continued acquisitions such as the recent Tableau deal and the pending Slack deal. Salesforce is widely considered a leader in each of its served markets, which is attractive on its own, but the tight integration among the solutions and the natural fit they have with one another makes for a powerful value proposition, in our view. To that end, more than half of enterprise customers use multiple clouds. Further, customer retention has gradually improved over time and is better than 90%, which we expect to grind higher still in the coming years.

Dan Romanoff, Equity Analyst

Western Union WU

“Western Union's primary macroeconomic exposure is to employment markets in the developed world, as the search for better economic opportunities is the fundamental driver for money transfers. While conditions have improved over time in the United States and Europe, a region that is about equally important for Western Union as the U.S., growth remains modest, with new entrants adding to the issues for legacy operators like Western Union. At this point, we don't see a catalyst to improve the situation, although we expect solid growth in the very near term as the industry bounces back from pandemic-related declines. We continue to believe Western Union has a wide moat based on its sizable scale advantage, but with a stagnant top line, the value of the moat going forward could be questioned.

“Another major issue for Western Union is the industry shift toward electronic methods of money transfer. The company has been actively building out its presence in electronic channels in recent years to adapt to the change in the industry. Given the spike in digital transfers since the beginning of the pandemic, with Western Union seeing an 81% year-over-year increase in transaction growth last year, this area of the company's business jumped to 20% of revenue in 2020. We believe the firm's aggressive approach is the best strategy as Western Union positions itself to maintain its scale advantage despite the shift. In our view, scale and market share across all channels will be the dominant factor in long-term competitive position, and Western Union appears to be maintaining its overall position. However, the growth that the company is seeing in digital transfers does not appear to be leading to strong overall growth, and we don't expect this situation to change.

Brett Horn, Senior Equity Analyst

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

Sustainalytics is an environmental, social, and governance and corporate governance research, ratings, and analysis firm. Morningstar acquired Sustainalytics in 2020. Sustainalytics provides ESG scores on companies, which are evaluated within global industry peer groups, and tracks and categorizes ESG-related controversial incidents on companies. Morningstar uses Sustainalytics’ company level ESG analytics to calculate ratings for managed products and indexes using Morningstar’s portfolio holdings database.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZEMES5XIZBD2LHOJ4CE4VEBM6I.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)