7 Wide-Moat Stocks in Healthcare to Buy

We think the market is over-reacting to new drug pricing proposals, creating a buying opportunity.

Stocks of the major drug manufacturers recently took a hit as the U.S. Department of Health released details of a plan to address high drug prices. The plan lists three policy ideas: negotiating drug prices for those covered by Medicare, capping the out-of-pocket costs in Medicare Part D, and responding to manufacturers that raise prices greater than the inflation rate. Other variations of these policies are already making their way through Congress in the form of the Democrat-led HR.3 Act and bipartisan Senate Finance Committee drug pricing package.

Worried about how these proposals might affect the profitability of Big Pharma, investors have shunned the drugmakers. IShares U.S. Pharmaceuticals ETF IHE has declined 3.2% in September as of this writing and trails the performance of the overall healthcare sector by more than 12 percentage points and the U.S. market by 20 percentage points over the trailing year.

Despite the proposal concerns, Morningstar healthcare strategist Karen Andersen doesn’t see a reason to worry. “We expect Congress will struggle to pass any system that includes significant Medicare price negotiation, such as pegging prices to international prices or deeply discounted (Medicaid, VA) U.S. prices, given pressure from more moderate Democrats in the Senate,” she says. The razor-thin democrat majority will make significant healthcare system changes even more difficult. Readers can learn more about Andersen’s perspective from her recent stock strategist note.

On how the news might impact our healthcare stock’s valuations, Andersen says, “We don’t expect any changes to fair value estimates or moat ratings for our biopharma coverage. We continue to expect innovative drugs will carry strong pricing power, a core pillar in the valuations and moat ratings for the industry.”

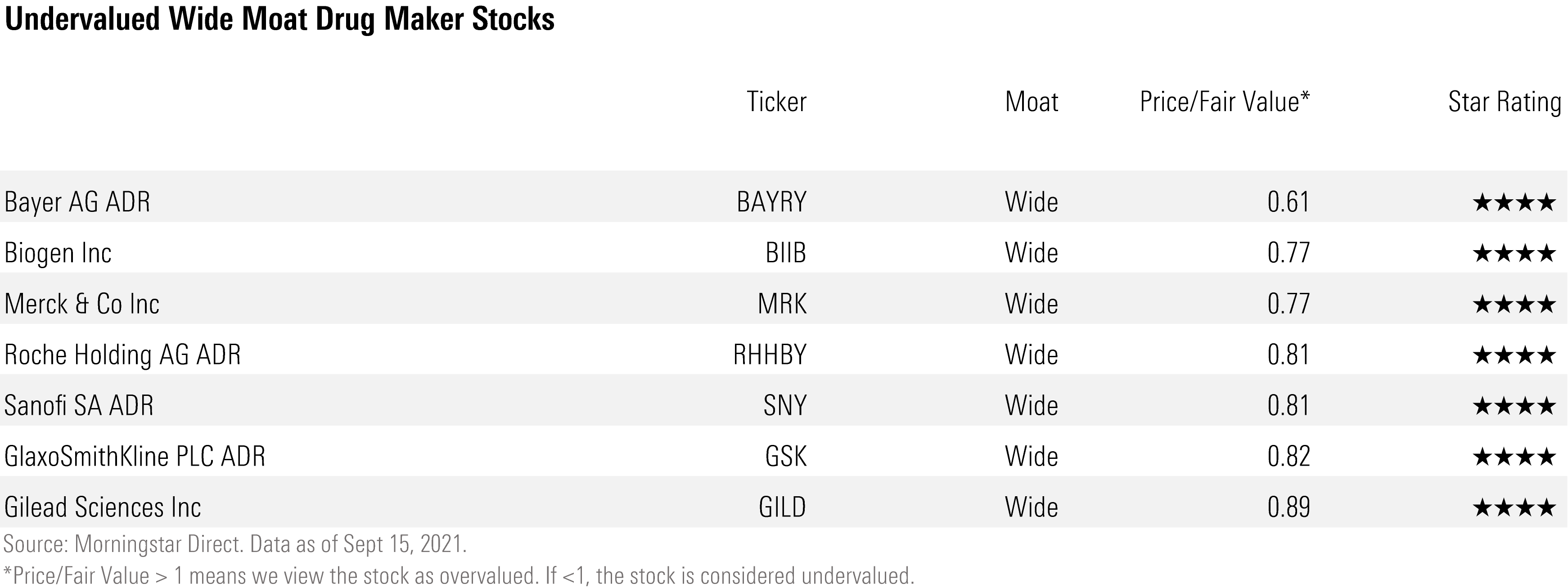

As a result, the recent decline in drug manufacturer stocks presents an opportunity for long-term investors. Below is a list of the most undervalued wide-moat drugmaker stocks in our coverage list.

Here’s what our analysts have to say about these businesses.

Bayer AG BAYRY

“Largely on the basis of the strong competitive advantages of the healthcare group and to a lesser extent the crop science business, we believe Bayer has created a wide economic moat. Also, the past divestiture of no-moat material science group Covestro leaves the company in a stronger competitive position.

"In the healthcare division, Bayer's strong lineup of recently launched drugs and solid exposure to biologics should support steady long-term growth. Bayer's hemophilia franchise and key ophthalmology drug Eylea are biologics. While competition is increasing in hemophilia and in eyecare, the manufacturing complexity of these drugs deters generics from entering the market. Further, strong demand for cardiovascular drug Xarelto should continue to drive growth.”

--Damien Conover, director

Biogen BIIB

“We think Biogen's specialty-market-focused drug portfolio and novel, neurology-focused pipeline create a wide economic moat. Biogen's strategy has its roots in the 2003 merger of Biogen (multiple sclerosis drug Avonex) and Idec (cancer drug Rituxan). While Rituxan is succumbing to biosimilar competition, Biogen is expanding its neurology portfolio beyond MS, with blockbuster neuromuscular disease drug Spinraza and future Alzheimer's disease blockbuster Aduhelm.

"Outside of MS, Biogen has strong human genetic validation for its neurology pipeline. Spinal muscular atrophy drug Spinraza (partnered with Ionis) is a $2 billion franchise, although competition from Novartis (gene therapy Zolgensma approved in May 2019) and Roche (oral drug Evrysdi) are beginning to erode U.S. Spinraza sales. Aduhelm has the largest potential; it was approved in the United States in June 2021 as the first disease-modifying Alzheimer's therapy. While there is significant uncertainty surrounding the potential commercial uptake of Aduhelm, we think the market also underestimates Biogen's remaining pipeline, which includes a continuing partnership with Ionis (including tau-targeting Alzheimer's drug BIIB094) and drug candidates to treat conditions including stroke, depression, Parkinson's, pain, and ALS.”

--Karen Andersen, strategist

Merck & Co MRK

“Merck's combination of a wide lineup of high-margin drugs and a pipeline of new drugs should ensure strong returns on invested capital over the long term. Further, following the divestment of the Organon business in June 2021, the remaining portfolio at Merck holds a higher percentage of drugs with strong patent protection. On the pipeline front, after several years of only moderate research and development productivity, Merck's drug development strategy is yielding important new drugs.

"Merck's new products have mitigated the generic competition, offsetting the recent major patent losses. In particular, Keytruda for cancer represents a key blockbuster with multi-billion-dollar potential: It holds a first-mover advantage in one of the largest cancer indications of non-small-cell lung cancer. Also, we expect new cancer drug combinations will further propel Merck's overall drug sales. However, we expect intense competition in the cancer market with several competitive drugs likely to report important clinical data over the next two years in earlier-stage cancer settings. Other headwinds include generic competition, notably to diabetes drug Januvia, likely to start as early as 2022.”

--Damien Conover, director

Roche Holding AG RHHBY

“Roche's drug portfolio and industry-leading diagnostics conspire to create sustainable competitive advantages. As the market leader in both biotech and diagnostics, this Swiss healthcare giant is in a unique position to guide global healthcare into a safer, more personalized, and more cost-effective endeavor. Strong information sharing continues between Genentech and Roche researchers, boosting research and development productivity and personalized medicine offerings that take advantage of Roche's diagnostic arm.

"Roche's biologics focus and innovative pipeline are key to the firm's ability to maintain its wide moat and continue to achieve growth as current blockbusters face competition. Blockbuster cancer biologics Avastin, Rituxan, and Herceptin accounted for 32% of Roche's revenue in 2019, and all three are seeing strong headwinds from biosimilars. However, Roche's biologics focus (more than 80% of pharmaceutical sales) provides some buffer against the traditional intense declines from small-molecule generic competition. In addition, with the launch of Perjeta in 2012 and Kadcyla in 2013, Roche has expanded its breast cancer franchise, and Phesgo, a subcutaneous coformulation of Herceptin and Perjeta, is launching in the U.S. Gazyva, approved in CLL and NHL and in testing in lupus, will also extend the longevity of the Rituxan franchise. Avastin's lung cancer sales are vulnerable to biosimilars and competition from new therapies Opdivo and Keytruda, but Roche's own immuno-oncology drug Tecentriq launched in 2016, and we see peak sales potential above $10 billion. Roche is also expanding outside of oncology with MS drug Ocrevus ($9 billion peak sales) and hemophilia drug Hemlibra ($6 billion peak sales).

"Roche's diagnostics business is also strong. With a 20% share of the global in vitro diagnostics market, Roche holds the number-one rank in this industry over competitors Siemens, Abbott, and Ortho. Pricing pressure has been intense in the diabetes-care market, but new instruments and immunoassays have buoyed the core professional diagnostics segment.”

--Karen Andersen, strategist

Sanofi SA SNY

“Sanofi's wide lineup of branded drugs and vaccines and robust pipeline create strong cash flows and a wide economic moat. Growth of existing products and new product launches should help offset weakening pricing in the insulin market.

"Sanofi's existing product line boasts several top-tier drugs, including immunology drug Dupixent. Dupixent looks well-positioned to reach peak sales over EUR 8 billion, with an initial focus on the moderate to severe atopic dermatitis market. We expect additional indications in areas such as the recently added severe asthma indication will help the drug serve additional patients. While Sanofi shares profits on the drug with Regeneron, the very high sales expected for it should provide a strong tailwind to overall growth for the company. Additionally, Sanofi holds a strong position with several vaccines and rare-disease drugs that should hold up well as pricing pressures and competition tend to be less severe in these areas.

"The company also harnesses its research and development group to bring new drugs to emerging markets. While pricing in emerging markets is not usually as strong as in developed markets, the company can still leverage its investment in developing new drugs for developed markets by bringing them to emerging markets. The rapid economic growth in emerging markets has created new geographic markets for Sanofi's drugs.

"A history of acquisitions and robust cash flow from operations means Sanofi could take advantage of further growth opportunities through external collaborations. We expect Sanofi's acquisition focus on rare-disease drugs will continue following several deals in this area, including Genzyme and more recently Bioverativ.”

--Damien Conover, director

GlaxoSmithKline PLC GSK

“As one of the largest pharmaceutical companies, GlaxoSmithKline has used its vast resources to create the next generation of healthcare treatments. The company's innovative new product lineup and expansive list of patent-protected drugs create a wide economic moat, in our opinion.

"The magnitude of Glaxo's reach is evidenced by a product portfolio that spans several therapeutic classes as well as vaccines and consumer goods. The diverse platform insulates the company from problems with any single product. One of the firm's highest revenue generators, Advair (for respiratory disease), represents just close to 5% of total revenue. The complexity in approving a generic version of an inhaled drug like Advair has held off significant U.S. generic competition well past the drug's 2010 patent expiration, but the early 2019 approval of a generic version of Advair will create headwinds for Glaxo. The company's advancement of its next-generation respiratory drugs should help Glaxo maintain its entrenchment in both asthma and chronic obstructive pulmonary disease as generic Advair competition intensifies.

"On the pipeline front, Glaxo has shifted from its historical strategy of targeting slight enhancements toward true innovation. Also, it is focusing more on oncology and immune system, with genetic data to help develop the next generation of drugs. The benefits of this strategies are showing up in Glaxo's early-stage drugs. We expect this focus will improve approval rates and pricing power.

"From a geographic standpoint, Glaxo is strategically branching out from developed markets into emerging markets. Its consumer and vaccine segments position the firm well in these price-sensitive markets. While this strategy is likely to create some challenges, like the potential legal violations that arose in early 2013 in China, we believe the fast-growing emerging markets will help support long-term growth and diversify cash flows beyond developed markets.”

--Damien Conover, director

Gilead Sciences GILD

“Gilead Sciences generates stellar profit margins with its HIV and HCV portfolio, which requires only a small salesforce and inexpensive manufacturing. We think its portfolio and pipeline support a wide moat, but Gilead needs HCV market stabilization, strong continued innovation in HIV, solid pipeline data, and smart future acquisitions to return to growth.

"Gilead is building a pipeline outside of HIV and HCV through acquisitions. The acquisition of Kite (CAR-T therapy Yescarta) has brought only slow sales growth, but the 2020 acquisitions of Forty Seven (CD47 antibody magrolimab) and Immunomedics (breast cancer drug Trodelvy) add to the oncology pipeline. Lead NASH program selonsertib failed in a phase 3 trial, but Gilead is exploring combination therapy with other mechanisms in NASH. Gilead's Veklury is also a leading treatment for SARS-CoV-2; it generated $2.8 billion in sales in 2020 and is poised for $2.7 billion in 2021.”

--Karen Andersen, strategist

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZM7IGM4RQNFBVBVUJJ55EKHZOU.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_d910b80e854840d1a85bd7c01c1e0aed_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/K36BSDXY2RAXNMH6G5XT7YIXMU.png)