Why the Rich Have Become Richer

Wage disparity is only half the story.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

This article was originally published on July 26, 2021.

Opposite Directions

Over the past half century, disparities in personal incomes have both fallen and risen. Between countries, the difference between the haves and have-nots has declined, thanks primarily to spectacular improvements in China and India. But within most advanced economies, the wealthy have become wealthier.

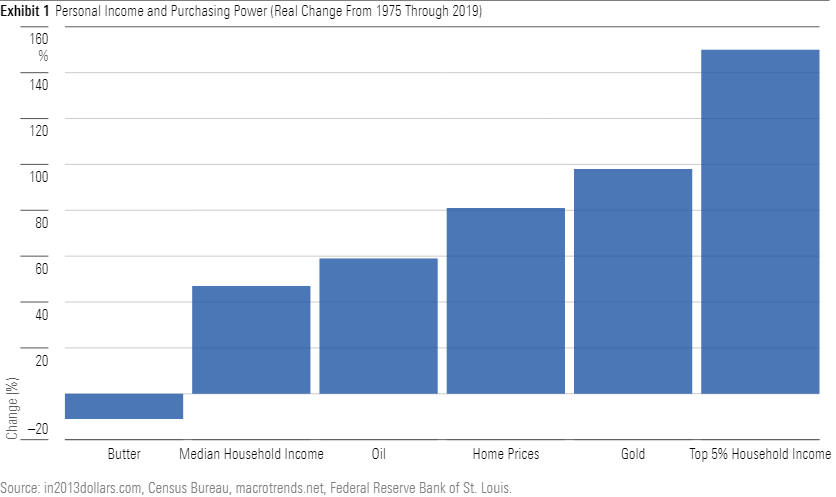

The latter is today’s topic. The following chart shows the growth in income after inflation for the median U.S. household from 1975 through 2019 (the period for which the Census Bureau’s data are available.) Also included is the change in median income for the highest-earning 5% of households, along with that of per capita gross domestic product and several goods. (All figures are expressed in real terms.)

Personal Income and Purchasing Power

These results should not surprise. That higher incomes within the United States have outgrown median wages has been widely discussed, as has the struggle of ordinary workers to outdo inflation. Some items have become relatively cheaper, such as basic foodstuffs and airline flights. And, of course, modern technology permits services that previously did not exist. However, many common goods, including oil, houses, and gold, have become costlier for average Americans.

This outcome has been caused by shifts in both earned and unearned income. With earned income, elite employees have expanded their negotiating power. Spiraling CEO compensation and the hefty salaries earned by tech workers—in 2018, the median wage at Alphabet GOOG was almost $250,000—have grabbed the headlines. But college graduates overall have fared well over the past several decades. In contrast, employees who lack college degrees have increasingly been regarded as replaceable. Their wages have languished along with their standing.

Corporate Successes

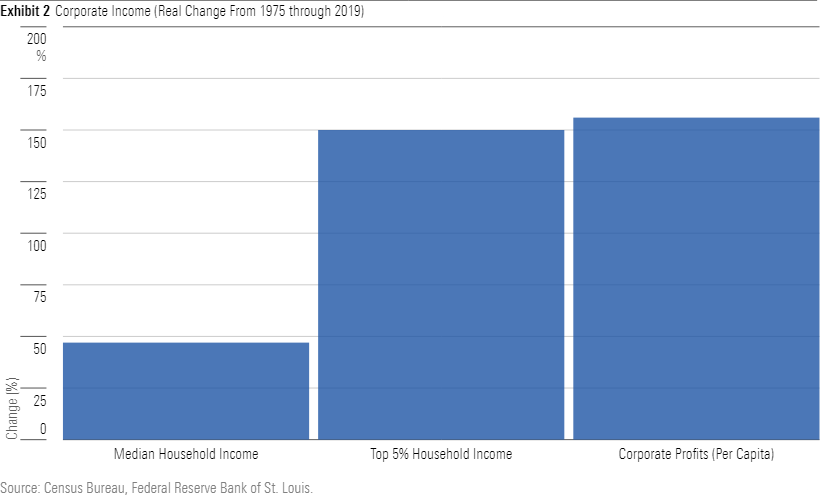

The role of unearned income has been less discussed, but it is equally relevant. In recent decades, U.S. companies have grown their profits faster than households have increased their incomes. This result has lifted the prices of stocks, which are mostly owned by the higher-income households. For the well-positioned, the economic circle has been splendidly virtuous.

The next chart depicts the growth in aftertax corporate profits.

Corporate Income (Real Change From 1975 Through 2019)

Although suggestive, this illustration alone does not indicate that stock market shareholders prospered, as this measure of corporate profits, calculated by the Bureau of Economic Analysis, includes both private and publicly traded firms. It could be that privately held businesses thrived while listed companies struggled. Or perhaps public corporations profited handsomely, but for whatever reasons, equity investors refused to pay higher share prices for those greater earnings.

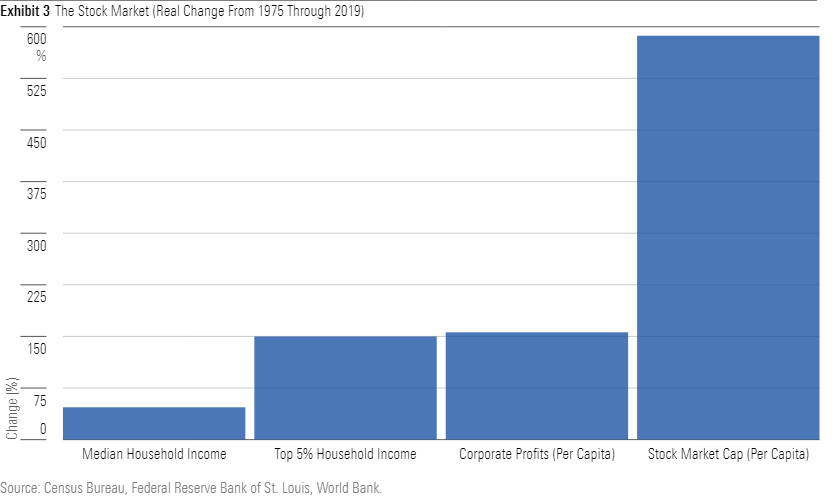

However, neither event occurred. Over that 44-year stretch, the capitalization of the U.S. stock market—that is, the cost of buying every listed share—increased dramatically. Even after adjusting for inflation, and for the nation’s increase in population by computing the statistic on a per capita basis, the amount of dollars invested in listed U.S. equities ballooned by nearly 600%.

The Stock Market (Real Change From 1975 Through 2019)

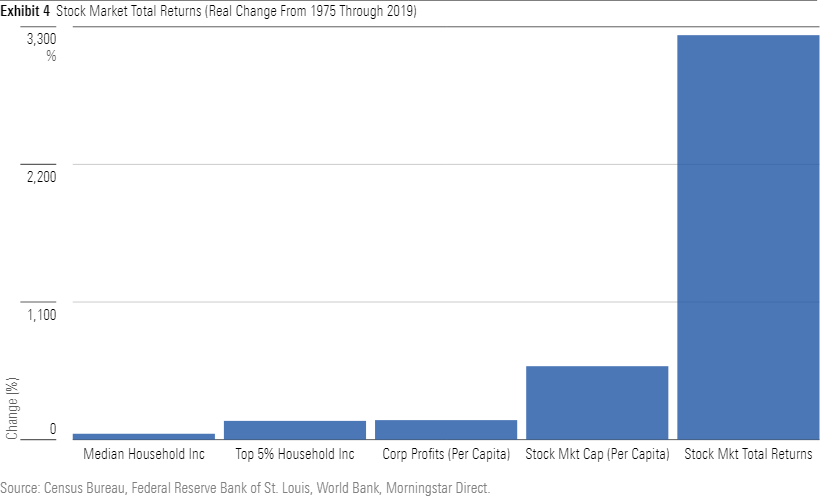

This figure, too, requires further investigation. If a huge number of privately held firms went public, or publicly traded companies issued a barrage of new shares, then the capitalization of the stock market could soar without enriching shareholders. The pie would enlarge, but the slices would not. Happily for equity shareholders, that has not been the case. Since 1975, the S&P 500′s returns after inflation have been enormous.

Stock Market Total Returns (Real Change From 1975 Through 2019)

Dividends Matter

The explanation for this performance is straightforward. First, although many firms have entered the public markets, the dilution caused by their activities has been counterbalanced by the trillions of dollars that companies have spent on share repurchases. These days, the amount of money spent on stock buybacks typically exceeds that used for dividend payouts. Second, and of even greater importance, the total-return calculation includes those dividends. They represent additional receipts that are not captured by price-only measurements.

The boon of dividend payments makes stocks different from the other elements featured in today’s charts. Butter, gold, and oil distribute no cash. For its part, household income consists almost entirely of cash—but the Census Bureau’s measure conceals no further benefits. The only item on the previous charts that can be compared with equity investment is homeownership, which also can generate greater gains than the initial numbers suggest (because house purchases are typically leveraged).

In short:

- High wage earners have never fared better. They are likelier than ever before to have more money than they require for their everyday expenditures.

- Increasingly, their monies are likely to find their way into equities, because of the ubiquity of 401(k) plans and the growth in registered funds.

- High wage earners have received a double boost. Not only have their salaries tended to improve faster than their lower-paid peers, but their stock portfolios have performed better yet.

Two Sources of Income

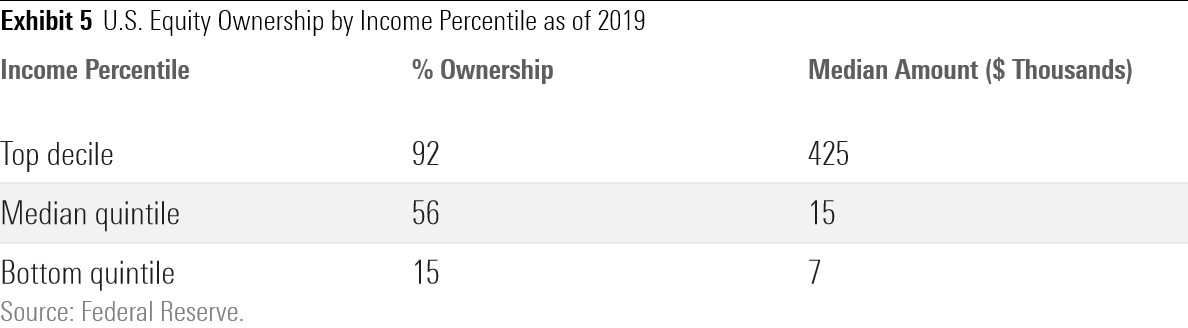

The table below supports the final claim. It shows the percentage of equity ownership (either by holding individual stocks directly or by owning stocks indirectly through funds) for those in the top income decile, the middle income quintile, and the bottom income quintile. It also shows the median dollar amount of equities, for those who did own such securities.

U.S. Equity Ownership by Income Percentile as of 2019

The differences were pronounced in 2021. With stocks up 15% (somewhat more for most U.S. equities, somewhat less for foreign securities), the median high-income household has enjoyed about $60,000 in equity appreciation, in addition to its earned income. Meanwhile, other households have gained only negligible amounts from their much smaller equity positions.

Of course, the stock market isn’t usually as ebullient as in 2021. Nevertheless, over the long term, stock returns should continue to exceed that of income growth, because equity performances include the effects of both 1) profit increases and 2) dividend payouts. Stocks have a higher expected rate of return than do wages, and the wealthy own a great deal more stocks. In effect, they possess a second source of income that others lack.

Postscript: Despite the stock market’s recent troubles, equities have outstripped wage growth since the ending date for this column’s calculations, December 2019. Barring catastrophic stock market losses, the argument remains very much intact.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)