Liquid Alternatives Funds: Is There Any Hope?

Considering the future of a fund-industry flop.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Square One

Let’s define terms. “Liquid alternatives” funds are publicly available investments, typically mutual funds and exchange-traded funds. They are “liquid” because they may be traded more frequently than their forebearers, hedge funds, and they are “alternative” because they invest atypically, acting like neither stocks nor bonds.

These are the seven liquid alternatives Morningstar Categories:

- Equity Market Neutral

- Event Driven

- Macro Trading

- Multistrategy

- Options Trading

- Relative Value Arbitrage

- Systematic Trend

Almost all liquid alternatives funds are new, created after the 2008 global financial crisis. They were, quite literally, an afterthought--a reaction to the stock market’s tumble. The pitch: These funds would protect everyday investors’ portfolios, just as hedge funds did for institutions and wealthy individuals.

Protect they did--from investment profits. During the 2010s, liquid alternatives funds averaged an annualized gain of 1.66%, which placed them behind every fund category save for a few specialty groups, such as energy, precious metals, and Latin American stock funds, and three flavors of short-term bond funds. The results weren’t disastrous, but neither did they justify such funds’ existence.

The market environment provides no excuse. True, the stock-market boom hurt the relative performance for liquid alternatives. But relative returns are not the issue. That a hedge lagged during a bull market is both understandable and acceptable. The concern lies when the hedged investment trails high-quality bonds, as has been the case with liquid alternatives funds. In that case, why bother with trickery? You could just hold Treasuries instead.

The Performance Problem

Liquid alternative funds can't ride investment tailwinds. To use the vernacular, stocks and bonds have betas. (Textbooks define beta as an investment statistic, but in practice investment professionals generally use the word to mean "something that possesses expected returns.") Buy a basket of stocks, and over time you should make money; ditto for bonds. Profiting from betas requires no investment skill.

In contrast, liquid alternatives funds require insight. Take equity market-neutral funds. For each long stock, a market-neutral fund holds a corresponding short position. The betas cancel each other out. The fund’s expected return is therefore 1) the interest collected from the portfolio’s cash 2) minus expenses. If the market-neutral fund is to exceed this distressingly low hurdle, it must either cheat with its hedges, or its portfolio manager must make more good decisions than bad.

The same principle applies to other liquid alternatives categories. Event-driven and relative value/arbitrage funds buy and sell stocks, while macro trading, options trading, and systematic trend funds buy other asset classes. Either way, as with market-neutral funds, such funds play a zero-sum game. They can’t succeed unless other investors lose. That is, they thrive only if their managers outdo the averages.

From the Report

A recent Morningstar publication, "2021 Global Liquid Alternatives Landscape," by Erol Alitovski, Matias Mottola, Francesco Paganelli, and Simon Scott, highlights several other difficulties. (If you click on the link, don't be dismayed. Once you answer those few questions, the paper will immediately be sent.)

1) Lineup churn. If fund companies aren't serious about liquid alternatives funds, then investors probably won't be, either. And fund companies have not been serious. Of the 453 liquid alternatives funds that have been launched since 2009, only 153 exist today. That makes for a 34% survival rate over 12.5 years. Liquid alternatives are the fund industry's mayflies.

2) Complexity. The instability comes from both directions. One reason fund companies have shuttered so many liquid alternatives funds is because their investors have been fickle. Liquid alternatives are hard to own. The elaborateness of their strategies makes them unpredictable, which tends to upset shareholders. Losing money is one thing, but losing money unexpectedly, without knowing why, is quite another.

3) Constraints. Liquid alternatives funds have been marketed as hedge funds for the masses. That promise has backfired, twice. First, hedge funds have disappointed since liquid alternatives were launched, with the 2010s described as that industry's "lost decade." Second, there is a catch to offering that extra liquidity. Some hedge fund investment strategies cannot be used by their publicly traded cousins. Liquid alternatives funds emulate hedge funds, but they are not perfect matches.

4) Fees. Fortunately, liquid alternatives funds usually cost considerably less than hedge funds. That is a benefit. However, they are costly by mutual fund standards, carrying a median expense ratio of 1.66%. Yes, the same figure as their net annualized return. For each dollar that shareholders have earned, the fund company collects a dollar for itself. A 50/50 split. What could be fairer?

Looking Forward

None of this sounds encouraging. Nor should it. Implicitly, liquid alternatives funds contradict passive investing. Indexers maintain that shareholders should avoid the temptation of chasing manager "alphas," opting instead to buy dirt-cheap betas. Without putting the matter quite so directly, liquid alternatives funds argue the opposite. Pay more, forgo beta, and pocket those manager alphas.

History has very firmly supported the indexers’ side of that argument.

Nevertheless, there are three current reasons for considering liquid alternatives funds, despite their drawbacks:

1) The need for an equity hedge has increased. Better to protect against a stock-market decline when equity valuations are at record levels than when prices are relatively modest. When liquid alternatives funds came to the marketplace, hedges weren't much needed. Today, they are. Of course, as previously mentioned, that doesn't mean that liquid alternatives funds are the correct hedge. But at least their function is required.

2) The competition has softened. Ten-year Treasuries yielded 2.5% in January 2009, 3% five years later, and 1.3% today. Cash, of course, pays just about nothing. Admittedly, choosing a liquid alternatives fund over such assets brings additional risk, but it is also likely, over a full market cycle, to bring at least somewhat higher returns.

3) The funds have longer track records now. Forecasting future winners is a perilous endeavor. Nevertheless, the task does become easier after the evidence accumulates, which is now the case for liquid alternatives funds. A decade ago, very few liquid alternatives funds possessed five-year track records. Now, 46 funds have 10-year records. It's not a huge number, but enough to justify some tentative conclusions.

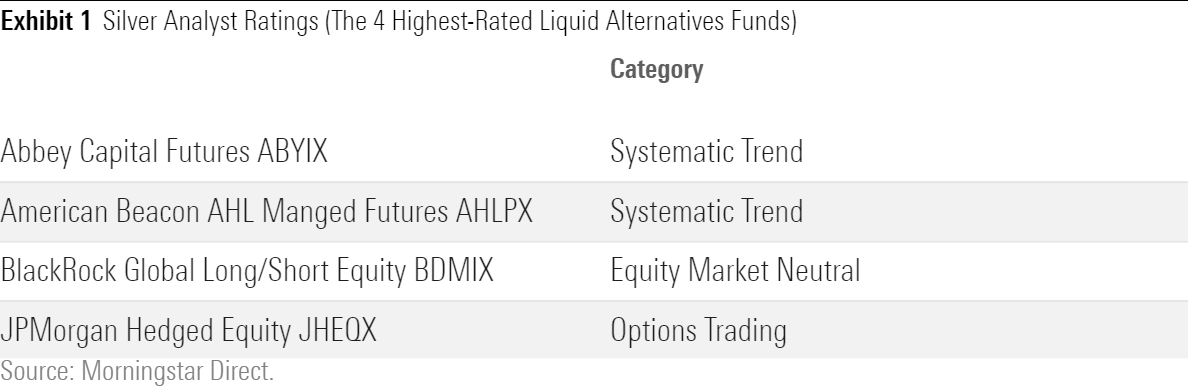

In that spirit, I conclude this column with the 4 liquid alternatives funds that carry Morningstar’s second-highest Analyst Rating of Silver. (No liquid alternatives funds are rated Gold.) Personally, I prefer the simplicity of cash/bonds, but selecting one or more of these funds would also make for a sensible hedge.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HTLB322SBJCLTLWYSDCTESUQZI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TAIQTNFTKRDL7JUP4N4CX7SDKI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)