Investing During an Era of Speculation

Should we be concerned about the financial markets' excesses?

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

The Winning Mindset

Four faculty members from Hong Kong and Taiwan universities have published a paper, "Do You Feel Lucky? Lottery Jackpot Winnings and Retail Trading Around Neighborhoods." (When Clint Eastwood is long gone, and his films watched as seldom as "The Robe," that line will persist.) The article's thesis: Those who trade through brokerage branches located near stores that have recently sold jackpot-winning lottery tickets are likelier to invest more aggressively.

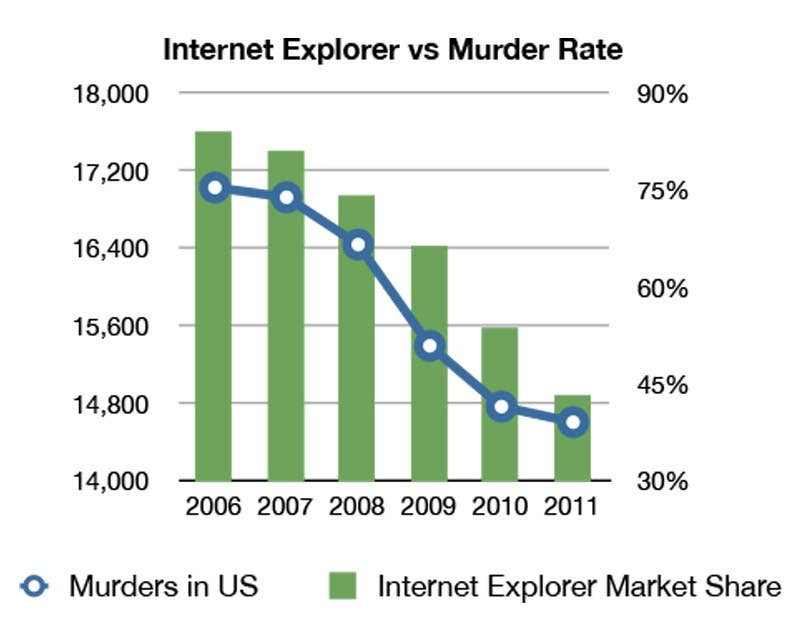

Yes, I know, it sounds like a stretch. It may be. Despite the apparent evidence, using Internet Explorer did not increase the U.S. murder rate. Nor do Nicolas Cage films cause pool accidents. Similarly, the authors' result does not necessarily indicate that Taiwanese investors--the subject of their study--change their behavior because a local buyer hit the lottery jackpot. Sometimes, correlations just happen, even when the findings are deemed to be statistically significant.

However, regardless of the accuracy of the paper's specific claim, its broader point is certainly correct. Success emboldens. This holds true not only for investors, but across a wide variety of endeavors. After a string of positive results, banks frequently loosen their lending standards, divers seek higher rocks, and gamblers double their antes. Fortune favors the brave. Strike when the iron is hot. Make hay while the sun shines. Carpe diem.

More Than Luck

Feeling fortunate is only a part of it. Those who have prospered are likely to conclude that they are smarter than the rest, because they can perceive what others cannot. Consequently, investors who profited from buying Tesla TSLA or Bitcoin tend to believe that their achievements are repeatable. What they once foresaw they can foresee again. (I have been no exception to the rule, although my audacity took the opposite path, in thinking that I could predict a bear market.)

When the going is truly good, the twin effects of luck and confidence are joined by the wealth effect--that is, the real ability to assume more risk. The first two attributes are psychological; they describe the investor's mindset but not the ability to sustain portfolio losses. But the wealth effect is tangible. Having more money means having greater protection against adverse outcomes. Unsuccessful trades become annoyances, not disasters.

(Early in my Morningstar career, while working as a mutual fund analyst, I learned firsthand about the wealth effect. I received a phone call from Sen. Alan Cranston, who asked about several emerging growth funds. I responded that a couple of them struck my fancy, but that such funds were highly volatile, and the senator should understand their dangers before purchasing them. His response: "I am at the point in my life where I can afford to take investment risk.")

Speculative Elements

Such is the current condition in the United States. Luck, confidence, and wealth have created an age of speculation. Signs of economic aggression are everywhere. Stocks are soaring, thanks in part to record trading volume from retail investors. In addition, alternative investments are thriving. Cryptocurrencies, special-purpose acquisition companies, and nonfungible tokens have all sprung from dragons' teeth, although only the former marketplace yet rates as truly large.

The desire to spend--and the ability to absorb losses--is abundantly evident outside of the investment markets. House prices have risen so sharply as to inspire a bevy of articles wondering about the possibility of a real estate crash. Forbes predicts that revenue derived from U.S. sports betting will grow sixfold within three years. And an offhand doodle made by Nirvana singer-songwriter Kurt Cobain recently sold for $281,000.

The Good News

All this said, it would be inaccurate to imply that today's Americans are imprudent. If anything, the facts suggest the opposite. The ratio of household debt payments to disposal income--that is, the percentage of income that Americans must devote to debt service--is at its lowest since the Federal Reserve Bank of St. Louis began tracking that measure 40 years ago. Similarly, the ratio of household debt to gross domestic product is below the norm. For the most part, investors are speculating with assets that they can afford to do without.

This assertion is supported by the mutual fund data. Ark Innovation ARKK, Ethereum, and snowbird condos might attract house money, but the basic needs for retirement typically are covered by old-fashioned mutual funds (in addition to Social Security and/or pension receipts). And those funds are being invested quite carefully. During the first five months of 2021, U.S. mutual fund investors redeemed a net $45 billion of equity fund shares while reallocating $260 billion into bond funds.

In short, there is something of a method to the madness. The $24 trillion held by U.S. mutual funds (more than double the amount of China's entire stock market capitalization) is, by and large, invested soberly. In addition, despite offering piddling interest rates, U.S. banks currently possess record deposits of $22 trillion, up 25% over the past five years. That makes for a massive ballast of conservative investments--about $350,000 for every full-time American worker.

(Of course, everyday Americans don't hold every mutual fund share, nor every bank deposit. But, if anything, those figures understate the amount of conventional assets that they possess, since they don't include the assets from institutional pension funds that invest on their behalf.)

Looking Forward

My take:

1) Some investments undoubtedly are frothy. Morningstar calculates that the average stock in ARK Innovation's portfolio trades at 106 times its trailing 12-month earnings. That is pricey by any standard.

2) However, given the relatively modest level of consumer debt, shareholders should be able to withstand reasonably large investment losses.

3) They also are protected by the $46 trillion that they hold in mutual fund shares and bank deposits.

In summary, if the general economy remains solid--all bets are off during recessions--everyday investors should be relatively immune to a sell-off in speculative investments, should that event occur. I do not believe that such damage would spread.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/54RIEB5NTVG73FNGCTH6TGQMWU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}