10 Promising Stocks to Consider

These companies are growing their competitive advantages--and their stocks are undervalued.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Sometimes, it's easy to spot potential. Take, for instance, Michael Jordan. It was obvious from the get-go that Jordan’s NBA career held great promise--though maybe none of us realized just how very great that promise was.

Other times, though, future ability isn't as obvious. During his first NBA season in Utah, John Stockton played fewer than 20 minutes per game--and his 0.471 field-goal shooting percentage was the lowest of his Hall-of-Fame career. That didn’t look nearly as promising.

The same holds true when it comes to finding promising stocks. For some companies, their competitive advantages are apparent, and their paths to growth and increasing profitability are seemingly clear-cut. Other firms, meanwhile, may be experiencing improving competitive advantages that aren't as noticeable.

Our moat trend ratings get at that idea--how a company's competitive advantages are changing. Companies with positive moat trends have competitive advantages that are strengthening; those with negative moat trends face weakening competitive advantages. And those with stable moat trends are maintaining whatever competitive advantages they have.

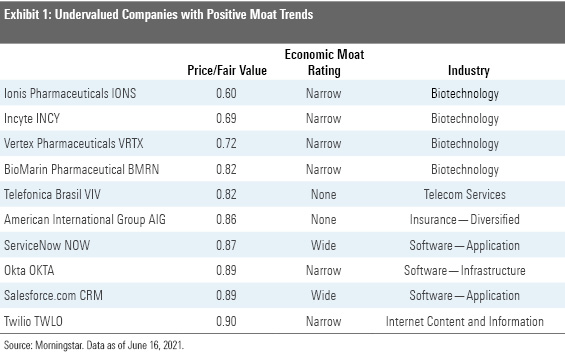

Today we’re looking for promising stocks on the cheap. Specifically, we screened for the 10 stocks in our coverage universe with the lowest price/fair values and positive moat trends. We tossed out companies with poor stewardship ratings. Why? Managers who have a record of poor capital-allocation decisions may not have the wherewithal to establish or deepen their companies’ competitive advantages, no matter the trend.

Here’s a closer look at three stocks from the list.

Ionis Pharmaceuticals IONS

"Ionis is a leader in RNA-based therapies, and its spinal muscular atrophy drug Spinraza, marketed by partner Biogen BIIB, is the first RNA-based therapy to achieve blockbuster status. The firm's antisense oligonucleotide, or ASO, technology faces strong competition from RNA interference technology emerging from Alnylam ALNY, Arrowhead ARWR, and Dicerna DRNA, as well as gene editing and gene therapy pipelines at multiple firms. However, Ionis has built a massive pipeline of promising new drugs that are rapidly moving toward the market, securing a narrow moat.

Ionis' therapies alter production of a given protein in the body, typically reducing production of a toxic, mutant version. Therefore, Ionis can tackle diseases that are difficult to treat effectively with other methods, as its therapies are targeted (avoiding safety issues with off-target effects of small-molecule drugs), can act inside the cell (unlike antibody therapies), and are reversible (unlike gene therapy). Ionis has a broad pipeline and strong collaboration partners to help usher to market drugs for large indications, requiring large clinical trials and salesforces. Ionis spun out cardiovascular-focused Akcea in 2017 but reacquired full ownership again in 2020, given the advancement and increasing attractiveness of Akcea's late-stage cardiology pipeline.

Waylivra and Tegsedi, both approved for rare metabolic disorders and wholly owned by Ionis, have yet to generate significant revenue, due to significant side effects for both and direct competition for Tegsedi from Alnylam's Onpattro. While we are skeptical that these two products will ramp strongly, next-generation ASOs TTR-LRx and APOCIII-LRx require much smaller doses and are easier to administer, and we think they have improved prospects. Beyond these programs, several other drug candidates could continue to validate Ionis' pipeline potential. Ionis has several wholly owned neurology and rare-disease programs poised to generate early data through 2021. Partnered programs in neurology (with Roche RHHBY and Biogen) and cardiology (with Novartis NVS and Pfizer PFE) are in late-stage development, putting Ionis in a position to see new royalty streams by the mid-2020s." Karen Andersen, strategist

American International Group AIG

"The years since the financial crisis have shown that American International Group would have destroyed substantial value even if it had never written a single credit default swap, had noncore businesses it needed to shed, and had material issues in its core operations that it needed to fix. We've been encouraged, however, by the recent progress in terms of improving underwriting margins, and the plan to take out $1 billion in costs by 2022 would be another material step. But over the past year, the impact of the coronavirus has obscured the company's progress.

COVID-19 losses to date have been very manageable. Looking at loss estimates and current industry capital suggest, as a percentage of capital, losses are likely to stay well within the range of historical events that the industry has successfully absorbed in the past. In our view, the major risk that still remains is legal rulings on business interruption claims. While we believe rulings to date have largely been in the industry's favor, we don't think insurers are completely out of the woods, and legal outcomes are difficult to predict.

If coronavirus losses are manageable, the longer-term picture looks relatively bright. The pricing environment has not been particularly favorable in recent years. However, in 2019, pricing momentum picked up in primary lines, and commentary from carriers suggests this positive trend has only accelerated in 2020. The coronavirus could be an additional spur to pricing. While this is not our base assumption, we see potential for a truly hard pricing market, similar to the period that followed 9/11.

We think AIG has made material progress in improving its under/over the past couple of years, and has set a target for an underlying combined ratio below 90% by the end of 2022. Assuming an average level of catastrophe losses, we think this is a level that would allow P&C operations to achieve an acceptable level of return, and a harder pricing market may make hitting this target easier." Brett Horn, senior analyst

Salesforce.com CRM

"We believe Salesforce.com represents one of best long-term growth stories in software. Even as revenue growth is likely to dip below 20% for the first time at some point in the next several years, we believe ongoing margin expansion should continue to compound earnings growth of more than 20% annually for much longer.

After introducing the software-as-a-service model to the world, Salesforce.com has assembled a front-office empire that it can build on for years to come, in our view. Sales Cloud represents the original salesforce automation product, which streamlined process management for sales leads and opportunities, contact and account data, process tracking, approvals, and territory tracking. Salesforce.com’s critical differentiator was that the software was accessed through a web browser and delivered over the Internet, thus inventing the SaaS software delivery model. Service Cloud brought in customer service applications, and Marketing Cloud delivers marketing automation solutions. These solutions encompass nearly all aspects of customer acquisition and retention and, in our view, are mission critical. Salesforce Platform also offers customers a platform-as-a-service solution, complete with the AppExchange, as a way to rapidly create and distribute apps. We believe this further strengthens the substantial community of Salesforce users.

In our view, Salesforce will benefit further from natural cross-selling among its clouds, upselling more robust features within product lines, pricing actions, international growth, and continued acquisitions such as the recent Tableau deal and the pending Slack deal. Salesforce is widely considered a leader in each of its served markets, which is attractive on its own, but the tight integration among the solutions and the natural fit they have with one another makes for a powerful value proposition, in our view. To that end, more than half of enterprise customers use multiple clouds. Further, customer retention has gradually improved over time and is better than 90%, which we expect to grind higher still in the coming years." Dan Romanoff, analyst

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/2UWGQD7LCJCYNF3WQ5HHLP7UBE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WC6XJYN7KNGWJIOWVJWDVLDZPY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HHSXAQ5U2RBI5FNOQTRU44ENHM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)