What Are TIPS, and How Do They Help Protect Against Inflation?

A quick look at the benefits and risks of Treasury Inflation-Protected Securities, and the best way to invest in them.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

Like traditional Treasury bonds, Treasury Inflation-Protected Securities are backed by the full faith and credit of the U.S. government (meaning there is no credit risk involved). But, as their name implies, TIPS also offer inflation protection.

Why Invest in Treasury Securities?

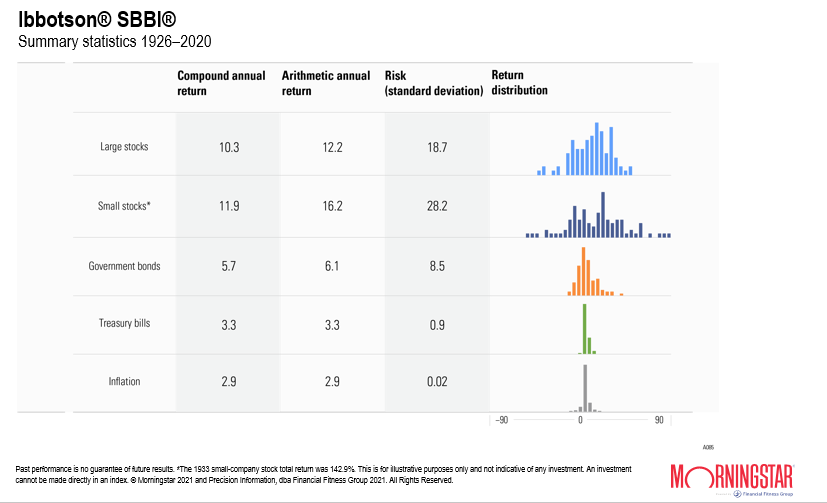

Treasuries (and other very high-quality bonds) offer diversification benefits for stock-heavy portfolios. As you can see from the image below, stocks (as an asset class) have far greater return potential over the long term than high-quality bonds do, but stocks are prone to more dramatic price swings in the short term. You can see this from their higher standard deviation and return distribution, which measures how variable an asset's price is. A larger standard deviation means bigger price swings.

Investors who are many years away from retirement have time to ride out stock market downturns, but they don't always feel great while they're happening. Keeping a small portion of your portfolio in Treasuries can offset some of the stock price volatility in your portfolio because Treasuries tend to hold up well when stock markets are selling off.

Source: Morningstar Presentations, available in Morningstar Office.

Watch Out for Inflation

One of the biggest risks of investing in Treasury bonds is that the fixed yields they pay will not be able to keep up with the rate of inflation.

Over the past 94 years, inflation has averaged 2.9% per year. Morningstar's outlook for core inflation is 2.5% for 2021, falling to 2.3% for 2022-25. This is in line with the break-even inflation rate, which is a market-based measure of expected inflation.

The break-even inflation rate is calculated like this: The 10-year Treasury yield minus the 10-year TIPS yield equals the 10-year break-even rate. Let's plug in real numbers (as of June 23, 2021, from www.Treasury.gov): 1.50% (10-year Treasury yield) minus -0.84 (10-year TIPS yield) equals 2.34% (10-year break-even rate).

Yes, you read that TIPS yield correctly. When Treasury bonds are trading below the expected inflation rate, as is the case today, TIPS yields fall into negative territory. Some investors are willing to accept that negative yield if they think inflation is enough of a concern because TIPS' principal value adjusts upward with inflation.

How Do TIPS Work?

Unlike traditional bonds, TIPS' principal value will change, upward or downward, to keep pace with inflation as measured by the Consumer Price Index for All Urban Consumers (with a lag of a few months). The coupon payments, which are paid twice per year, will also vary because although the coupon rate is fixed, the inflation-adjusted principal amount is changing.

If an investor holds a TIPS to maturity, the owner receives the adjusted principal or the original principal, whichever is greater. This provision protects the bond owner against deflation.

This protection has a cost. TIPS yield less than Treasuries of similar maturity, because TIPS holders receive that inflation adjustment that compensates for their lower yields. And because Treasury yields are currently low owing to the current low-interest-rate environment, TIPS' yields have gone so low they've actually been negative for most of 2021.

TIPS Can Be Volatile

Investors may be surprised to learn that TIPS' prices can be volatile, for a variety of reasons.

For one, although the principal values of TIPS are designed to appreciate with increases in inflation, inflation-protected bond funds are not impervious to changes in market yields, as floating-rate bonds are designed to be. When yields rise, TIPS' prices come under pressure--the longer the bond, the more pressure--even if inflation is pushing up their principal value at the same time.

In addition, while they're still Treasury bonds, TIPS tend to be less liquid than traditional Treasuries; this was really on display during the financial crisis.

"The inflation protection is really a long-term feature that works properly if you hold a TIPS until maturity. You should pretty much expect that changing market yields will drive TIPS market prices all over the map in the meantime, though," says Morningstar senior analyst Eric Jacobson.

What's the Best Way to Buy TIPS?

Buying individual TIPS is the most direct way to protect against inflation. If they are purchased directly from the Treasury when they are issued and held until maturity, they will provide a positive real return.

But the biggest drawback of owning individual TIPS over a professionally managed TIPS fund or exchange-traded fund is capital appreciation potential, explains Morningstar analyst Neal Kosciulek. A TIPS fund can take advantage of rising yields by swapping out the bonds in the portfolio for higher-yielding ones.

However, because TIPS funds can buy and sell TIPS any time--they don't necessarily need to buy them when they're issued and hold them until maturity--they don't necessarily move in lock step with inflation.

If any degree of unexpected inflation could cause serious harm, or if you have very specific cash flow needs, individual TIPS might be a better choice for you. But, Kosciulek says, low-cost TIPS index funds are probably suitable for most investors concerned about unexpected inflation over the long term. The trade-off for losing the fixed real yield is a potential uptick in total return.

See this article for a list of TIPS funds earning Morningstar Medalist ratings.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/XLSY65MOPVF3FIKU6E2FHF4GXE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)