Which Stocks Benefit From Biden's Infrastructure Plan?

The proposed plan could be passed this summer, but related stock valuations remain uncertain.

/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)

At a current price tag of over $2 trillion, the American Jobs Plan would provide a boost to a wide range of sectors and companies, reinvigorating traditional U.S. infrastructure as well as supporting new nontraditional infrastructure programs. However, this is not a free lunch for the U.S. equity market, as the proposed increases in the corporate and global intangible low-taxed income tax rates to pay for the plan will be a headwind.

We expect that this plan will be enacted as soon as this summer and, for the most part, be of similar size to the version that's currently on the table. While the scope of the plan is large and wide-ranging, we do not expect that it will affect our long-term projections for economic growth in the United States.

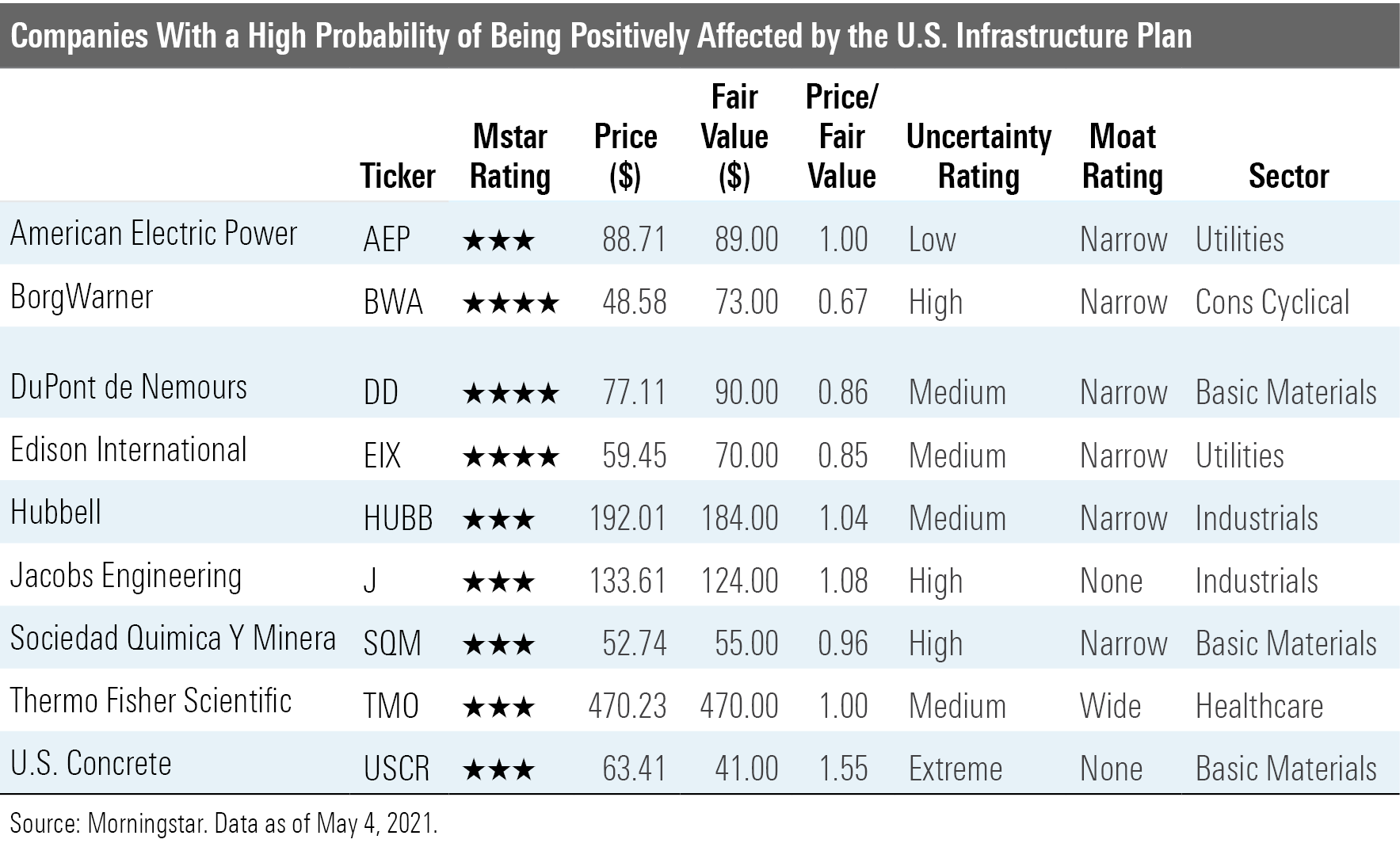

With the U.S. market near its highs--and slightly overvalued, in our view--many of the companies that might be able to capitalize on the infrastructure plan are either already fairly valued or overvalued. For example, stock prices for the obvious traditional infrastructure candidates have already run higher. We think that the most opportunity for currently undervalued 4-star stocks can be found in sectors that are not traditionally considered infrastructure plays.

In addition, investors may look to invest in a basket of 3-star stocks that have a high probability of being positively affected by the infrastructure plan. Since those stocks are currently fairly valued, it helps to limit downside risk if the final infrastructure plan does not play out as expected but may provide additional upside potential if the infrastructure plan comes to fruition.

Infrastructure Plan Shouldn't Impact Our Long-Term Economic Forecast

Total spending outlined in the Biden administration's American Jobs Plan equates to over $2 trillion in new federal government spending over a 10-year period on a wide range of programs. While we expect that the spending will be weighted toward the earlier years, on average the extra $200 billion-plus in annual spending is about 6% more than the federal government's annual spending before the pandemic and equates to about 1% of annual gross domestic product.

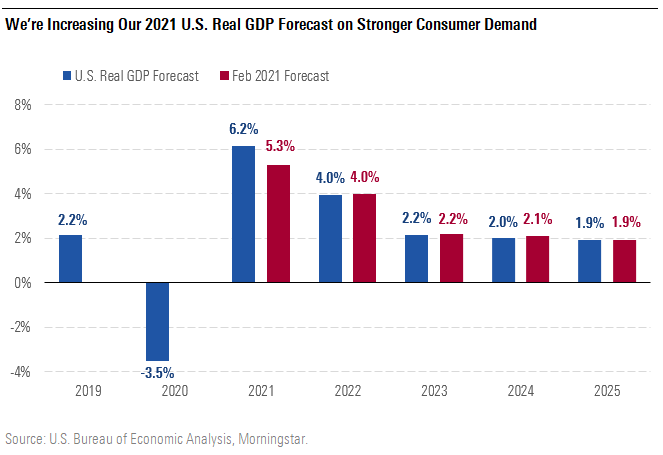

From a macroeconomic point of view, we do not expect that the infrastructure plan will lead us to revise our current economic forecasts for U.S. GDP. Like any form of fiscal stimulus, added infrastructure spending can help to bolster economic growth when the economy is operating lower than its total potential economic output. However, in our forecast, we think there's a good chance that the economy will be running near that potential by the end of 2022 and that there will be limited amounts of economic slack at that point.

In fact, as shown below, we recently boosted the GDP forecast that we made in February based on a faster-than-expected U.S. consumer recovery in the first quarter. We expect U.S. real GDP to jump 6.2% in 2021 and 4.0% in 2022, soaring past our pre-COVID-19 expectation. By the end of 2022, we expect labor markets to become very tight, with unemployment reaching 3.5%, below the prepandemic (fourth-quarter 2019) level of 3.6%. While the exact level of potential GDP is fundamentally unknowable, it's very unlikely that it would be so high that the output gap isn't closed by 2024.

Which Parts of the Proposal Will Be in the Final Infrastructure Plan?

We expect this framework will be the opening salvo in a multimonth negotiation. Depending on the negotiations between Democrats and Republicans, the infrastructure legislation could be enacted as soon as July. Although we think that is an aggressive time frame, we also think there is enough momentum to make it possible.

We expect that Democrats will prefer to have at least a few Republicans on board in order to assert that the spending package and associated tax increases are bipartisan. As such, the negotiations will allow Republicans to push back on several items within this framework as well as attach a few of their own priorities.

The central controversy right now is related to the definition of infrastructure, as the current plan includes what we consider to be traditional as well as nontraditional infrastructure spending.

- Traditional infrastructure consists of roads, transportation, and other shared public facilities.

- Nontraditional infrastructure includes expanding home- or community-based care for the elderly and people with disabilities, producing and retrofitting over 2 million affordable and sustainable places to live, and supporting green and sustainable initiatives. These are projects and programs that have not traditionally been funded by the federal government or have not historically been considered infrastructure.

The traditional infrastructure spending aspects will likely have broad support and should not have much difficulty being enacted. However, several nontraditional infrastructure spending proposals may see significant resistance from Republicans (and possibly some of the more centrist Democrats), who view that type of spending as being beyond the scope of the federal government.

At the end of the day, we fully expect that an infrastructure program will be pushed through, even if no Republicans vote for it. The largest question mark is the size and the scope of that final program. However, other than the traditional infrastructure spending, it is too early to determine with much specificity the potential impacts on individual company valuations.

No Free Lunch: Corporate Taxes Will Be Going Up

Based on current U.S. trading activity, it appears that many investors are pricing in the additional potential revenue, earnings growth, and economic impact of the infrastructure plan, but the stock market does not yet seem to be focusing on the increased taxes that will likely be required to fund these initiatives. Depending on the size of the final infrastructure program, a number of different tax proposals are on the table to fund it.

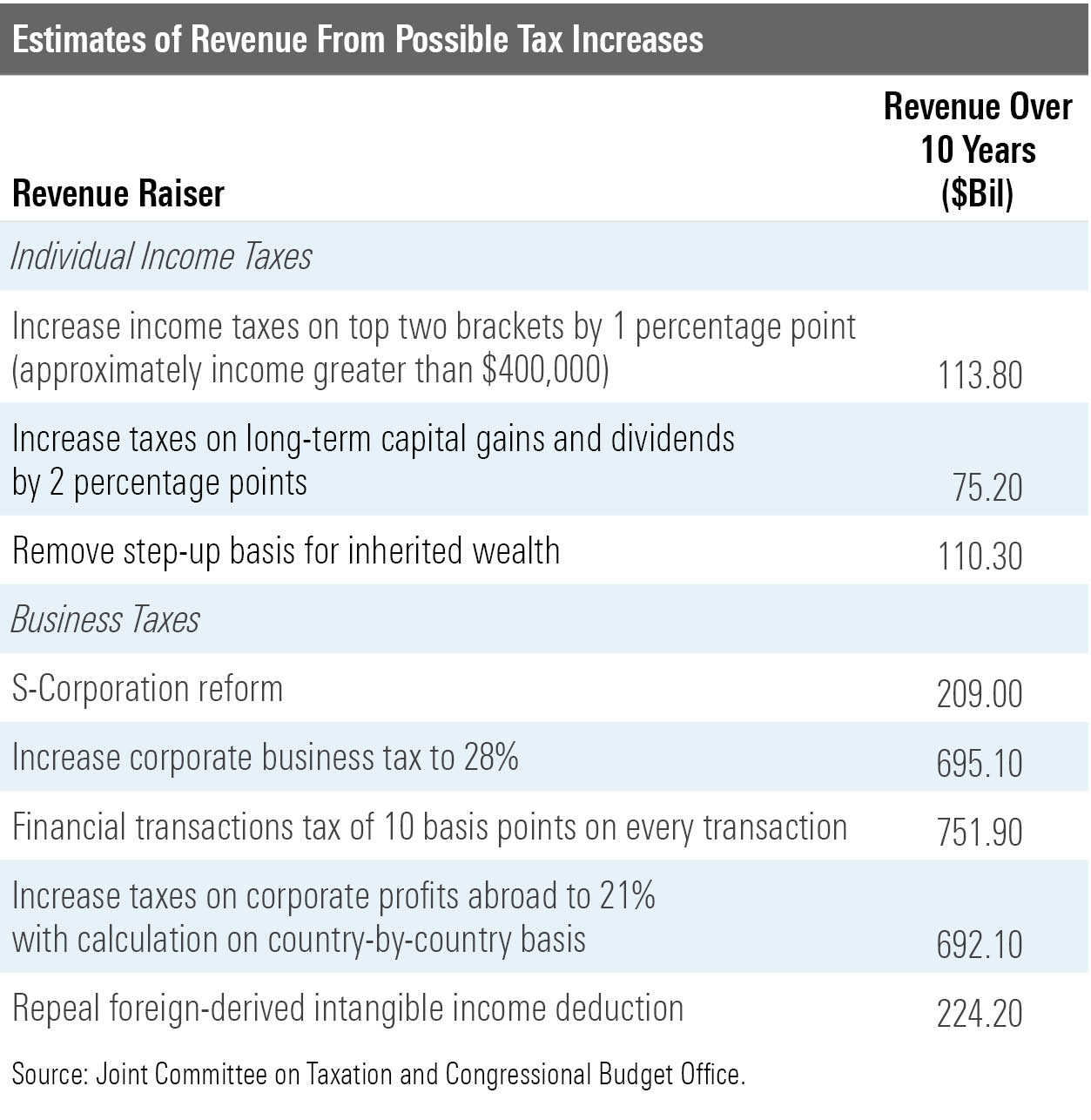

Morningstar head of policy research Aron Szapiro recently published an article detailing his thoughts on how the Biden administration can raise tax revenue to pay for its initiatives. He reviewed several types of potential tax increases and how much each would raise in revenue. The three main areas we are focused on are:

- Potential for increasing the corporate business tax.

- Increasing foreign corporate profits with a calculation on a country-by-country basis.

- Repealing the foreign-derived intangible income deduction.

The rate to which the corporate tax rate may rise and how the other proposals are structured remain subject to a wide range of change before any actual legislation is enacted.

If these changes are enacted as currently proposed, we estimate that they could reduce the intrinsic value of U.S. firms by a mid- to upper-single-digit percentage. However, that amount will vary from firm to firm. Some of the factors that will influence the impact of those potential changes are the amount of revenue and expense recognition domestically; the location of intellectual property; debt/equity capitalization; and the potential for specific companies to increase revenue greater than our current forecast from the increased infrastructure spending.

In addition, corporate lobbyists will look to influence the details of the final tax changes and minimize their clients' tax increases as much as possible. While Szapiro's article noted that we estimate the tax cuts in 2017 increased valuations by around 8%, the decrease in valuations by reversing those cuts may be more muted. Our expectation is that higher tax rates will not necessarily result in a sharp sell-off across the broad U.S. equity market, but that the implementation will act as a headwind for further valuation increases.

In our next articles, we share our analysis of the stocks that stand to benefit from the infrastructure plan, in both the traditional and nontraditional spending spaces.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZM7IGM4RQNFBVBVUJJ55EKHZOU.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_d910b80e854840d1a85bd7c01c1e0aed_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/K36BSDXY2RAXNMH6G5XT7YIXMU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)