Long Live the 60/40 Portfolio

The classic balanced portfolio wasn't slowed down by the worst quarter for U.S. core bonds this century.

/s3.amazonaws.com/arc-authors/morningstar/af89071a-fa91-434d-a760-d1277f0432b6.jpg)

It's a weekday. You know what that means. Somewhere, someone is pronouncing the classic balanced portfolio of 60% stocks and 40% bonds dead. Rising interest rates are the predetermined cause of death. Yet, as interest rates surged in the first quarter of 2021 and U.S. Treasuries were routed for their worst quarterly loss, the old-school balanced portfolio's performance was anything but an outlier.

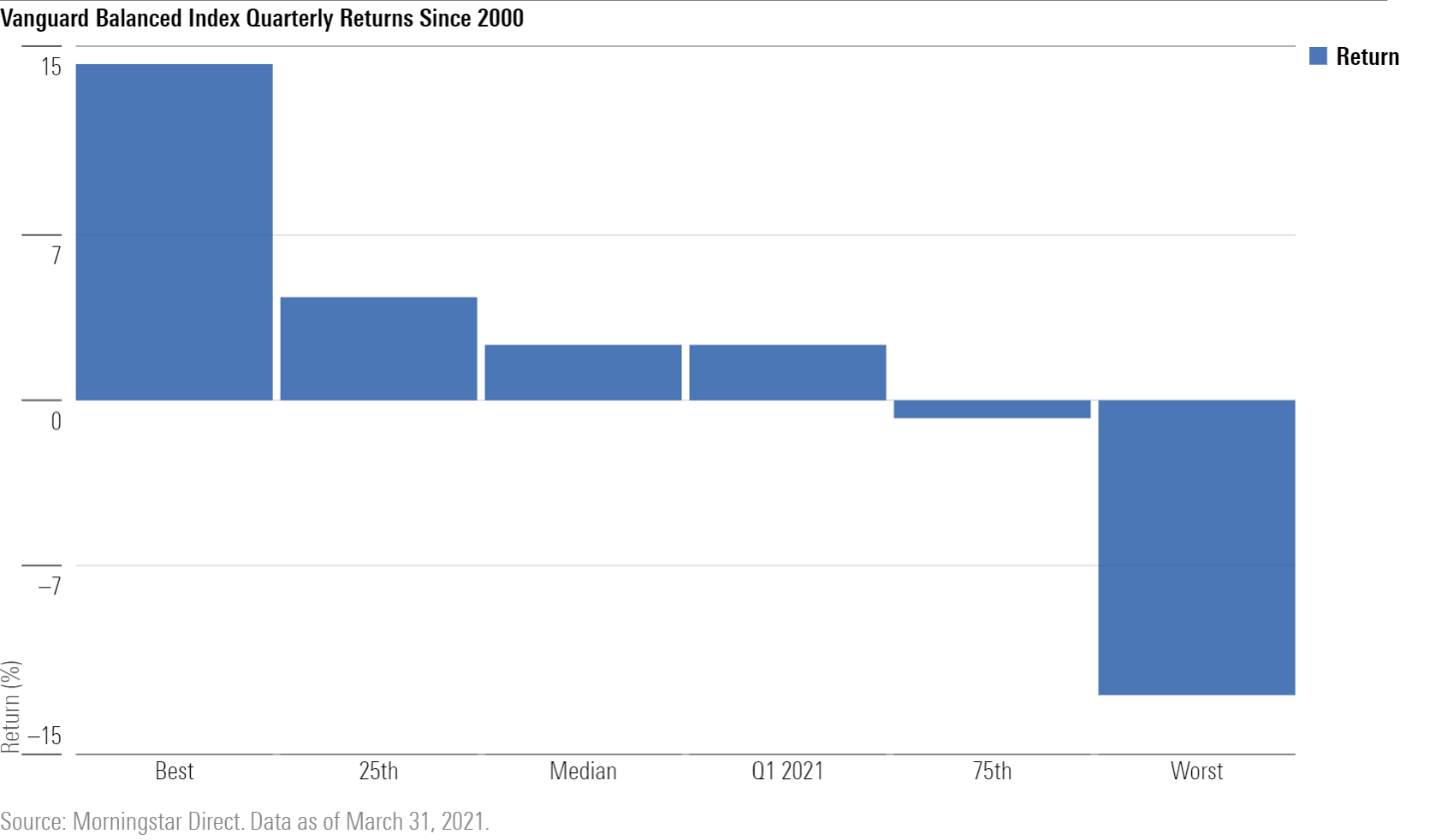

Vanguard Balanced Index VBAIX, a fund with a strategic 60% allocation to the U.S. total stock market (the CRSP U.S. Total Market Index) and a 40% allocation the U.S. total bond market (the Bloomberg Barclays U.S. Aggregate Bond Index), gained 2.4% for the first quarter of 2021. That was in line with the fund's 2.3% median quarterly return since 2000. Exhibit 1 shows a snapshot of the fund's range of quarterly returns over that period.

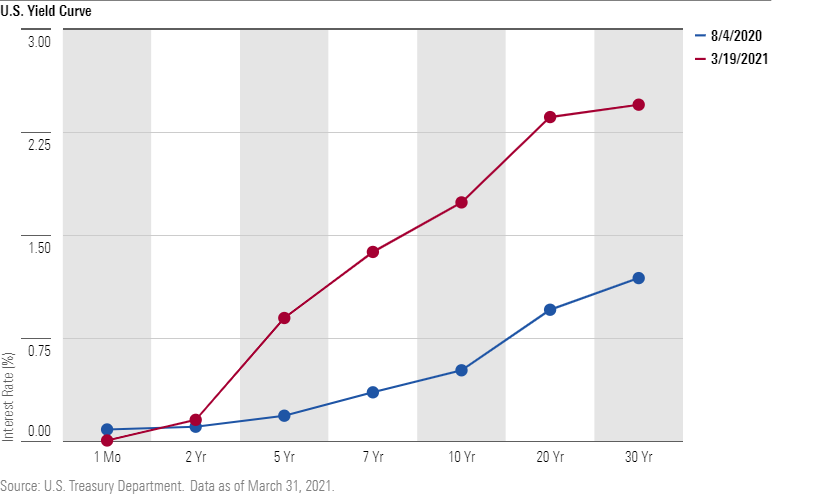

Within the context of the past 20 years, the 60/40 fund's 2021 first-quarter performance was a snoozefest. That's despite the 40% of the portfolio invested in U.S. core bonds, which had their worst quarterly performance since 2000. The bond portfolio suffered a 3.6% loss for the quarter as intermediate-term interest rates hit a post-coronavirus-pandemic high on March 19, 2021. Exhibit 2 shows how the U.S. yield curve steepened from the 10-year Treasury's low in August 2020 to its current high-water mark.

The spot rates furthest out saw the biggest increases in yield, but the middle of the yield curve also rose by about 1 percentage point. The steepening was the result of increased optimism for future U.S. economic growth spurred by the end of the pandemic and increased government stimulus.

Ironically for the 60/40 doomsayers, those same factors that caused interest rates to spike also spurred strong stock returns that more than outpaced the losses in the bond portfolio. The 60% of the portfolio invested in U.S. stocks gained 6.4% for the quarter.

Investors shouldn't expect stocks to surge every time interest rates rise, but the good news is that now that interest rates are no longer flirting with all-time lows, future rate increases should be less painful with higher starting rates.

Journey Before Destination

If interest rates continue to rise from here, the journey to whatever level they settle at as a result of the economy reopening and further government stimulus should only get easier with each step higher.

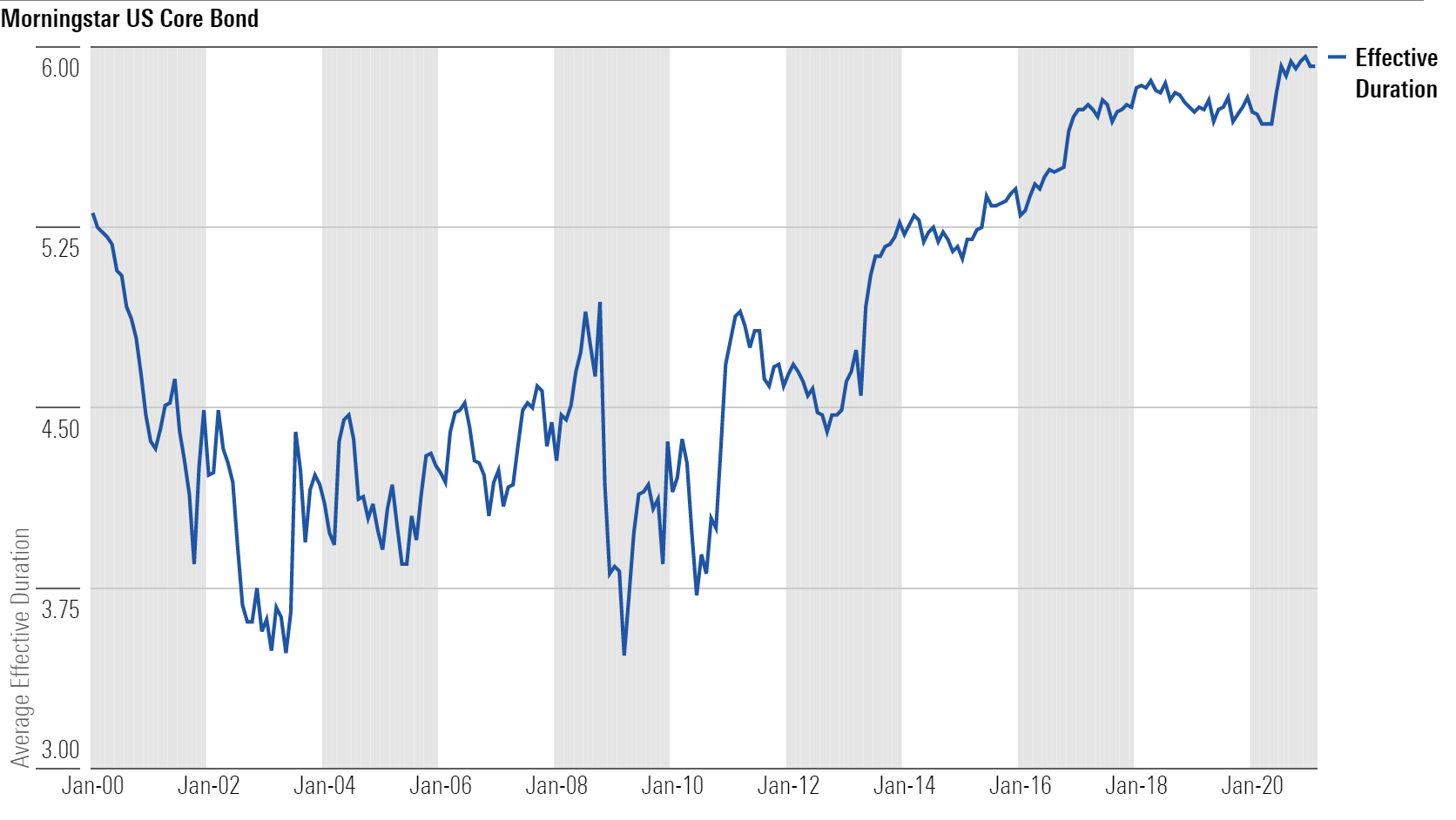

As Morningstar's Eric Jacobson pointed out in September 2020, it is a brave new world for core bonds. At the time of Jacobson's article, the duration of U.S. core bonds, a gauge of how much a bond's price is likely to rise or fall given a sudden change in market yields, was the longest it had ever been. By that measure, U.S. core bonds had never been more sensitive to changes in interest rates than in recent memory. Exhibit 3 shows how the effective duration of the Morningstar US Core Bond Index has changed since 2000.

The good news for 60/40 investors is that as rates rise, the duration, and sensitivity to changes in interest rates, falls. The effective duration of the Morningstar US Core Bond Index has already started to dip from its high in January 2021 as a result of increased rates. It obviously has a long way to go to reach its average duration over the last decade, but investors can take solace in knowing that each basis point of higher interest rates should be less painful than the one before it.

Strength Before Weakness

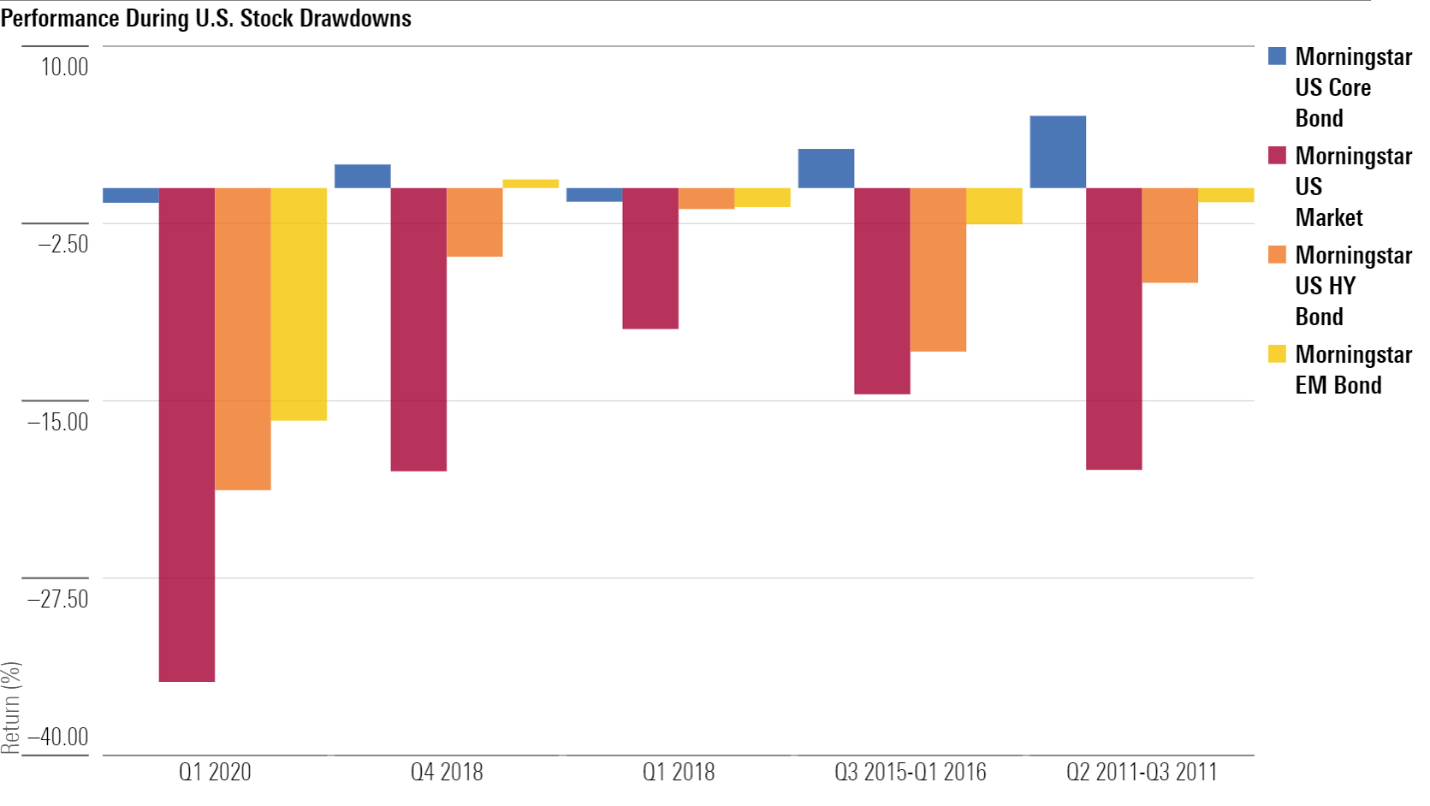

The concern over the risk of loss from rising interest rates belittles the reason U.S. core bonds play such a valuable role in the 60/40 portfolio in the first place. Even with low yields, these bonds continue to be a reliable ballast against equity market drawdowns, which are the real risk in a 60/40 portfolio. Exhibit 4 shows the performance of the Morningstar US Core Bond Index and other popular fixed-income alternatives with higher yields (high-yield and emerging-markets bonds) during the five worst drawdowns for U.S. stocks during the past decade.

During the first quarter of 2020's bear market, U.S. core bonds showed their value yet again as they held up much better than other fixed-income asset classes. It's not unexpected that more economically sensitive assets, like below-investment-grade corporate debt or sovereign debt issued by emerging-markets countries, would fare worse during times of heightened economic uncertainty. Those are also the periods that are worse for stocks.

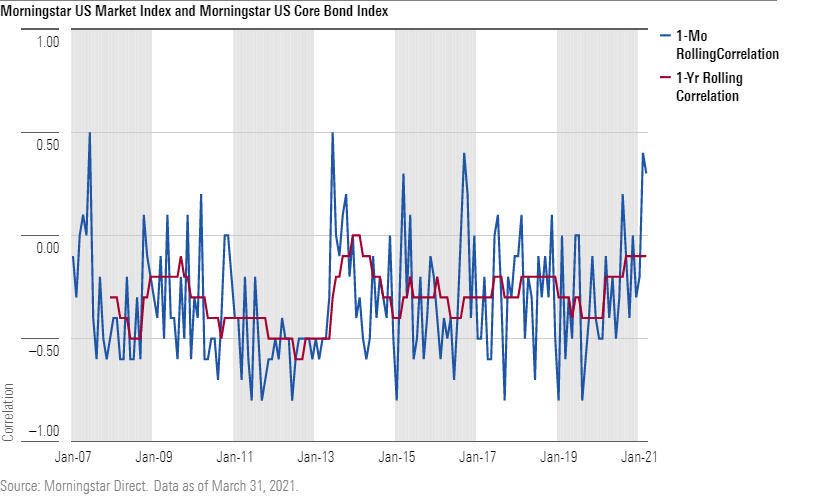

If U.S. core bonds were to behave more like stocks during these periods, that would pose a far greater threat to the 60/40 portfolio than rising interest rates. Indeed, during the first quarter we did observe a higher short-term correlation between core bonds and stocks. Exhibit 5 shows the rolling one-month and rolling one-year correlations between core bonds and stocks going back to January 2007. Both use daily returns.

Short-term correlations between U.S. stocks and bonds have fluctuated historically, so seeing a short-term spike isn't cause for concern. Even though some of the spikes haven't been fun for 60/40 portfolios (like the taper tantrum in 2013), they have at least been short-lived. Correlations between the two asset classes over one-month periods hasn't translated into higher longer-term correlations, which would be concerning. There's little reason to think the longer-term relationship between the two asset classes will meaningfully change given investors' continued preference for U.S. Treasuries during uncertain times.

Life Before Death

The first quarter of 2021 showed that even the worst quarter for U.S. investment-grade bonds in the last 20 years wasn't enough to derail the classic 60/40 portfolio. Sure, loading up the fixed-income portfolio with more risky bonds that are less sensitive to interest-rate changes would have led to better returns for the quarter, but over the longer term, it's a different case. Broad U.S. investment-grade bond exposure, such as the Aggregate Index, continues to provide ballast against the large equity market drawdowns that could actually derail the portfolio.

Of course, this doesn't mean it'll be all sunshine for the 60/40 portfolio going forward. There will be periods where stocks sink and returns are compromised, such is investing. But investors using a 60/40 portfolio shouldn't let the threat of rising interest rates lead them to more risky portfolios that could thwart their investing goals.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/af89071a-fa91-434d-a760-d1277f0432b6.jpg)