What to Know as Squarespace Goes Public

The established website builder sees growth opportunities but faces stiff competition.

/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)

Technology startup Squarespace, previously valued at around $10 billion, began trading today, May 19, in a direct listing. Squarespace is a one-stop shop for anyone who wants to build a digital presence; the company offers everything from website-building to payment services to customer relationship tools to brand management.

Investors shouldn't anticipate a drastic change in direction for the company after the public offering. Founder and CEO Anthony Casalena will retain a majority of the voting power, so shareholder resolutions aren't likely to rock the boat.

Squarespace aims to appeal to a growing market of businesses both large and small along with individuals who want a bigger online presence. But serving many kinds of customers also means facing many competitors--and competition is fierce.

The Public Offering at a Glance

- Ticker: SQSP

- Listing Date: May 19, 2021

- Exchange: New York Stock Exchange

- Publicly Tradable Shares: About 40 million

- Percentage of the Company Made Public: About 30%

- Reference Price: $50

- May 19 Opening Price: $48

- May 19 Closing Price: $43.65

- Market Cap: About $6 billion

Unlike an IPO, company shares were immediately made available to the public, and the opening share price was determined by the orders coming in for Squarespace stock. The company does not receive any proceeds from the offering.

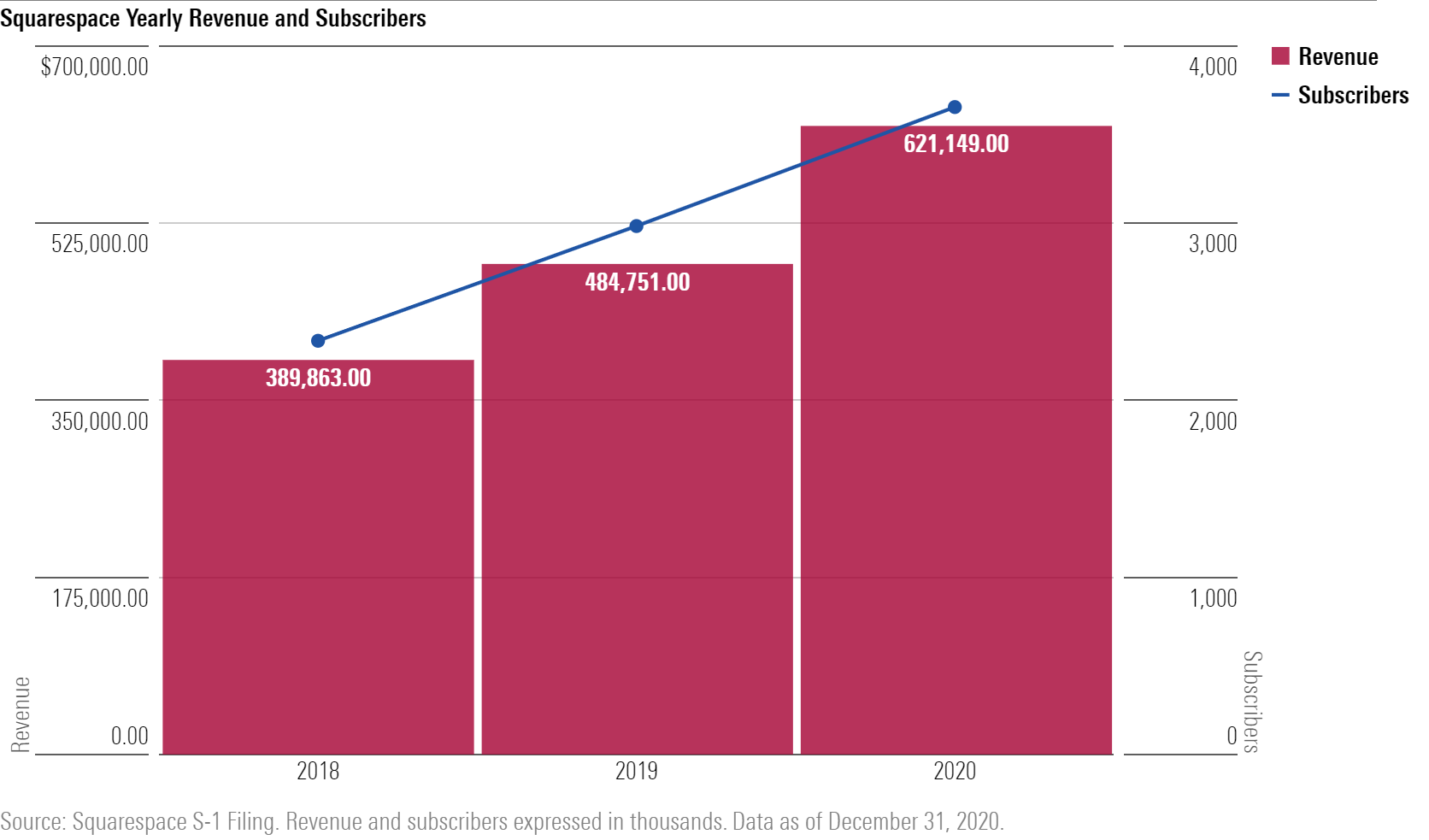

Squarespace's Growth Trajectory

Founded in 2003, Squarespace is an Internet veteran, and it has managed to consistently grow both its user base and revenue. The company first became profitable in 2016 and has since continued to perform well. At the end of 2020, Squarespace had roughly 3.7 million subscribers and brought in $621 million in revenue for the year. Both figures marked significant growth from the year before.

Though its user base grew in 2020, its net profit fell to $30.6 million for the year, down 47% from 2019. According to the company's SEC filing, the decline in profit was largely due to increased sales and marketing costs, which may be an indicator of competitive pressure in the space.

Who's Competing With Squarespace?

While Squarespace has built itself up over the years to serve many different customer segments, many of its competitors take a more targeted approach. The spaces that Squarespace inhabits are crowded with both startups and public companies, many of which our analysts believe have long-term competitive advantages.

Beyond domain acquisition and website construction, where Squarespace competes with GoDaddy GDDY and Wix.com WIX, e-commerce is a key area for the company and a target for future growth. But capturing market share in this packed house is no easy task.

Morningstar research suggests that Shopify SHOP is the leading e-commerce platform for small and midsize businesses, a key customer segment for Squarespace. Further, equity analyst Dan Romanoff says he believes Shopify's competitive advantage derives from switching costs, while Adobe's ADBE Magento is also strong in the midmarket space. Small and midsize businesses are less likely to switch platforms because of the financial and operational costs involved. Still, both companies will have the opportunity to capture new entrants into the market as e-commerce continues to gain momentum.

On the customer relationship front, Squarespace competes with established names like Salesforce.com CRM and Zendesk ZEN. Romanoff says he believes that Salesforce.com "has assembled a front-office empire that it can build on for years to come." Like Shopify, Salesforce.com enjoys a long-term competitive advantage derived from switching costs--its acquired customers are unlikely to switch platforms. In fact, the company's customer retention is over 90%. According to Romanoff, Zendesk joins Salesforce.com as a leader in customer service and engagement software.

Despite strong competition, Romanoff says that the opportunity in this space is substantial--the market is still growing rapidly and could be up to 3 times larger in the long run.

Is Squarespace's Dependence on Third-Party Platforms a Risk?

While Squarespace offers many proprietary solutions, it does have several dependencies to consider, particularly when it comes to handling transactions. Squarespace uses Stripe, an online payment processing platform developed by another tech startup, to process transactions with its customers. The company also offers payment processing integrations for its customers to charge their users through Stripe, PayPal PYPL, and Square SQ.

Squarespace acknowledges in its SEC filing that "the success of [its] platform depends, in part, on [its] ability to integrate and offer third-party services to our customers." Disruptions or problems with these services would have a direct impact on Squarespace. It could also suffer costly setbacks if any of these companies choose to terminate their relationship with the company.

Squarespace Eyes Expansion in Growing Markets

Increasing global Internet usage will likely continue to drive growth in the customer segments that Squarespace serves, creating opportunities that don't require the company to take market share from its competition. Squarespace can target new entrants into the market, including individuals and both new and established businesses building an online presence for the first time. The company has already demonstrated its ability to consistently grow its user base year over year.

In its SEC filing, Squarespace identifies favorable industry trends, including the rise of online commerce and direct-to-consumer relationships. These consumer-driven trends will push businesses to establish their online presence and seek solutions that give them control over their customer relationships. As a streamlined provider of a variety of solutions, Squarespace is poised to take advantage of the growing demand for online tools. Still, Squarespace will be under pressure to constantly innovate--a difficult task for any company.

Squarespace has so far continued to innovate and grow to take advantage of new opportunities, like making inroads through strategic acquisitions, but tight competition may cause the company to become less profitable over time. As evidenced in 2020, Squarespace may have to spend more on sales and marketing to fend off competitors. It may also face pressure to reduce prices because of competition, which could eat into the company's profits.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PLMEDIM3Z5AF7FI5MVLOQXYPMM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/I53I52PGOBAHLOFRMZXFRK5HDA.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CEWZOFDBCVCIPJZDCUJLTQLFXA.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)