Infinity Q: The Fund that Checked All the Wrong Boxes

When investments come with warning signs.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

A Hedge Fund for the Masses On Monday, Feb. 22, disaster struck Infinity Q Diversified Alpha Fund IQDAX. The SEC announced that Infinity Q’s management had asked the commission’s permission to deny redemptions for Diversified Alpha, meaning that its investors would be unable to sell their shares. Shortly thereafter, Infinity Q fired the fund’s portfolio manager, James Velissaris, who was also the company’s founder. (Neat trick, that.)

Why the fund closed its doors (the SEC granted the request) and dismissed its portfolio manager I will divulge shortly. First, though, let’s run through the indicators that should have concerned the fund’s investors. There were many.

To start, Diversified Alpha was marketed as a "hedge fund for the masses." If that phrase doesn't have you walking backwards toward the nearest exit, while clutching your wallet, then your survival instinct needs honing. However, to judge from the response to my 2019 article about private-equity funds seeking permission to sell into 401(k) plans, few readers need be reminded why foxes visit henhouses. The opposition to the SEC's proposal was fierce. (It passed anyway.)

Worse, Diversified Alpha wasn’t pitched as a hedge fund because it traded rapidly, leveraged its equity holdings, or sold short. Such tactics, to be sure, can be dangerous. But the fund’s actual tactics were more perilous yet, because it built a portfolio that no outsider could analyze. Ultimately, Infinity Q’s investors were entirely at the fund company’s mercy. They could not know what they owned.

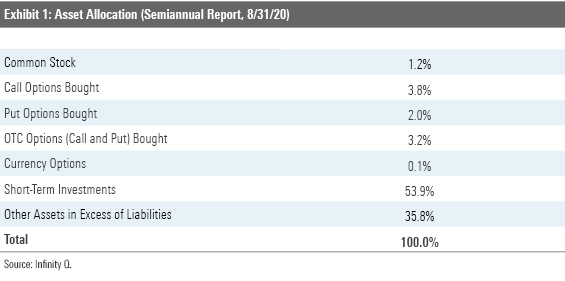

The Black Box That is no exaggeration. This was Diversified Alpha's official portfolio allocation at the date of its last semiannual report:

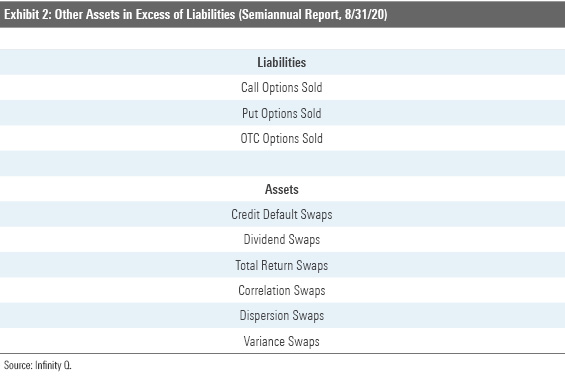

After stripping out the cash, the category of Other Assets in Excess of Liabilities accounted for more than 75% of the fund’s meaningful investments. That’s one very large junk drawer! The notes indicated these items as consisting of:

In fairness to Infinity Q’s management, the report provided extensive details about the fund’s swap positions: strike prices, counterparties, termination dates, realized gains and losses, even the constituents of its customized baskets. But the data alone do not suffice; to understand the implications of the fund’s swaps, one would have needed to run that information through a pricing model.

Even then, the task would have been daunting. By the Financial Accounting Standards Board's definition, 18% of the portfolio was invested in Level 3 Assets--its least reliable category. Level 1 Assets are conventional securities that may readily be priced, such as stocks and liquid bonds. Level 2 Assets trade less often, but their values are easy to estimate. At the bottom are Level 3 Assets, which, per the FASB, require "unobservable inputs that are not corroborated by market data."

High Hopes, at High Cost To rephrase, Infinity Q's investors were required to take management's word, which was, shall we say, highly optimistic. According to a potential buyer of Infinity Q funds, cited in an article by Institutional Investor, the fund's portfolio manager stated that he would limit portfolio losses to 2%. An ambitious claim, considering that in November 2016, staid Vanguard Intermediate-Term Bond Index VBIIX dropped considerably further, losing 3.4% for the month.

That promise did not come cheaply. Per the August 2020 report, the expense ratio for Diversified Alpha’s Investor Shares was 2.24%, and that of its Institutional shares at 2.02%. A bargain by hedge fund standards, but distinctly pricey for a publicly available fund. Alternative investments are the costliest form of mutual fund, but even they have average expenses that are below 2%.

In summary, the fund:

1) Boasted of its institutional pedigree.

2) Used an investment strategy so complex that management’s claims could not be independently verified.

3) Held substantial assets that were illiquid and difficult to value.

4) Promised that its investment risk would be unusually low.

5) And charged a whopping fee for the privilege.

No single item was devastating--well, except for the fund's expenses, as I cannot conceive of paying more than 2% for a mutual fund--but the combination clanged the alarm bells.

A final concern was the company's size. Infinity Q has only 11 to 15 employees, according to its Form ADV. Usually when publicly traded funds suffer meltdowns, those funds are sponsored by smaller organizations. That occurs because major fund companies typically impose strict risk controls on their investment managers that prevent them from taking too much rope. However, smaller firms sometimes skip that step.

The Prices Weren't Right As did Infinity Q's management. In customary fashion, the value of the fund's Level 3 Assets was estimated by an outside pricing model. Very much not in customary fashion, Diversified Alpha's manager adjusted that model, thereby generating higher estimates. That's one way to ensure that the fund posted only minimal losses--fix the prices that determine the fund's returns. Infinity Q's management, of course, should have prevented such meddling. But it did not.

The fund is now scheduled to liquidate its investments, thereby self-terminating. That decision seems drastic. After all, replacing Velissaris’ estimates with those from the model would address the fund’s pricing problems. True, its net asset value might still be incorrect, because Level 3 Assets cannot be priced with full accuracy by any party, but at least the results would be independently derived.

What happened, I suspect, is that management foresaw a run on the bank. Following the news of the fund’s scandal, shareholders would bolt once the fund was repriced and the redemption gate lifted. Although the fund does own a substantial amount of cash and liquid options, those redemptions might be so large as to force it to unwind its custom swaps. Doing so would generate heavy losses, as those contracts are not easily sold. Thus, better to keep the fund shut, while liquidating its assets methodically.

In conclusion: Not every fund that carries warning signs implodes, but funds that lack warning signs rarely do. When I see such indicators, I head elsewhere. There are thousands of fish in the mutual fund sea.

Note: If you clicked on the link to Diversified Alpha’s Morningstar report, you may have noticed that the fund received a Morningstar Analyst Rating of Silver--the second-highest of the five possible Analyst Ratings. You may also wonder why my view differs so sharply from the analyst who assigned that score. The answer is that it does not. All Morningstar analysts would have been wary of Diversified Alpha. That rating was quantitatively assigned, as Diversified Alpha was not large enough to receive coverage from a Morningstar researcher. (The small Q to the right of the rating indicates that it was quantitatively generated.)

This is not to denigrate the quantitative ratings. They have their strengths, being invariably objective and consistently calculated. There are times when the quantitative ratings predict more accurately than their human counterpoints would have done. However, they struggle when evaluating funds that use uncommon investment strategies. In such cases, the art of investment analysis often outdoes the science.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WJS7WXEWB5GVXMAD4CEAM5FE4A.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NOBU6DPVYRBQPCDFK3WJ45RH3Q.png)