Digging Into Berkshire Hathaway’s Portfolio

Morningstar’s Global Risk Model reveals how the investment giant’s equity holdings stack up on 11 measures of risk.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

For investment aficionados, there’s no better person to learn from than Warren Buffett, probably the best capital allocator of the 20th century. Berkshire Hathaway’s BRK./BRK.B equity portfolio is now partly in the hands of two other managers, Ted Weschler and Todd Combs, who are each responsible for investing a small slice of the company's collection of investment securities.

In this article, I’ll use Morningstar’s Global Risk Model to analyze the underlying characteristics of Berkshire’s equity holdings. The portfolio remains highly concentrated and shows Buffett’s distinctive imprint in many ways, but has also evolved over time to become more modern and technology-focused.

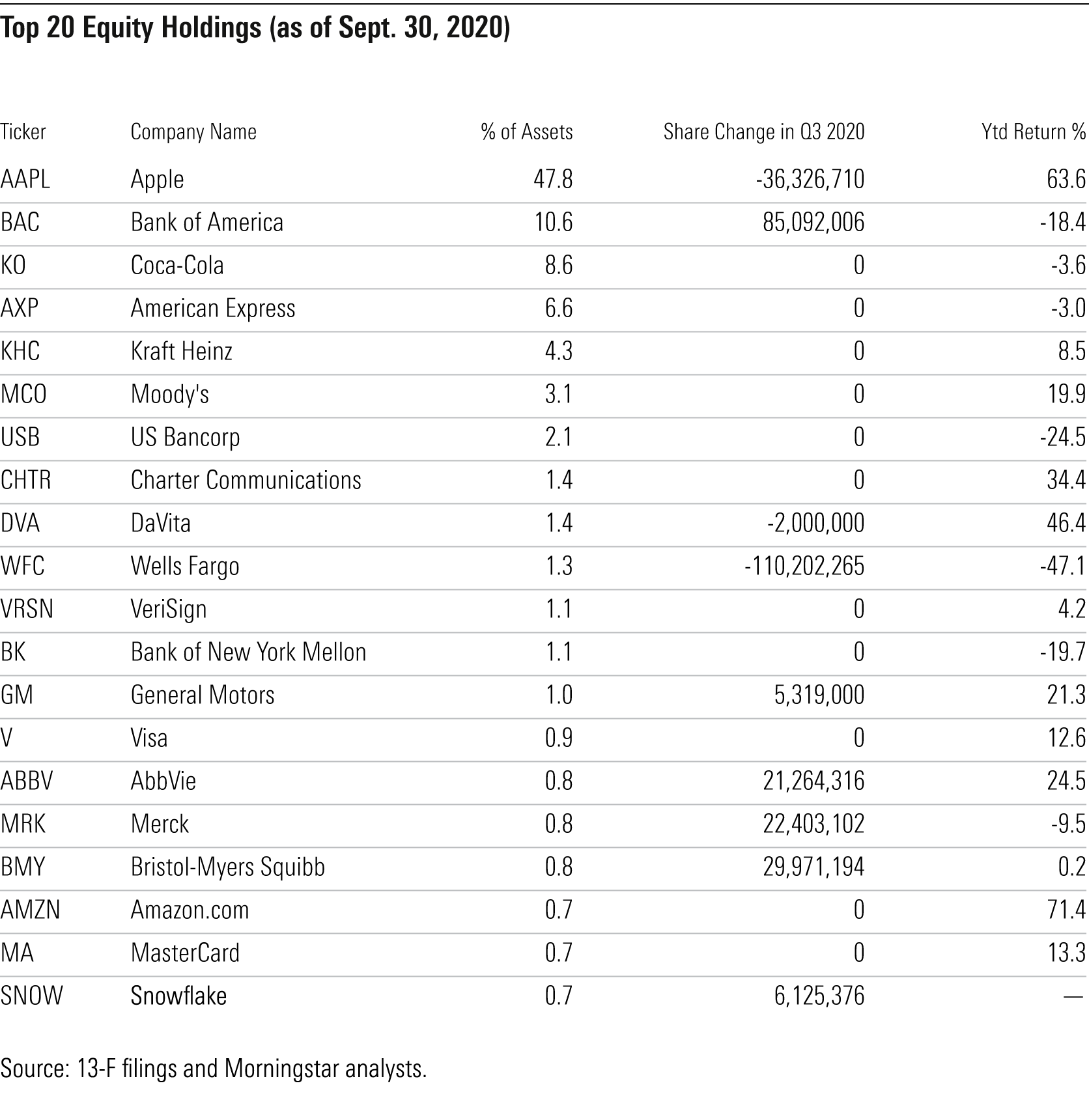

Looking Under the Hood Like all institutional investment managers with at least $100 million in assets under management, Berkshire is required to report its consolidated equity investments in quarterly 13-F filings with the SEC. Berkshire's most recent 13-F disclosed 50 stock positions totaling nearly $230 billion as of Sept. 30, 2020. Because investment managers are only required to disclose transactions made on U.S. exchanges, the filing doesn't show holdings in international stocks unless they're held via the U.S. ADRs.

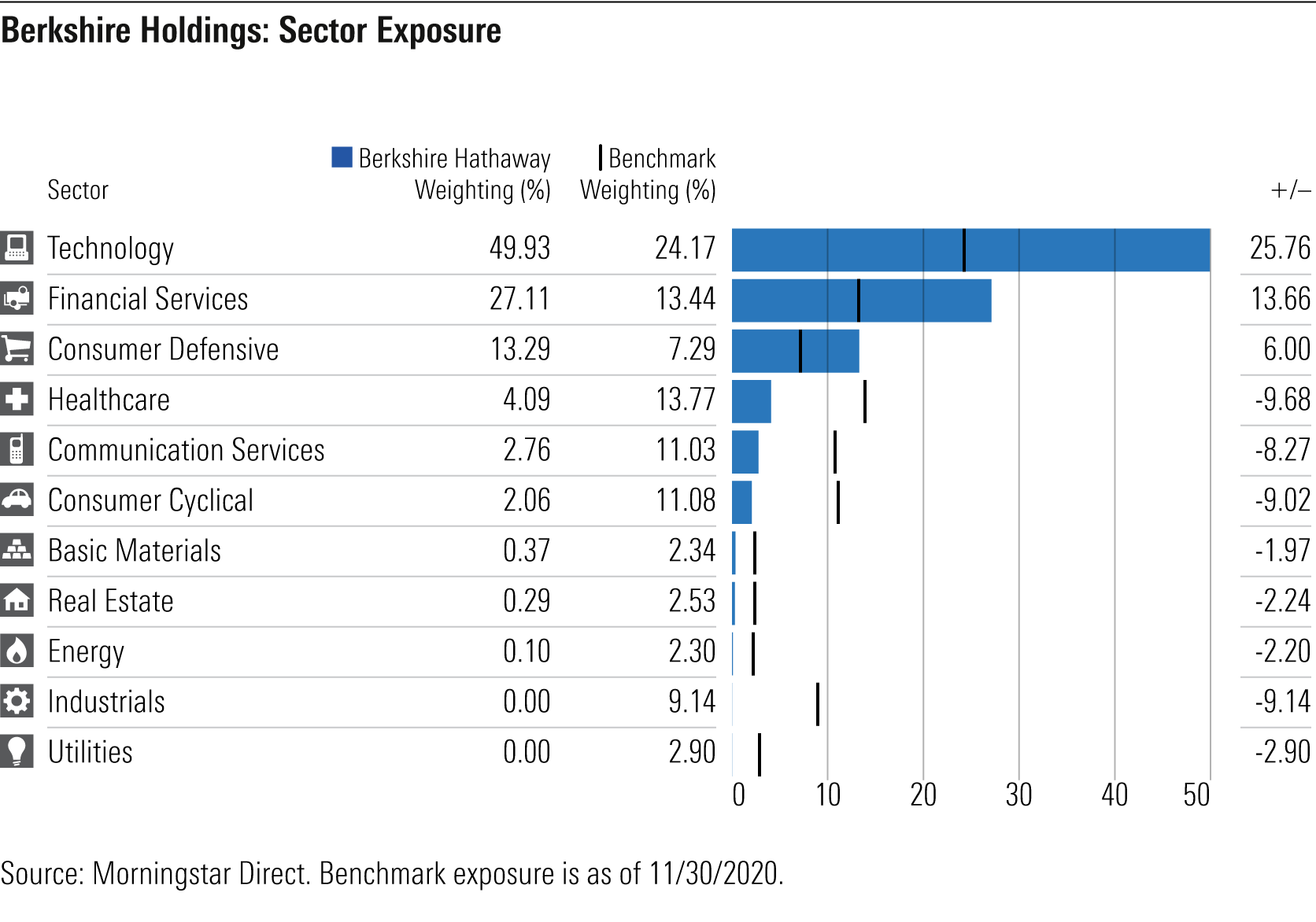

Not surprisingly, Berkshire’s portfolio is far from conventional. Buffett has long downplayed the value of diversification, preferring to make highly concentrated bets on a small handful of companies that he knows inside and out. As a result, it’s an unusually concentrated list. Apple AAPL, which Buffett and his team first started buying in 2016, now makes up nearly 48% of its total 13-F equity holdings, even after the team sold about 36 million shares in the third quarter of 2020. Other major holdings include American Express AXP, Bank of America BAC, Coca-Cola KO, and Kraft Heinz KHC.

Berkshire’s operating subsidiaries focus on boring but profitable areas such as insurance, rail transportation, regulated utilities, and industrials firms, but its equity holdings are anything but old-school. For most of his career, Buffett avoided investing in technology companies, averring that “if there’s lots of technology, we won’t understand it.” He finally bought shares in IBM IBM in 2011, explaining that his thinking on the company finally crystallized after reading its annual report for 50 years. IBM is no longer in the portfolio; instead, Apple (which Buffett has come to see as both a consumer firm and a technology company) currently accounts for nearly all of the portfolio’s outsize weighting in technology stocks. The team also recently added a small stake in Snowflake SNOW, a cloud data storage platform that recently went public.

Berkshire also has relatively heavy weightings in financial services (such as American Express) and consumer defensive names (like Coca-Cola). The team recently added shares in several large-cap pharmaceutical stocks, including AbbVie ABBV, Merck MRK, Pfizer PFE, and Bristol-Myers Squibb BMY, but the portfolio remains light on healthcare overall. It’s also significantly underweight in communications services, consumer cyclicals, and industrials.

Next, let’s take a deep dive into Berkshire’s holdings using the 11 style-based factors in our Global Risk Model.

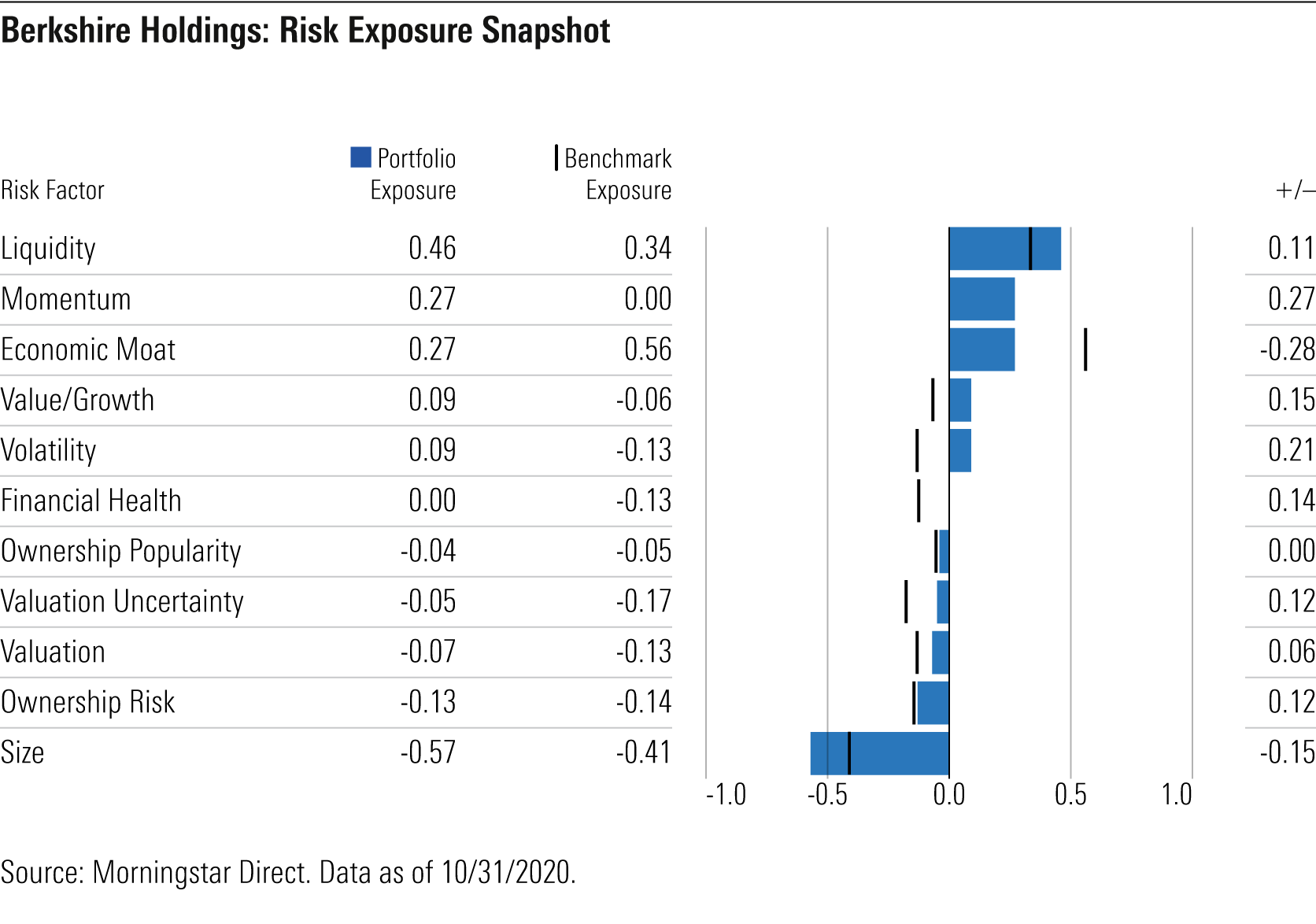

How Berkshire's Holdings Stack Up on 11 Different Factors The Morningstar Global Risk Model includes 11 style-based factors that help shed light on a portfolio's underlying risk exposure. Six of the 11 style factors (Valuation, Valuation Uncertainty, Economic Moat, Financial Health, Ownership Risk, and Ownership Popularity) are based on Morningstar's fundamental equity research and extensive ownership data. The other five factors--Liquidity, Size, Value-Growth, Momentum, and Volatility--are traditional risk factors that have been widely studied by academic research. We express each score in terms of the number of standard deviations from the average (also known as a z-score), with a score of zero indicating the average score for a universe of about 7,000 domestic stocks. We set the sign of each exposure so that positive numbers are generally associated with factors that have shown a positive effect on returns over time.

Liquidity: The Liquidity factor measures a stock's average trading volume over the past month relative to total shares outstanding. It's basically a measure of how quickly a stock's ownership base changes hands between different investors. Overall, Berkshire's holdings score relatively high on liquidity, with a z-score of 0.46 versus 0.34 for the S&P 500. This bias for more-liquid stocks is probably a function of both Berkshire's size, as it would be difficult for it to take meaningful positions in more thinly traded stocks, and the fact that the equity portfolio still acts as a backstop for the insurance operations. The equity portfolio does include some holdings in less-liquid shares, such as RH RH and Axalta Coating Systems AXTA, but those positions tend to be very small.

Momentum: The Momentum factor measures how much a stock has risen in price over the past year relative to other stocks. Academic research has consistently found that stocks that have recently performed well generally continue to perform well even after accounting for other factors that tend to drive returns. Surprisingly, Berkshire's holdings score relatively high on Momentum, with a z-score of 0.27, compared with zero for the S&P 500. This doesn't reflect an investment strategy geared toward buying momentum stocks but is more likely a side effect of positive stock-price performance trends for larger holdings such as Apple.

Economic Moat: The Economic Moat factor is based on the Morningstar Quantitative Economic Moat Rating, which is designed to measure the strength of a firm's competitive advantage based on the sustainability of its profits. Higher scores suggest a firm will be able to keep competitors at bay for an extended period. Oddly enough, given Buffett's well-known affinity for economic moats, Berkshire's holdings score below average on this factor. The list includes some wide-moat stalwarts, such as Coca-Cola and Moody's MCO, but a few no-moat holdings, such as Kraft Heinz and General Motors GM, pull down the overall score. Apple's narrow economic moat rating is another significant reason behind the portfolio's lower overall rating for this metric.

Value-Growth: This factor measures value and growth characteristics based on how the market is pricing a stock. If a stock's current price is high relative to a simple price estimate based on earnings yield, dividend yield, and book value, that suggests the stock has higher growth expectations baked into its current price. On the flip side, a low current price relative to the simple price estimate indicates a value leaning. Berkshire's holdings score higher than the overall market on the Value-Growth factor, reflecting higher growth expectations for holdings such as Apple, Moody's, and Verisign VRSN.

Volatility: Our Volatility factor is based on a stock's range of historical prices over the past year. Based on our research, stocks with higher volatility scores have statistically outperformed over longer time periods, but also have a wider range of expected outcomes. Berkshire's holdings score above average for volatility, with a z-score of 0.09, compared with negative 0.13 for the S&P 500. Apple carries a lot of weight in the overall score, with its above-average volatility more than offsetting lower-volatility holdings like Coca-Cola and Merck.

Financial Health: The Financial Health factor is based on strength of a firm's financial position and ranks companies based on how likely they are to fall into financial distress. Higher scores imply stronger financial health and therefore a lower risk of bankruptcy. Stocks that score well based on this factor tend to hold up better during economic downturns, such as the global financial crisis in 2008. Berkshire's stocks score above average on Financial Health, with an average z-score of zero, compared with negative 0.13 for the S&P 500. Nearly all of the largest holdings have decent Financial Health scores, more than offsetting weaker balance sheets for smaller holdings such as General Motors.

Ownership Popularity: The Ownership Popularity factor represents the growth in the popularity of a particular stock from the perspective of fund manager ownership. High Ownership Popularity scores indicate that more fund managers have been increasing their positions in the stock over the past several months. Berkshire's holdings rank about in line with the overall market based on this metric, suggesting that it's neither following trends nor following a pronounced contrarian strategy.

Valuation Uncertainty: The Valuation Uncertainty factor is based on Morningstar's Quantitative Uncertainty Rating and measures the level of uncertainty embedded in a company's Quantitative Fair Value Estimate. Companies with less-consistent operating earnings and capital spending tend to have less-stable cash flows, making it more difficult to pin down an estimated fair value. Higher scores imply greater uncertainty with a wider range of potential valuation outcomes. By extension, portfolios with high scores for Valuation Uncertainty tend to have more volatility in returns. Berkshire's holdings have a portfolio z-score of negative 0.05 for Valuation Uncertainty, compared with negative 0.17 for the S&P 500. Financial holdings such as American Express, Bank of America, and Wells Fargo WFC (which Berkshire has been selling) have some of the higher ratings for Valuation Uncertainty.

Valuation: The Valuation factor measures how cheap or expensive a stock is relative to Morningstar's Quantitative Fair Value Estimate, which is based on a statistical model that calculates fair values based on a company's projected future cash flows. Higher scores indicate the company is undervalued and more likely to generate positive future returns. The Berkshire portfolio scores fairly well on this metric, with a z-score of negative 0.07, compared with negative 0.13 for the S&P 500.

Ownership Risk: The Ownership Risk factor defines a stock's risk level based on the company it keeps. We gauge Ownership Risk by looking at the risk profiles of the funds that own shares in the same security. If funds owning the stock tend to have high risk profiles, we assign a higher Ownership risk score. Berkshire's holdings are roughly in line with the S&P 500 based on this metric, despite small weightings in riskier stocks such as Teva Pharmaceutical Industries TEVA, Barrick Gold GOLD, and RH.

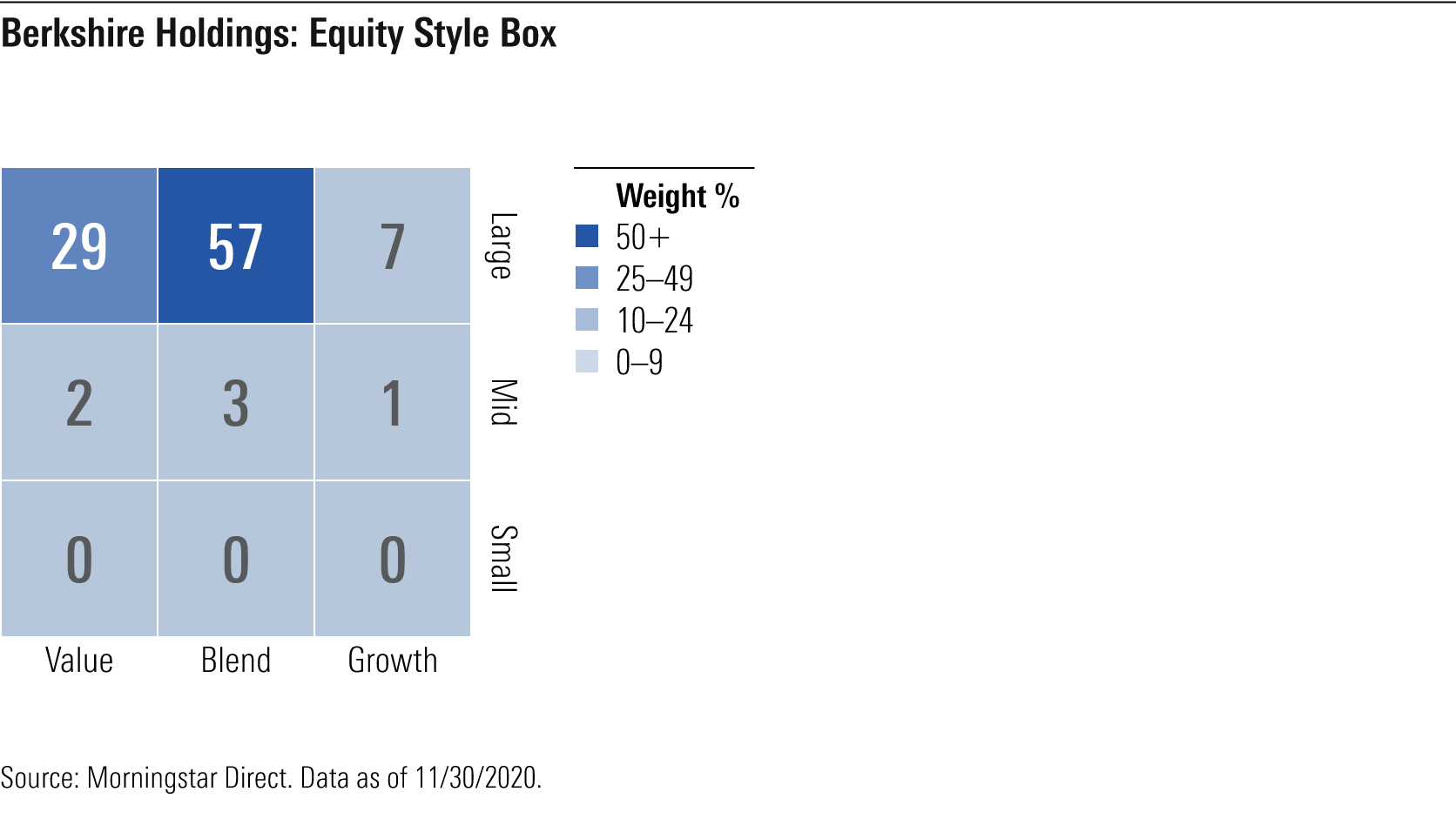

Size: The Size factor is based on the market capitalization of the stocks included in a portfolio, with higher scores indicating more exposure to smaller-cap stocks. Academic research has found that smaller-cap stocks tend to outperform over longer time periods, although larger-cap names have taken a strong lead over the past decade. Berkshire's huge asset base makes it nearly impossible for it to take meaningful positions in smaller-cap stocks, so it shouldn't come as a surprise that if we break down the portfolio along Morningstar Style Box lines, none of its holdings land in the small-cap row, and only 6% of the portfolio lands in mid-cap territory. Instead, nearly all the holdings land in the large-value and large-blend squares.

Conclusion As a group, Berkshire's holdings don't hew closely to the market on most dimensions of risk. Even as Buffett has started giving more investment discretion to his lieutenants (each of which is managing an estimated $15 billion in equities), the portfolio hasn't exactly turned into a closet indexer. In fact, the portfolio is so different from the mainstream that its investment strategy could be encapsulated by top holding Apple's erstwhile tagline: Think Different. Because of its heavily concentrated portfolio, it stands out for its hefty technology weighting and above-average exposure to momentum, volatility, and growth.

These characteristics probably aren’t what you might expect from Berkshire Hathaway. But the legions of investors who still count on it as a quasi-mutual fund for their life savings likely aren’t complaining. While mutual funds have increasingly shifted toward passive investment strategies, Berkshire remains as idiosyncratic as ever.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T5MECJUE65CADONYJ7GARN2A3E.jpeg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)