When Bonds Do Not Hedge Stocks

For the first time in decades, bonds haven’t protected balanced portfolios. What to do?

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

The Formula Fails

The formula had worked perfectly for 40 years. Invest predominantly in stocks. Occasionally, they lose a great deal of money, but over time they profit handsomely. Cushion the inevitable stock market blows with Treasury bonds. When equities decline, Treasury bond prices inevitably will increase, because during stock bear markets investors seek safety. Risk on, risk off.

As Morningstar’s Amy Arnott writes, that seemingly foolproof approach has at long last flopped. Stocks have plummeted; long bonds have plummeted. For several decades, the umbrella provided by balanced funds had shielded both sun and rain. However, when the flood arrived, the umbrella no longer sufficed.

(The recent marketplace has supplied a useful lesson about the limitations of statistics. For the year to date, both Vanguard 500 Index and Vanguard Long-Term Treasury Index have lost more than 20%. Yet the correlation between the two funds’ weekly returns has been negative. Each has suffered for the same reason—high inflation and rising interest rates—but because the timing of their losses has been slightly asynchronous, the correlation calculation is misleading. Sometimes, statistics are inadequate; the researcher must catch what the numbers missed.)

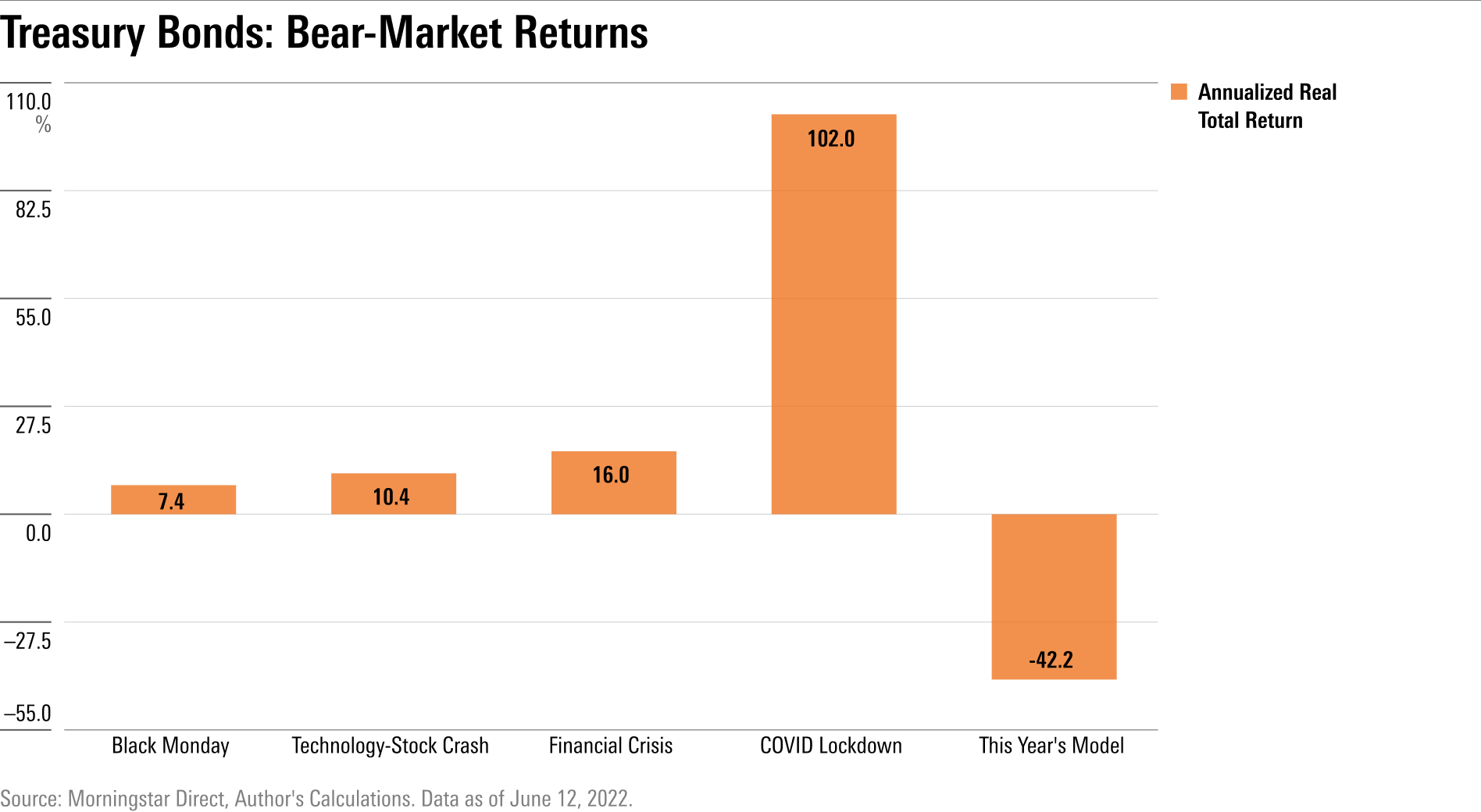

The following chart demonstrates the extent of bonds’ 2022 failure. It shows the annualized rate of return for 20-year Treasury bonds, as represented by the Ibbotson Associates Long Government Bond Index, during the major bear markets of the past four decades. (If a couple of these results seem very high, remember that they are annualized figures, derived from shorter time periods.)

Ouch! That outcome has wrought havoc on allegedly safe funds. This week, a reader wrote to me, “I am bewildered by the performance of Vanguard STAR. Wasn’t this fund designed as an all-in-one option? It is tanking.” Indeed, it is. Vanguard STAR is down 20% so far this year. But its misery shares plenty of company. Every flavor of balanced portfolio has suffered, including target-date funds. With rare exception, all rely upon a similar blueprint of risk on, risk off.

Option 1: Stay the Course

Balanced-fund investors have three options. One is to pretend that this year never happened, by continuing to do what they have long been doing. Playing ostrich seems silly; even enigmatic gurus rarely suggest poking one’s head into the sand. But it often is sound investment policy.

After Black Monday, many asserted that strategic asset allocation was dead. The stock market’s abrupt plunge had demonstrated the need for market-timing. After the technology-stock crash, hedge funds became fashionable. Several years later, following the financial crisis, the watchword was “liquid alternative funds.”

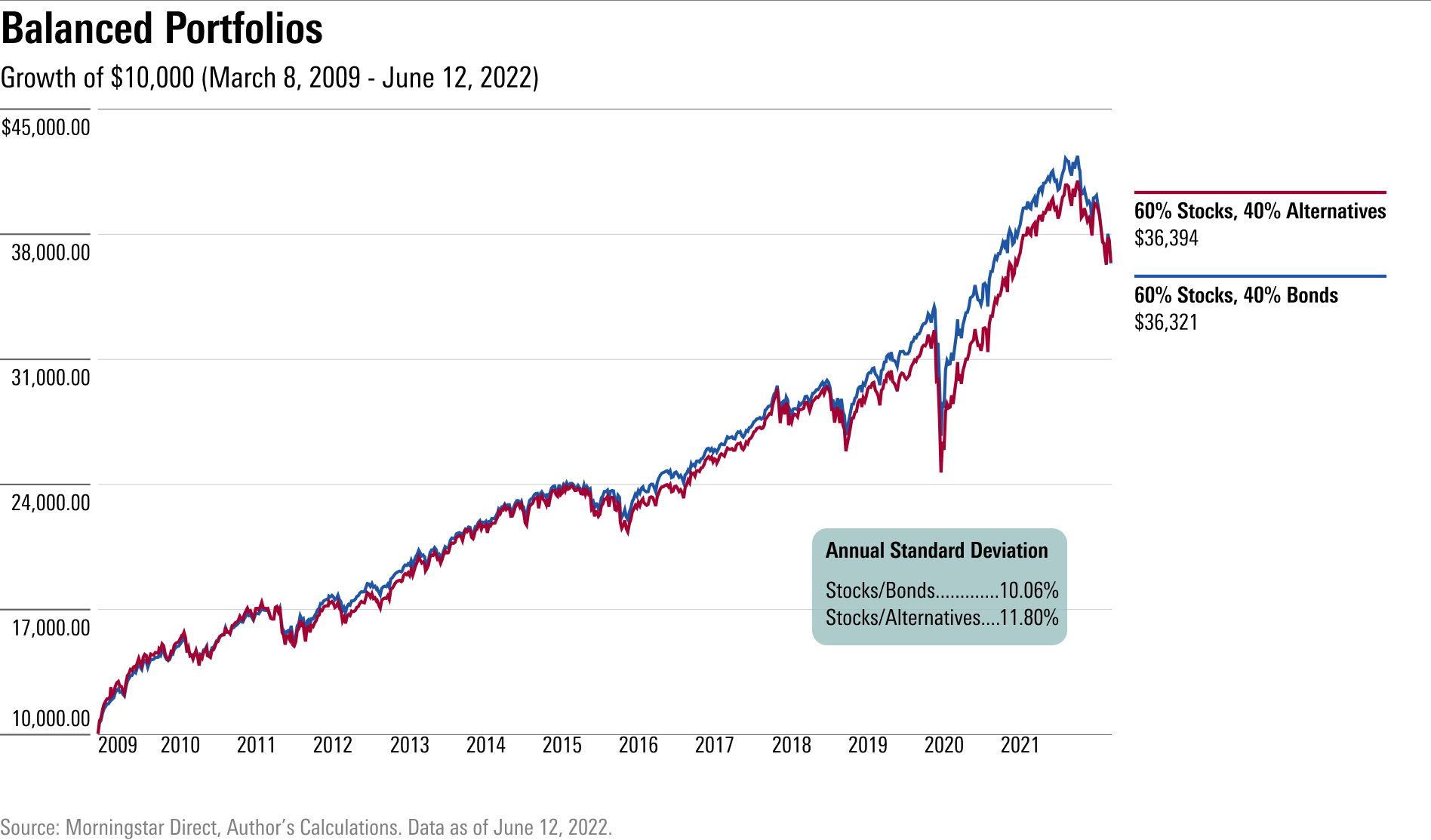

All would have been mistakes. Every market-timing fund has since disappeared. Hedge funds thrived for a short while, but they disappointed during 2008 and have not since regained their form. And while liquid alternative funds have shone recently, they have not improved upon the conventional choice. Since the financial crisis ended, a balanced portfolio that invested 60% in large-company stocks and 40% in intermediate-term bonds would have returned just as much as a rival that exchanged its bonds for liquid alternatives, while being less volatile.

Of course, this time might be different. Today’s conditions might signal a return to the environment of the 1970s, when inflation raged and bonds were ongoing losers. Rather than wait out the sandstorm, the ostrich might get buried.

Option 2: Allocate Differently

My colleague Amy Arnott suggests that investors add variety. Rather than rely on what essentially are two assets—stocks to provide high returns, and bonds to function as ballast—balanced portfolios should invest more broadly. Along with large dollops of international stocks and bonds, such portfolios such also include 5% positions in: 1) high-yield bonds, 2) REITs, 3) gold, and 4) other commodities.

Such counsel, of course, comes somewhat after the fact. (In fairness to Amy, she argued similarly last year.) But that does not mean that it arrives too late. If the developed world has indeed entered a new economic era—inflation being a global problem, rather than one that afflicts only the United States—then greater portfolio diversification should benefit investors for the foreseeable future.

There are three potential drawbacks to increasing portfolio diversification. It involves more work than owning only two investments. It will likely be more expensive, because funds that hold less-common asset classes typically charge more for their services. Finally, if a new economic era has not in fact dawned, such that inflation subsides, Treasuries will promptly recapture what they have lost. The investor who has made a “strategic” shift will find herself whipsawed.

Option 3: Become Tactical

Perhaps inflation will neither persist for several years nor soon abate. In which case, balanced-fund shareholders might benefit by temporarily adjusting their allocations to favor inflation-resistant assets such as commodities, gold, and liquid alternatives. Then, when the economic climate reverts to the norm, swap those assets for Treasuries, thereby returning to the previous formula.

That sounds good. Unfortunately, the record of professional managed mutual funds that invest in such fashion is dismal. Ten years ago, 22 funds promised in their names to provide “tactical allocation.” Today, only five of those funds remain. The rest have been either liquidated or merged. Predicting the future is delightfully easy when done in hindsight but wretchedly difficult in practice.

Thus, I cannot recommend tactical allocation. Periodically, I receive emails from readers who recently have made lucrative trades, and who cannot understand how others missed what they spotted. It seemed so obvious to them. The letters invariably are graciously phrased; the writers are puzzled rather than boastful. To which I can only respond: Best of luck! My talents do not lie in that direction. Nor, regrettably, do those of professional investment managers.

Final Words

All three options are imperfect. Staying the course may lead to additional inflation-related losses; switching to a new strategic allocation courts the danger of whipsaw; and tactical allocation is only for the gifted or lucky. That said, even after their recent upticks, long Treasury yields remain unappealingly low. Even at the risk of missing a long-bond rally, I prefer offsetting equities with intermediate-term notes or even cash.

Also, Amy’s advice is perpetually sound. Not all investors will wish to implement her suggestions fully. But as attractive as the customary 60% stock/40% bond approach can be, there is something to be said for smoothing the strategy’s edges, by adding assets that might be able to profit during those unusual occasions when both stocks and high-quality bonds swoon.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HTLB322SBJCLTLWYSDCTESUQZI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TAIQTNFTKRDL7JUP4N4CX7SDKI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

{kind=link}