Since the introduction of the qualified default investment alternative, or QDIA, about a decade ago, target-date funds have grown in popularity. That’s mainly due to their lower cost and ease of implementation. But despite their popularity, target-date funds often fall short when it comes to personalization. A managed accounts service can offer much greater personalization and advice, but it often comes at a higher cost.

So, what’s a plan sponsor to do?

The default investment decision is an important one, and historically, defined-contribution plans have been limited to choosing a single option. But a new, dynamic approach may help plan sponsors get the best of both worlds.

What is a dynamic default investment?

A dynamic default investment is the use of multiple defaults, such as managed accounts and target-date funds. The default investment varies by participants. And under such an arrangement, the plan sponsor could default participants into different benefits options based on certain criteria.

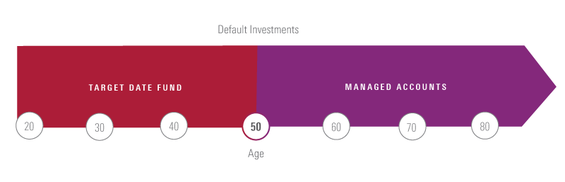

For example, a plan sponsor may decide to default participants into managed accounts once they reach a certain age (i.e. 50) while younger participants would be defaulted into target-date funds. This idea of a “dynamic” or “hybrid” default, where the default investment varies by age, is illustrated in the example below.

The dynamic default investment concept illustrated above shows how participants who were initially defaulted in target-date funds would move into managed accounts when they reach the transition point. In this example, it’s age 50. But a plan sponsor could use other attributes to divide participants, such as income, balance, or a combination of factors.

How does cost impact the dynamic default investment?

Cost is a key consideration when deciding the right default option for a participant. If the additional cost of managed accounts is relatively low, that could favor wider use of managed accounts. As the cost of managed accounts increases, target-date funds—or the alternative default option—becomes more attractive. So, the transition decision should not only be based on participant demographics and plan information, but also on the cost of the different options as well.

The future of dynamic default investments in defined-contribution plans

There are relatively few providers offering a dynamic default solution today, with Empower Retirement being among the first to announce a product and Fidelity also making an announcement shortly thereafter. We expect both interest and availability of these types of dynamic default solutions to increase in the future.

Please see below for important disclosure.