Previewing 2018 Global Industry Classification Standard Updates

How will the proposed 2018 Global Industry Classification Standard changes affect your sector-focused ETFs?

/s3.amazonaws.com/arc-authors/morningstar/64dafa24-41b3-4a5e-aade-5d471358063f.jpg)

In mid-November 2017, S&P Dow Jones and MSCI (SPDJI/MSCI) announced that the Global Industry Classification Standard, or GICS, telecommunication services sector would be broadened and renamed communication services. The communication services sector will add select media, entertainment, and consumer Internet stocks from the consumer discretionary and information technology sectors to its current telecommunication services constituents.

The GICS structure changes will be implemented after the market close on Friday, Sept. 28, 2018. SPDJI/MSCI plan to announce the large market capitalization companies affected by the GICS structure change in January 2018. This change will have an impact on index funds that focus on the telecommunication, information technology, and consumer discretionary sectors.

How Did We Get Here? SPDJI/MSCI joined forces to create the GICS industry taxonomy system in 1999. GICS organizes companies into subindustries based on the business activities that generate most of each firm's revenues. GICS is a four-tiered system where subindustries roll up into industries that make up industry groups, which are merged together to create the familiar GICS sectors. The original rendition included 10 sectors, 23 industry groups, 59 industries, and 123 subindustries. There are currently 11 sectors, 24 industry groups, 68 industries, and 157 subindustries. The last major GICS change occurred at the end of August 2016 when SPDJI/MSCI created the new real estate sector as an industry group carve out from the financials sector. Although that change created a new GICS sector, the forthcoming GICS sector reshuffle affects several sectors and will be more complicated than the real estate sector creation, which had an impact on only the financials sector.

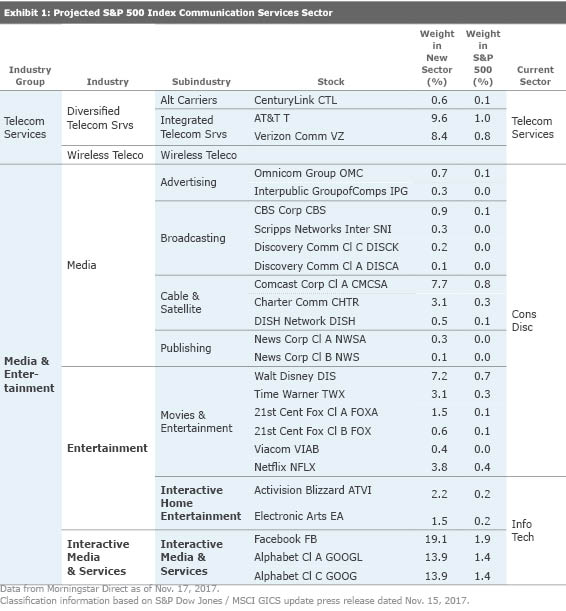

Impact Analysis I evaluated SPDJI/MSCI's GICS press release to create my projections of the S&P 500 constituents that will make up the newly anointed communication services sector. Note that Exhibit 1 is solely my view, and SPDJI/MSCI plan to provide more information about which large-cap stocks may be affected by the GICS update in January 2018. I calculated stock weightings in Exhibit 1 using market capitalizations as of Nov. 17, 2017. Bold text represents new industry groups, industries, or subindustries.

The newly formed sector adds media-focused stocks from the consumer discretionary sector and information technology stocks that create or distribute content through proprietary platforms to the current telecom services lineup. SPDJI/MSCI explains that categorizing these stocks together “is a step towards acknowledging the convergence of telecommunications, media, and select internet companies and overlapping services rendered by these companies, within the GICS Structure.” Given the integration of Internet, media, and telecommunications companies, I think that the GICS updates accurately reflect the changing competitive environment and are appropriate.

That said, these changes will significantly alter the composition of the current telecommunication services sector, making it considerably broader and less defensive. For example, the new S&P 500 communication services sector’s beta with the S&P 500 (a measure of market sensitivity) would have been 1.0 during the trailing three years through October 2017, while the current S&P 500 telecommunication services sector’s beta measured 0.6 during that period. This is because the media and content distributors tend to be more cyclical than traditional phone companies, like

Notable (possible) stock migrations from the information technology sector include

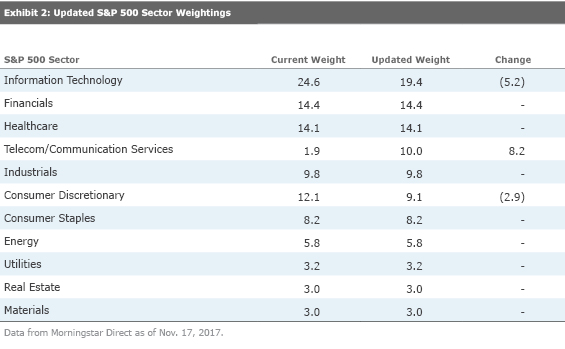

Based on stock market capitalizations as of Nov. 17, 2017, the communication services sector will represent about 10% of the S&P 500. In addition to the current telecom services stocks (these represent 2% of the S&P 500), the updated sector will draw names from the consumer discretionary and information technology sectors that represent about 3% and 5%, respectively, of the S&P 500. Exhibit 2 summarizes the S&P 500 sector weighting changes based on current market capitalizations.

The sector changes help reduce sector concentration within the S&P 500. Currently, the top five sectors of the S&P 500 represent nearly 75% of its market capitalization. After the projected GICS sector changes, the top five sectors will represent about two thirds of the S&P 500’s market capitalization.

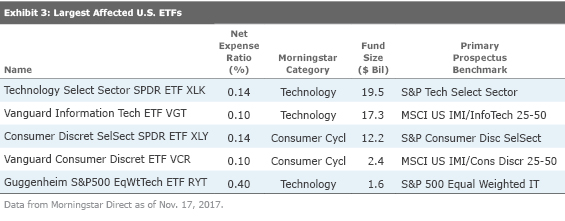

State Street Global Advisors

Vanguard does not include telecommunication services stocks in

Sector funds that do not use GICS classifications will not be affected. For example, BlackRock’s iShares sector funds track Dow Jones sector indexes and will not be immediately affected by the GICS update. Consequently,

Understand the Implications for Your Holdings SPDJI/MSCI incorporates the investment community's feedback during its annual GICS review and provides a long lead time ahead of potential changes so investors have time to react. Investors who hold affected funds should understand the implications of the upcoming GICS changes, decide if they agree with the reclassifications, and either keep or swap their sector funds to express their investment beliefs.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click

for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets,

or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)